Over the past half-century of industrialisation, the global seaborne iron ore market consolidated around a duopoly dominated by Australia's Pilbara region and Brazil's Carajás and Iron Quadrangle districts. However, driven by macroeconomic cycle evolution, a structural shift in China's growth engine, and the steel industry's irreversible push toward low-carbon and green transformation, this traditional supply map is undergoing an unprecedented reshaping.

On 26 November 2025, the first commercial vessel loaded with Simandou iron ore departed from the Port of Mabarya, marking the official commissioning of Guinea's Simandou Iron Ore Project — the world's largest undeveloped high-grade greenfield iron ore deposit by reserve. This milestone signals that the African continent, long relegated to secondary status, is progressively emerging as a significant new force in the global ferrous metals market.

Africa's iron ore resources are widely regarded as the third-largest iron ore supply region globally, after Brazil's Carajás and Australia's Pilbara. With an estimated 13.8% share of global iron ore resources, and representing the most significant supply-side growth driver over the next five years, shifts in African iron ore dynamics will be a key determinant of international iron ore pricing over the long term.

I. Global Iron Ore Market Background

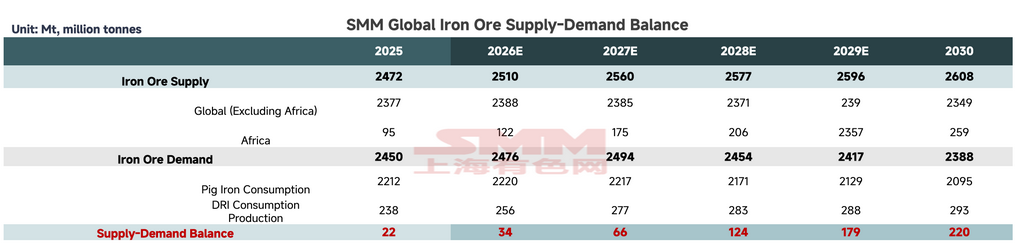

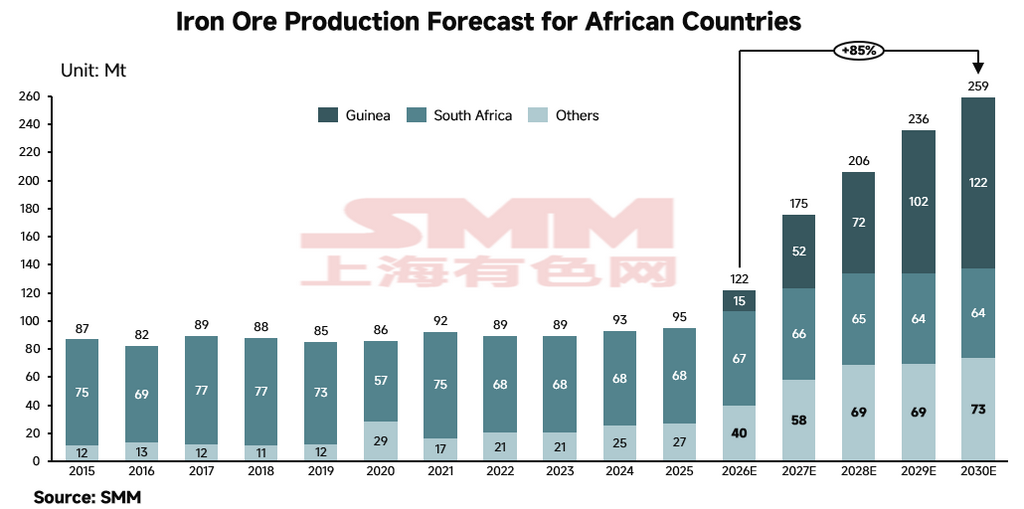

According to SMM research data, global iron ore production in 2025 is estimated at approximately 2.472 billion tonnes (bt). Africa contributes roughly 95 million tonnes (Mt), representing close to 4% of global output. As major mining projects progressively come on stream, Africa's iron ore production capacity is forecast to double by 2030, reaching approximately 259 Mt. Assuming no production curtailments elsewhere, Africa's global market share could rise to nearly 10%, while the overall global iron ore supply surplus is projected to widen to approximately 220 Mt.

