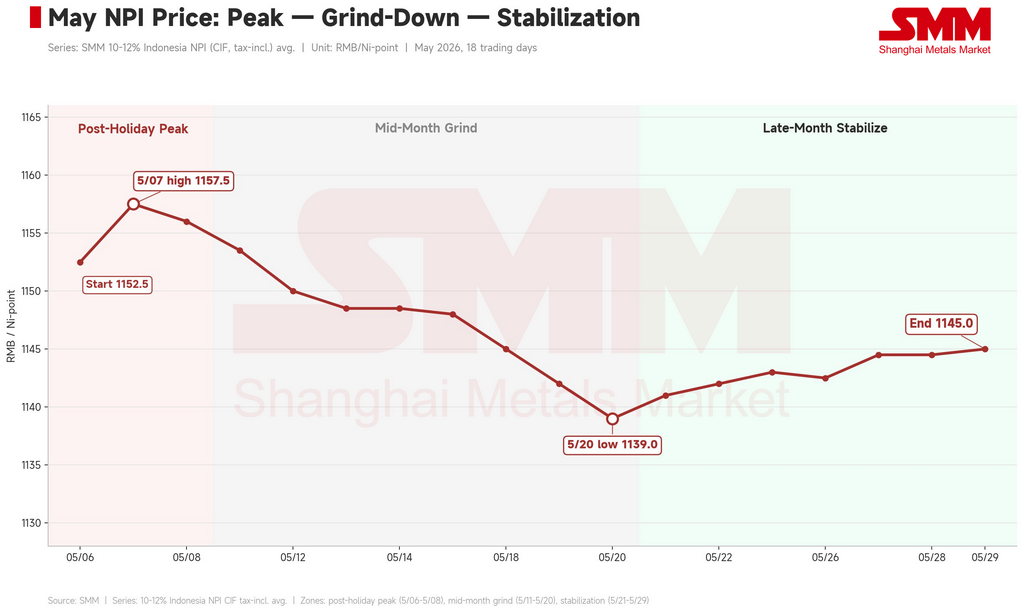

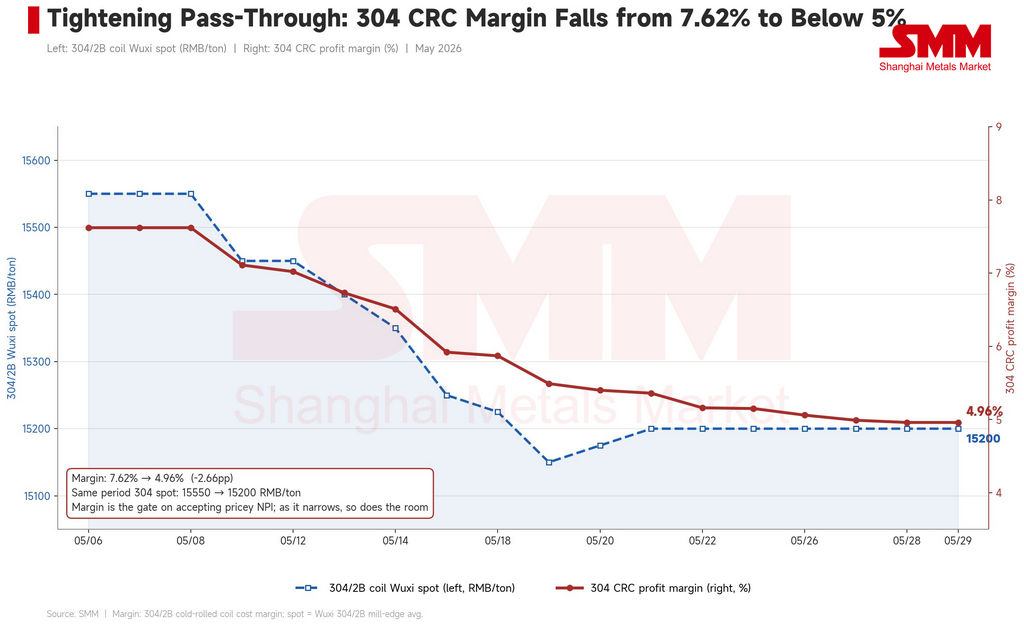

Heading into China's May Day holiday, Chinese stainless steel mills restocked at around RMB 1,130 per nickel unit (≈ $165). When the market reopened, it tried to ride April's late rally higher: the CIF China price for 10–12% Indonesian high-grade Nickel Pig Iron (NPI) opened at RMB 1,152.5/nickel unit (≈ $168) on May 6 and touched a monthly high of RMB 1,157.5 (≈ $169) the next day. The Shanghai Futures Exchange (SHFE) nickel contract climbed in lockstep to RMB 153,600/mt (≈ $22,420), and the 304 cold-rolled margin was pushed to 7.62%. All three peaked together — and that was the ceiling for the month.