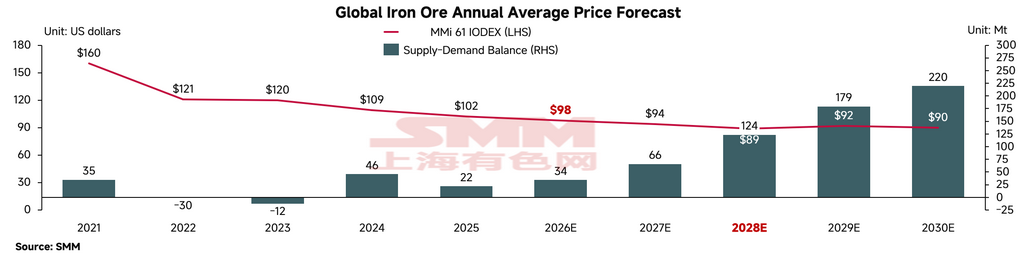

Although the international iron ore market has already entered a prolonged loose supply cycle, the substantive supply shock from African iron ore is expected to materialise gradually over the next five years. In the near term, Africa's estimated incremental shipment of approximately 15 Mt in 2026 — bolstered by its superior high-grade characteristics — is expected to be absorbed relatively smoothly by steelmakers seeking low-carbon blending feedstocks, resulting in a relatively moderate impact on absolute benchmark pricing.

The critical inflection point is projected to fall in 2028–2029. As rail and port infrastructure currently under construction in West Africa is fully commissioned, a surge in high-grade iron ore output will exert heavy downward pressure on the right-hand side of the global iron ore cost curve. This will not only systematically compress the iron ore price floor but will trigger intense structural displacement — squeezing the operating margin of low-grade, high-cost producers. The current price downcycle is expected to persist through 2028. When international ore prices breach the USD 90/tonne marginal cost support level, higher-cost non-mainstream small and mid-size mines will be forced into curtailment and exit. The resulting supply shakeout will reshape the global iron ore supply structure into a multi-oligopoly dominated by ultra-large, low-cost operations (including the new African mines), complemented by quality mid-tier producers.

II. Africa's Current Market Landscape: South Africa as Dominant Producer, West Africa Expanding Aggressively

Building on the global context, this section focuses on Africa's overall iron ore landscape. As the primary driver of supply growth over the next five years, Africa's iron ore production is concentrated in West Africa and South Africa, currently dominated by three key countries.

South Africa

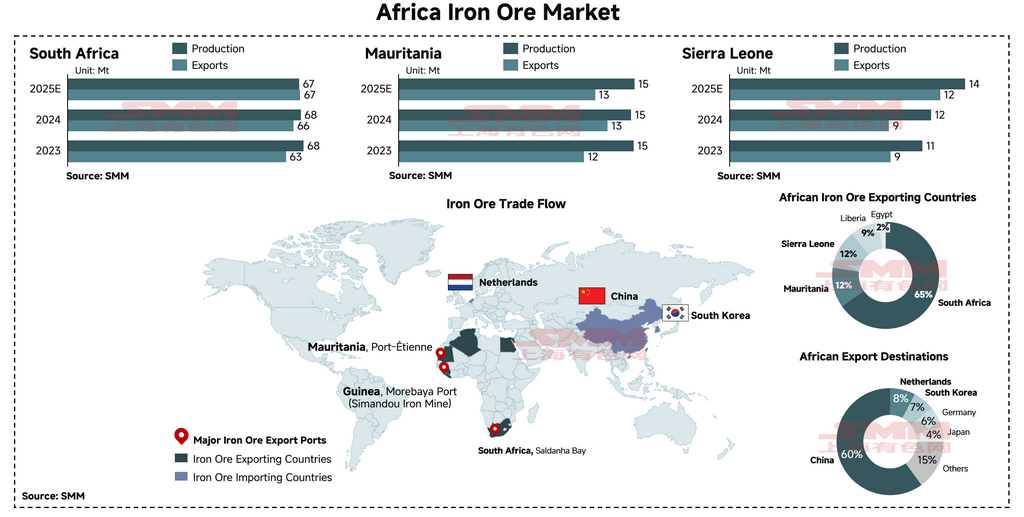

South Africa is the continent's largest producer, with 2025 output reaching approximately 67 Mt and export shipments maintaining an overwhelming 65% share of total African iron ore exports. However, South Africa's iron ore sector faces structural constraints limiting its organic growth headroom. As other emerging African resource nations commission significant new projects, South Africa's share of total African export volumes is projected to face sustained compression.

Mauritania

Mauritania is Africa's second-largest iron ore producer, with 2025 output of 15 Mt and export volumes of approximately 12 Mt, representing approximately 12% of the African market. Strategically situated adjacent to the Atlantic Ocean with high-grade iron ore deposits deep within the Sahara Desert, Mauritania possesses highly advantageous geographic and mineralogical characteristics. Its proximity to European and Middle Eastern markets — both in urgent need of green industrial raw materials — provides ideal conditions for the country to become a hub for global green metallurgy capacity relocation. Mauritania is expected to emerge as a highly promising iron ore supply nation going forward.

Sierra Leone

Sierra Leone is another important regional supply pole, with projected 2025 output also reaching approximately 12 Mt, holding a stable share of approximately 12% in the African export market. Chinese-invested iron ore mines within the country are actively scaling up their operations.

Trade Flow Overview

Based on full-year 2024 trade data, the proportion of African iron ore shipped to China is relatively low compared to traditional mainstream ore origins, at approximately 60%. The broader Pan-Asian market — encompassing China, Japan, and South Korea — absorbs approximately 70% of total African iron ore shipments. Western European countries, led by the Netherlands and Germany, constitute Africa's core secondary destination, accounting for close to 14% of trade flows. The remaining marginal trade flows are broadly diversified, extending to emerging steelmaking capacity clusters in the Middle East, including Bahrain, Oman, and Saudi Arabia.

Key Corporate Players

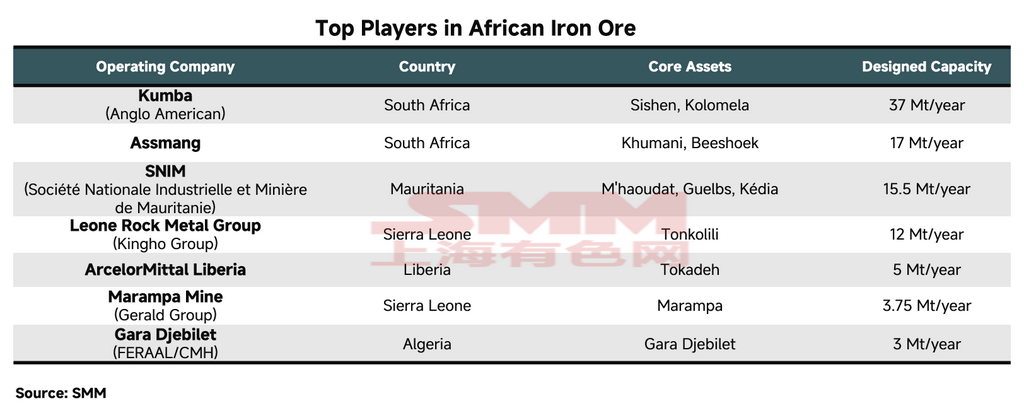

At the corporate level, South Africa's Kumba Iron Ore and Assmang rank as Africa's largest and second-largest iron ore producers, with annual output of approximately 37 Mt and 17 Mt respectively.

Kumba Iron Ore: Kumba's mining operations — including the Sishen mine — are globally recognised for producing high-grade fines (Fe >62%) and metallurgically superior premium lump ore (Fe 65.2%). Under the prevailing trend of blast furnace (BF) emission reduction, this type of direct-charge lump ore — which reduces sintering-related carbon emissions — commands strong market demand and a substantial price premium.

Assmang: Assmang similarly holds high-quality iron ore assets, operated as a 50:50 joint venture between African Rainbow Minerals (ARM) and Assore. Its Assmang Fines and Assmang Lump products (Fe 64–65%) are also direct-charge, high-quality materials. However, the company's key bottleneck lies not at the pithead but on the rail. Heavy dependence on Transnet Freight Rail (TFR) for haulage means logistics constraints frequently cap its achievable shipment volumes.

SNIM (Société Nationale Industrielle et Minière): Mauritania's state-owned mining company is Africa's third-largest iron ore producer after the two South African majors. Unlike mainstream Australian and Brazilian ores, SNIM products occupy a distinctive niche in terms of physicochemical specifications and market segment. Its most widely traded product, TZFC fines, is characterised by extremely low alumina (Al2O3) and phosphorus (P) content. As an excellent blending ore, major steelmakers regularly blend SNIM fines with high-alumina Australian fines (such as certain Pilbara blend products) to significantly dilute the impurity ratio in the burden, thereby optimising blast furnace performance metrics.