From there, high-grade NPI ground steadily lower to a monthly low of RMB 1,139/nickel unit (≈ $166) on May 20, only stabilizing back to RMB 1,145 (≈ $167) in the final week on the back of policy noise and production-cut expectations. Over the full month, the 10–12% Indonesian CIF price slipped from RMB 1,152.5 to RMB 1,145 — essentially giving back part of April's late spike and then flatlining.

(For readers outside China: NPI is priced in "nickel units" — RMB per one percentage point of nickel content per metric ton. A 10–12% grade therefore carries a per-ton price of roughly eleven times the quoted figure. NPI is a low-grade ferro-nickel alloy made from laterite ore, produced mainly in China and Indonesia, and consumed almost entirely by stainless steel mills. SMM is Shanghai Metals Market, China's main commodity price-assessment and research provider.)

This was not a linear decline. It was a relay of three different stories: a one-week speculative flare driven by the refined-nickel futures board, a mid-month triple squeeze, and an end-of-month standoff held up by Indonesian supply-side developments. More importantly, May ran April's thesis in reverse: the cost side was visibly tighter, yet price couldn't follow.

Week one: a refined-nickel flare that topped out almost immediately

Early May looked strong on the surface. Sellers lifted offers to RMB 1,170–1,200/nickel unit (≈ $171–175), and leading smelters argued that NPI at RMB 1,200 was justified because stainless had risen to RMB 15,700/mt (≈ $2,290). A few hundred tons did trade at RMB 1,200.

But those high prints don't survive scrutiny. As one trader noted, the RMB 1,200 deals were mostly hedged sellers liquidating — worried that nickel prices had peaked, they cleared inventory while they could, selling largely to intermediary traders and smaller mills. In other words, RMB 1,200 wasn't bought by real demand; it was sold by hedging positions cashing out near the top.

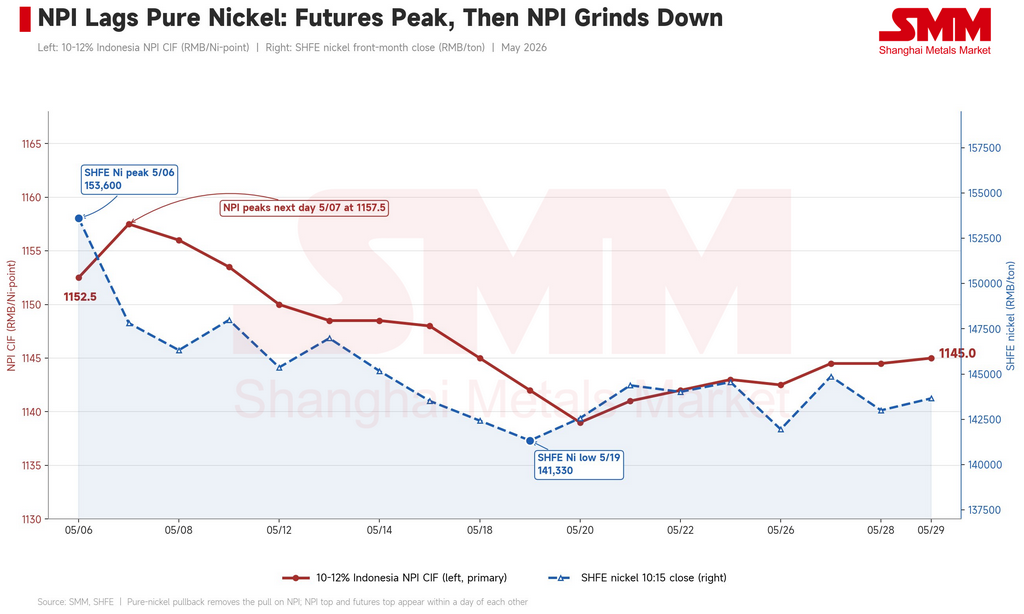

The real signal sat in the refined-nickel board. After peaking at RMB 153,600/mt on May 6, the SHFE nickel contract fell to RMB 147,800/mt (≈ $21,580) the very next day, and LME nickel turned down from its $19,770/mt high. Chase-the-rally sentiment faded that same day. The 10–12% Indonesian CIF price topped at RMB 1,157.5 on May 7 — the same window as the nickel-board peak. Week one's flare was the dying glow of April's nickel-led rally, pushed to its extreme through the holiday window, with the top already baked in.