III. Africa's Market Transformation: Major Producers Facing Stagnation; Emerging Projects as Primary Growth Drivers

Where does future growth lie? According to SMM observations, Africa is expected to undergo a significant structural transformation within the next five years. Multiple large-scale iron ore projects across the continent are currently under construction, with scheduled commissioning prior to 2030. Based on our modelling, African iron ore supply is forecast to grow substantially from the current approximately 95 Mt to 260 Mt over five years — a cumulative increase of 85%. The market structure is also expected to shift from South Africa-dominated Western-oriented exports to a Guinea-led export paradigm.

Guinea — Simandou Iron Ore Project

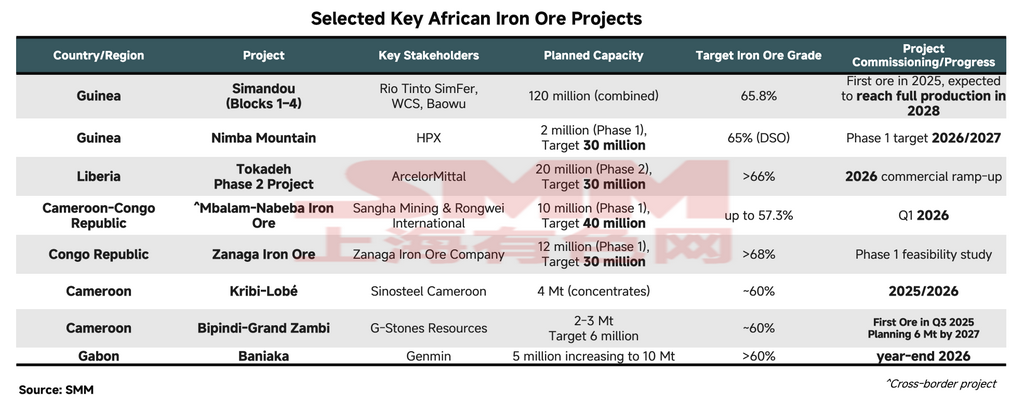

The primary growth driver will be Guinea's renowned Simandou iron ore project, jointly developed by multiple entities and representing the world's largest undeveloped high-grade open-pit hematite deposit. The project holds reserves in excess of 5 billion tonnes (bt) and a designed production capacity of 120 Mt per annum, making it the project with the greatest strategic potential to reshape the existing iron ore market structure.

Since first ore shipments in late November 2025, cumulative exports from the principal export hub — the Port of Mabarya — reached approximately 1.6 Mt through Q1 2026. Blocks 1 & 2, developed under the Winning Consortium Simandou (WCS), have successfully commenced production, with 2026 capacity expected to reach nameplate and ramp-up to 60 Mt per annum projected over the next two to three years. Blocks 3 & 4, led by Simfer (a Rio Tinto and Baowu joint venture), are forecast to commission in Q1 2026, with estimated 2026 shipments of 5 Mt and a 30-month ramp-up timeline to reach 60 Mt per annum. In aggregate, Guinea is projected to achieve 120 Mt per annum before 2030, becoming the world's second-largest single iron ore project by capacity — second only to Vale's S11D project in Brazil (designed capacity of 200 Mt post-expansion, expected by 2030).

Other African Countries — Key Development Projects

Other nations — including Liberia, Gabon, Sierra Leone, and the Republic of Congo — all have iron ore projects under development. Projects scheduled for commissioning before 2030 account for a combined planned capacity of approximately 46 Mt. The largest single project is ArcelorMittal Liberia's (AML) Tokadeh Phase II, expected to commission in H2 2026 and reach a nameplate capacity of 20 Mt per annum by year-end, producing iron ore concentrate with an estimated grade exceeding Fe 66%. Given that AML's European steelmaking capacity cannot absorb such a large volume increment in the near term, the majority of Tokadeh's output is expected to enter the international seaborne market, exerting pricing pressure on the iron ore concentrate segment.

South Africa — Structural Constraints on Production Growth

South Africa's output is expected to remain broadly stable in the 63–67 Mt range, with mild downside risk. The primary underlying cause is the country's heavy dependence on the heavy-haul Sishen–Saldanha Bay rail corridor, operated by Transnet Freight Rail (TFR). In recent years, TFR has suffered a severe reduction in effective haulage capacity due to locomotive fleet shortages, frequent cable theft incidents, and chronic infrastructure underinvestment, materially constraining the rail transport of major bulk commodities including iron ore and coal.