Mid-month: a triple squeeze from futures, stainless, and scrap

May 11–20 was the month's main downleg, with the 10–12% Indonesian CIF price drifting from RMB 1,153.5 (≈ $168) to RMB 1,139 (≈ $166). This wasn't one factor — three variables turned at once.

First, the refined-nickel board kept falling. The SHFE nickel contract dropped from RMB 148,000/mt on May 11 to a RMB 141,300/mt (≈ $20,630) low on May 19, down about 8%. NPI trades behind refined nickel, so once the board weakened, the pull on NPI vanished — most traders simply attributed the week's softness to the falling futures.

Second, stainless weakened and mill margins compressed. Wuxi 304/2B spot fell from RMB 15,550/mt (≈ $2,270) at the start of the month to RMB 15,200 (≈ $2,220), and the SHFE stainless contract dropped from RMB 15,710 to a RMB 14,555/mt (≈ $2,125) low on May 19. The crucial mechanism is the margin: the 304 cold-rolled margin was squeezed from the post-holiday 7.62% to 5.40% by May 20. Margin is the master valve on whether mills can absorb expensive feedstock — as it narrowed, so did mills' room to pay up for NPI. Several mills repeatedly flagged weak stainless sales and sluggish coil shipments, and said they simply couldn't accept high prices.

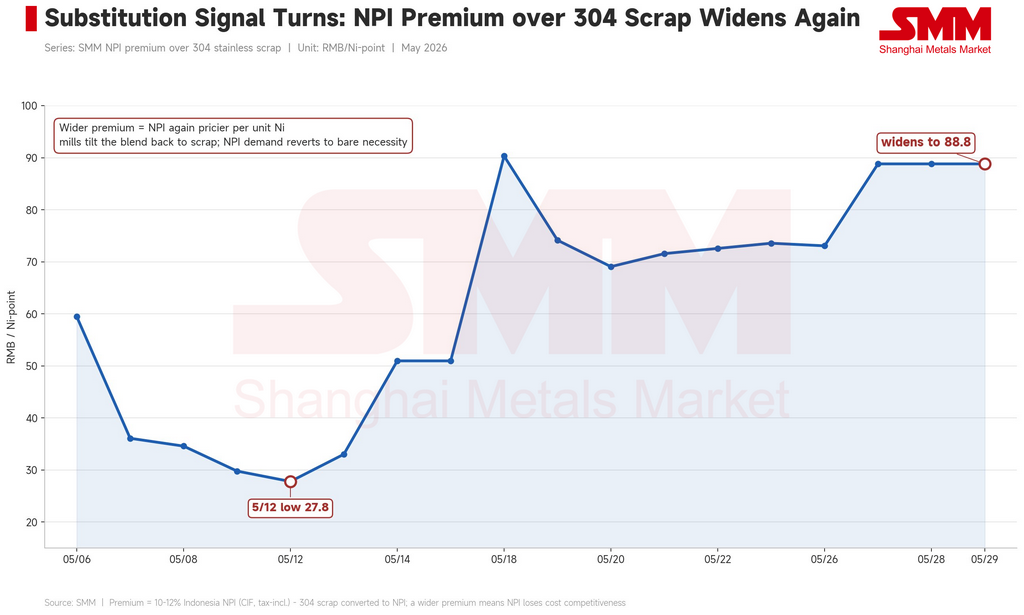

Third — and most telling — the scrap parity reverted. April's rally happened because NPI's premium over stainless scrap had been compressed, erasing scrap's substitution advantage and pushing mills from scrap back to NPI. May ran the exact opposite. Scrap prices fell alongside refined nickel; the market's implied nickel-unit cost for scrap dropped from RMB 1,132 (≈ $165) at the start of the month to RMB 1,128 (≈ $165) by May 19, with scrap at one point falling a further RMB 200/mt (≈ $29). High-grade NPI's premium over 304 stainless scrap widened sharply from a monthly low of RMB 27.8/nickel unit (≈ $4) on May 12 to RMB 88.84 (≈ $13) by month-end. A widening premium means NPI is again the more expensive source of equivalent nickel units — so mills naturally shifted the mix toward scrap and pulled NPI purchasing back to bare necessity.

Put the three together, and the striking point about mid-May is not how they pressured prices, but that they did so while Indonesia's cost side was strengthening in the opposite direction. Over the same period, the CIF Indonesia price for 1.5% domestic-trade laterite ore rose from $70.55 to $73.80 per wet metric ton, the Indonesian NPI FOB index held firm-to-strong, and the NPI smelting margin even flipped from negative to positive. The cost support was there the whole time — but it stayed trapped in sellers' offers and psychological floors and never made it into transactions. This is the core logic of NPI pricing: rising costs only transmit to price when the downstream cost structure and the futures board cooperate at the same time. Cost alone cannot hold up a rally.

The final week: supply-side support builds a floor, but stainless caps the ceiling

After May 21 the slide halted, with prices steadying and inching up within RMB 1,139–1,145/nickel unit. Two new supply-side variables put in the floor.

One was Indonesia's export and unified-pricing policy. Market attention clearly shifted toward Indonesian policy direction; sellers widely flagged the disruption, reasoning that if Jakarta's unified government pricing actually takes effect, retail spot supply would shrink markedly, limiting downside. One trader even raised offers by RMB 20/nickel unit (≈ $3) on the day over policy noise. Still, most doubt the execution: the prevailing view is that formal implementation won't come until Q3 or even year-end, with plenty of uncertainty in the transition.

The other was switching and cut expectations. A major Indonesian producer signaled it would convert part of its NPI lines to high-grade nickel matte from June; combined with an integrated project cutting output over power constraints, and another large producer's high inventories pushing some contracts to July delivery, the market built a fairly strong expectation of reduced NPI inflows into China.

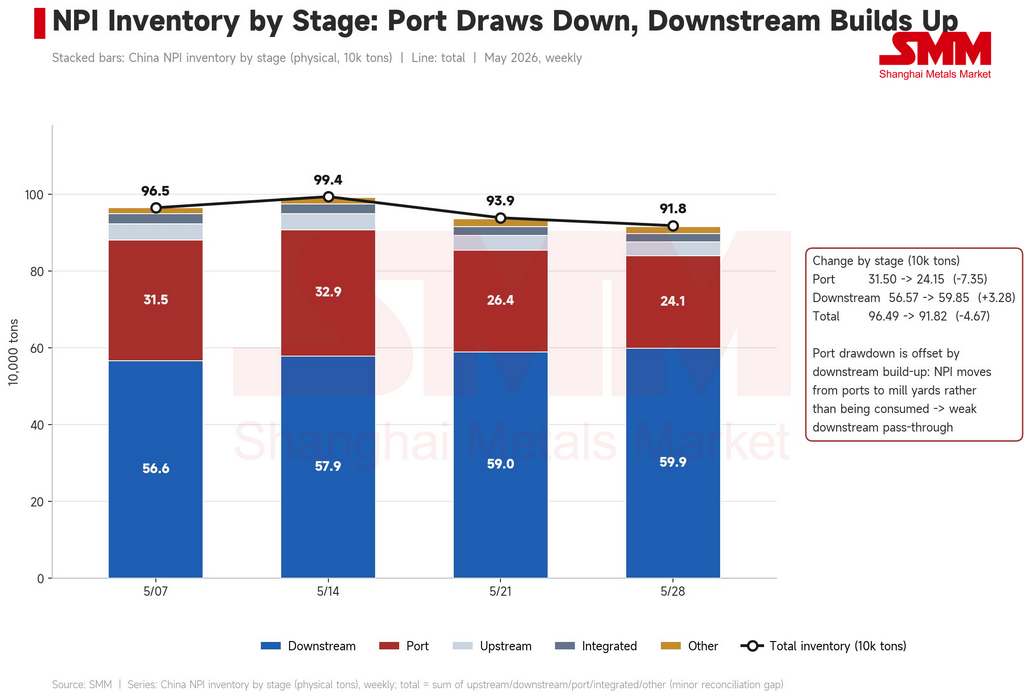

But the inventory picture only reads correctly when broken out by stage. Port inventory fell sharply from 315,000 mt at the start of the month to 241,500 mt at month-end — which, on its own, looks like improving demand. Over the same period, however, NPI inventory at downstream mills actually rose from 566,000 mt to 599,000 mt, so total inventory only edged down, from 965,000 mt to 918,000 mt. In other words, the port destocking was mostly NPI moving from ports into mills' hands, not being consumed. Against a backdrop of stainless output cuts and scrap substitution, NPI is increasingly piling up at the mill stage. Read the port number alone and you overstate demand; read the stages together and downstream consumption is actually soft.