In its FY2025 annual results published in February 2026, Kumba Iron Ore — South Africa's dominant iron ore producer — reported total finished goods inventory of 7.5 Mt, up from 6.9 Mt at end-2024. With rail haulage capacity unable to match mine production, South Africa's major iron ore producers have been compelled to stockpile large volumes at mine sites. To avoid inventory saturation, miners have been forced to proactively revise production guidance downward. While producers are actively addressing haulage constraints, the deeply entrenched structural issues on the rail network are unlikely to be resolved in the short term.

Mauritania — SNIM Long-Term Strategic Growth Blueprint

Post-2030, attention turns to SNIM's strategic growth roadmap. Under its Horizon 1 programme, the company plans to raise annual production capacity to 45 Mt by 2031, through the implementation of lean manufacturing practices, equipment and technology upgrades, and the co-development of new mineral reserves. Of this total, 20 Mt will be produced under SNIM's wholly owned capacity, while the remaining 25 Mt will be realised through joint ventures with international capital partners. SNIM has further set a long-term target to expand annual capacity to 80 Mt by 2045 under its Horizon 3 plan.

Democratic Republic of Congo (DRC) — MIFOR (Grand Est Iron Ore Project)

On 26 March 2026, the DRC and China signed a Memorandum of Understanding designating the MIFOR project as a priority flagship initiative. The deposit is estimated to hold cumulative resources of 15–20 bt, with an average grade exceeding Fe 60% — a potential scale approximately 2.5 times that of Guinea's Simandou. Phase I capital expenditure is estimated at USD 28.9 billion, encompassing the construction of a heavy-haul railway and the utilisation of Congo River navigation, ultimately linking to a deep-water port at Banana on the Atlantic coast. Phase I design capacity stands at 50 Mt per annum, with a long-term target of scaling to 300 Mt per annum. These projects collectively underscore Africa's inevitable emergence as an indispensable iron ore supply source for the global steel industry.

IV. Global Steel Industry Chain Transformation: Can Africa, as a Hub for High-Grade Ore, Enable DRI Production?

High-Grade Ore as a DRI Feedstock Advantage

Notably, the majority of Africa's current and planned iron ore projects produce ore at average total iron (Fe) grades predominantly above 65%, with extremely low impurity content. This scarce, high-grade ore is the ideal feedstock for the Direct Reduced Iron (DRI) process. As the DRI-Electric Arc Furnace (EAF) green steel route gains traction across Europe, the Americas, and China, demand for iron ore at Fe 65% and above will grow exponentially on the demand side. This will confer a substantial 'grade premium' on major projects, including South Africa's Kumba, Guinea's Simandou, and other future African producers. Over the longer term, iron ore pricing benchmarks are inexorably shifting away from the traditional Platts 62% Fe index, and African ore producers will gain bargaining leverage when renewing long-term supply agreements, thereby reshaping the global industry chain profit distribution structure.

DRI Investment Pipeline in Africa

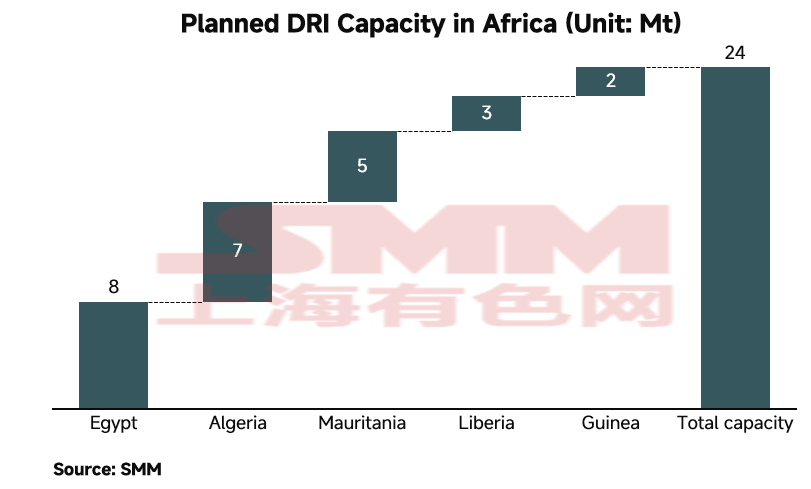

In alignment with global carbon neutrality objectives, international investors — encouraged by local governments — are actively deploying capital into high value-added downstream processing facilities, including DRI plants and high-grade pellet facilities, aimed at leveraging Africa's abundant high-grade iron ore resources and vast renewable energy potential for DRI production. According to SMM observations, Africa is projected to add approximately 20 Mt of DRI capacity by 2030. The largest single project is a Libyan integrated DRI complex, jointly developed by Turkish steelmaker Tosyali and the Libyan National Steel Company, with a total design capacity of 8.1 Mt.