These supply-side positives could build a floor but not a rally — and the reason, again, lands on stainless. The end-of-month consensus stated it plainly: the tight-supply expectation has formed, but prices can't rise because stainless hasn't risen in tandem and can't support higher feedstock costs. Some mills were blunter — at current prices, steelmaking is already loss-making and finished-product sales are weak. The 304 margin kept grinding down to 4.96% that week, tightening the absorption valve further. Pricing reverted to a premium over the average price, with end-of-month deal premiums for 11%-grade material generally down to just RMB 3–7/nickel unit (≈ $0.4–1.0), well below mid-month's RMB 10 (≈ $1.5). The supply side held the floor; the demand side capped the ceiling; price could only stand pat at elevated levels.

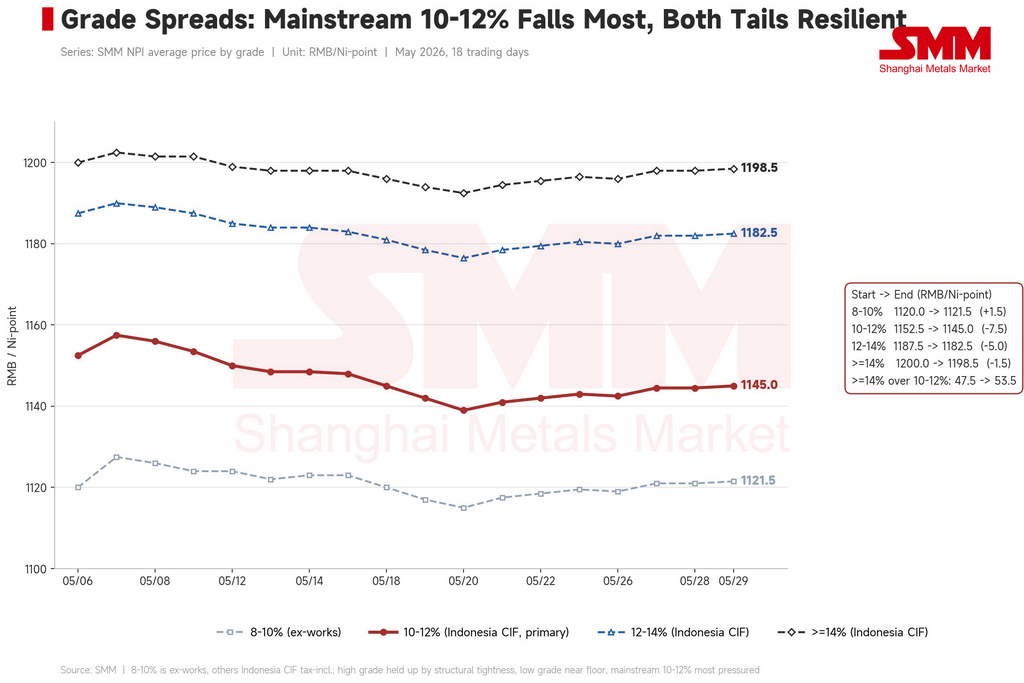

Grade spreads: the mainstream 10–12% fell hardest, both tails held up

Looking at start- and end-of-month figures by grade, the dividing line differs from April's. The 8–10% ex-works price edged up from RMB 1,120 to RMB 1,121.5/nickel unit (≈ $164) — essentially flat; the 10–12% Indonesian CIF fell RMB 7.5, the largest drop of any grade; 12–14% fell RMB 5; and ≥14% fell just RMB 1.5. The hardest-hit grade was the mainstream 10–12%, while both the high and low ends held up comparatively well.

The two tails held for different reasons. The high end was supported by structural scarcity: material above 12% was persistently tight all month, with several parties reporting fewer offers and only one or two holders with stock. One trader noted that each additional 0.5% nickel content commands a price difference of roughly RMB 5–10/nickel unit (≈ $0.7–1.5), more pronounced the higher the grade. That shows directly in the premium structure: the ≥14% premium over 10–12% widened from RMB 47.5/nickel unit (≈ $7) at the start of the month to RMB 53.5 (≈ $8) by month-end, and the 12–14% premium edged up from RMB 35 (≈ $5) to RMB 37.5 (≈ $5.5). The low-end 8–10% is a different matter — already at floor levels, 9–10% material struggled to sell even near RMB 1,100/nickel unit (≈ $161), leaving no room to fall further, so it simply held at the bottom.