China's Decarbonisation Push and the Global Green Steel Transition

As China advances its dual carbon targets — carbon peaking by 2030 and carbon neutrality by 2060 — the domestic steelmaking sector is undergoing significant adjustment. The traditional carbon-intensive Blast Furnace–Basic Oxygen Furnace (BF-BOF) long route faces increasingly stringent capacity replacement policies and environmental regulations. Simultaneously, the global trade system is accelerating the imposition of carbon costs, most notably through the EU Carbon Border Adjustment Mechanism (CBAM), compelling global steel supply chains to accelerate the transition from the source toward a low-carbon, ultimately zero-carbon 'green steel' era.

In the context of this irreversible transition, the DRI-EAF short-route process has become the most commercially viable decarbonisation pathway. To meet surging global demand for green steel, market projections indicate that global DRI designed production capacity will need to expand by hundreds of millions of tonnes during the 2030s. This scale of expansion will profoundly alter the global steel supply structure: the share of traditional hot metal (pig iron) production will progressively decline, while low-carbon DRI supply will directly determine the competitiveness of major economies in the global green steel market. In particular, 'hydrogen metallurgy' — using green hydrogen to replace natural gas and coking coal as the reductant in iron ore reduction — is widely recognised by the industry as the core technology for achieving ultimate zero-carbon steelmaking.

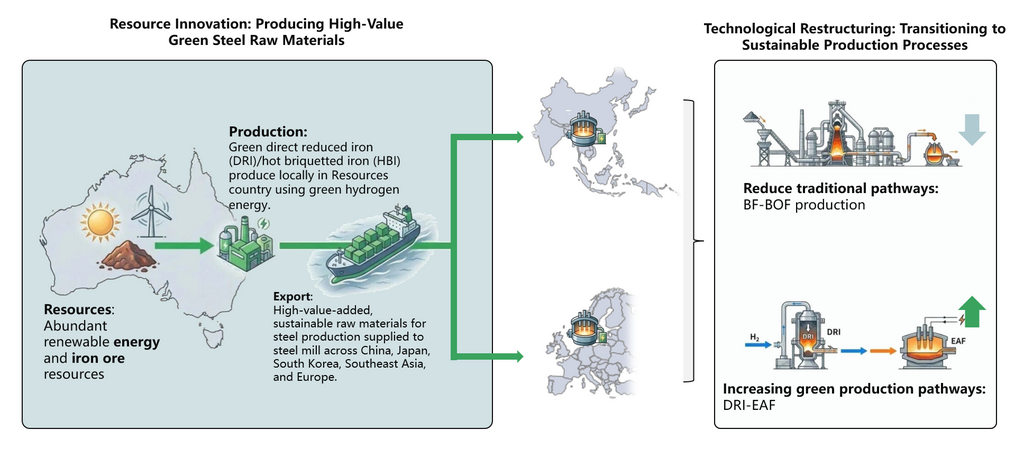

Africa as the Future 'Green Iron' Production Hub

Represented by world-class high-grade iron ore projects such as Guinea's Simandou, the progressive commissioning of these mega-mines is expected to inject over 100 Mt of high-grade iron ore per year into the global market, substantially alleviating the global scarcity of DRI-grade ore. More critically, North Africa and West Africa possess world-leading solar and wind energy potential, enabling large-scale, low-cost green hydrogen production in situ. This perfect combination of 'high-grade ore + low-cost green hydrogen' is increasingly inclinng multinational capital and steel majors toward establishing DRI production lines directly on African soil — reducing iron ore to low-carbon Hot Briquetted Iron (HBI) on-site for ocean transport to EAF facilities in Asia and Europe. Africa is thus formally transitioning from its historical role as a raw material exporter to become an indispensable link in the green iron production chain of the future.

![[SMM Iron & Steel] Brazilian Crude Steel Output and Domestic Sales Rise in April 2026 Amid Shrinking Imports](https://imgqn.smm.cn/usercenter/DpLok20251217171715.png)

![[SMM Iron & Steel] Feralpi Stahl Plans to Expand Riesa Plant Capacity to 1.3 Million MT by 2027](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)

![[SMM Iron & Steel] US Drawn Wire Exports Jump 19.4% in March 2026 Driven by Mexican Demand](https://imgqn.smm.cn/usercenter/EXHJE20251217171720.jpg)