Caught in the middle, the mainstream 10–12% bore the most pressure: it has neither the scarcity protection of the high grades nor the floor of the low grades, so the hits from the falling futures board and scrap substitution concentrated on this tranche. The driver of May's widening grade spreads was a wider high-grade premium — not April's broad split between low-grade domestic material and Indonesian CIF.

The June watch: direction still rests on two external variables — stainless and refined nickel

The Indonesian narrative — unified pricing, the switch to high-grade matte, output cuts — will keep rolling, and it is genuinely building marginal supply-side support. But three external variables will decide June's direction.

The first and most sensitive is whether stainless prices and mill margins can stop falling. The 304 cold-rolled margin has already compressed from 7.62% at the start of the month to under 5%, 304 spot has fallen from RMB 15,550 to RMB 15,200/mt, SMM's forecast for China-plus-Indonesia 300-series output of 1.795 million mt in May has materialized (already down 120,000 mt month-on-month from April), and 300-series inventory edged up to 608,300 mt at month-end. If stainless keeps weakening and margins compress further into June, mills' ability to absorb expensive NPI will keep falling. This variable bears more directly on whether prices stabilize and recover than any single Indonesian headline.

The second is NPI's cost relative to scrap. The end-of-month premium has widened to nearly RMB 89/nickel unit (≈ $13), and scrap's parity advantage has reasserted itself. As long as scrap flows don't tighten further, mills will hold or raise the scrap ratio, leaving NPI demand support soft.

The third is the refined-nickel board. The SHFE nickel contract stabilized at RMB 143,000–145,000/mt (≈ $20,880–21,170) at month-end. NPI trades behind refined nickel; if the board holds this range, it supports NPI's floor — if it falls again, NPI will lose its pull quickly.

In the base case, June high-grade NPI most likely trades in a high but soft RMB 1,130–1,160/nickel unit (≈ $165–169) range. Downside support comes from the supply contraction implied by switching, cuts, and policy, plus the structural scarcity of high grades; the ceiling is set by ongoing stainless margin compression and the renewed scrap advantage. The upside risk is a resonance of recovering stainless futures and spot, an Indonesian policy that lands faster than expected, and the matte switch actually materializing. The downside risk is the resonance of further stainless weakness, a refined-nickel pullback, and a still-wider scrap substitution advantage.

Conclusion

May's small slide in high-grade NPI from RMB 1,152.5 to RMB 1,145/nickel unit looks unremarkable, but it proved April's thesis in reverse. April was the two external variables — the refined-nickel board and stainless margins — firing together, pulling price from RMB 1,087 to RMB 1,138/nickel unit (≈ $159 to $166). May was both turning weak at once: the nickel board spiked and reversed, the 304 margin fell from 7.62% to under 5%, and price was pinned at elevated levels, gave back gains, and stabilized.

And all of this happened while Indonesia's cost and supply side, far from loosening, tightened: ore prices up mid-month, smelting margins turning positive, switching, cuts, and unified pricing stacking up. That is precisely the point. Indonesian cost shifts, ore grade, and auxiliary-material prices are a necessary condition for the center of gravity in NPI pricing — but far from a sufficient one. However tight the cost side gets, if the refined-nickel board won't cooperate and stainless margins offer no room to absorb, prices still can't rise — and may even give back ground.

This is the structural signature of an intermediate product with capacity concentrated in Indonesia but pricing power dispersed across China: it rises only when downstream allows it, and it falls when downstream decides. Where June goes still comes back to watching two variables — stainless margins and the refined-nickel board — not whatever the latest headline out of Indonesia happens to be.

![[SMM Nickel Midday Review] Nickel Prices Edged Down on June 1, China's Manufacturing PMI Came in at 50.0% in May](https://imgqn.smm.cn/usercenter/KFwsY20251217171734.jpg)

![[NPI Daily Review] Policy Uncertainty Intensified, Strong Wait-and-See Sentiment Prevailed in the Market](https://imgqn.smm.cn/usercenter/UpZsx20251217171731.jpeg)