European Raw Material Market May Review: APT Consolidated at Highs with Recovering Sentiment, Supply Shortages Supporting Price Stabilization

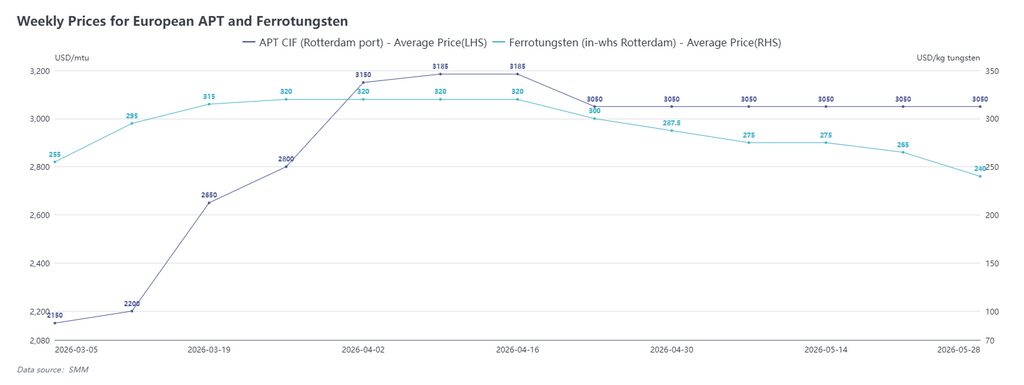

According to SMM data, as of May 29, APT CIF Rotterdam port was quoted at $2,900-3,200/mtu, with an average price of $3,050/mtu, flat compared to early May; Ferrotungsten (Rotterdam warehouse) was quoted at $220-260/kg tungsten, with an average price of $240/kg tungsten, down 16.5% from early May.

In May 2026, European APT prices consolidated at highs above $3,000/mtu after a slight correction at the end of April. Transaction side, some APT and tungsten oxide spot cargoes flowed out of Southeast Asia in early May, with APT transaction prices reaching $3,200/mtu with European downstream buyers. After very limited spot cargoes were cleared, the market returned to a raw material shortage pattern in mid-to-late May, with a situation of quoted prices but no actual trades supporting Rotterdam prices stabilizing within the previous transaction price range.

Sentiment side, European end-users were affected by the continuous decline in Chinese tungsten prices at the end of April, with overall market sentiment being poor and buyers showing low acceptance of high prices. However, due to the rigid existence of raw material shortages, new transaction prices remained stable above $3,000/mtu, providing strong consolidation support for the European market. Overall, European market sentiment stabilized in May, with prices not significantly impacted by the continued decline in the Chinese market.

Ferrotungsten market, Rotterdam warehouse ferrotungsten prices fell sharply by 16.5% this month, mainly because European ferrotungsten trade accounted for a relatively small share, with most demand relying on imports from China. In May, Chinese ferrotungsten FOB prices declined 22.6% overall, following the Chinese market trend. However, due to scarce market orders and trading volumes in late May, European prices lagged the market and remained $40-50/kg tungsten higher than China.

Overall, European market sentiment recovered somewhat at the end of May, with the market returning to a pattern of quoted prices but no actual trades and tight supply. Combined with Chinese prices beginning to recover at month-end, market sentiment was further boosted, and the consolidation at highs is expected to continue. If new raw material resources from outside China flow into the market subsequently, European prices may even have the potential to rise further.

International Tungsten Scrap Market May Review: Europe Fell Sharply, India Adjusted Accordingly Then Stabilized

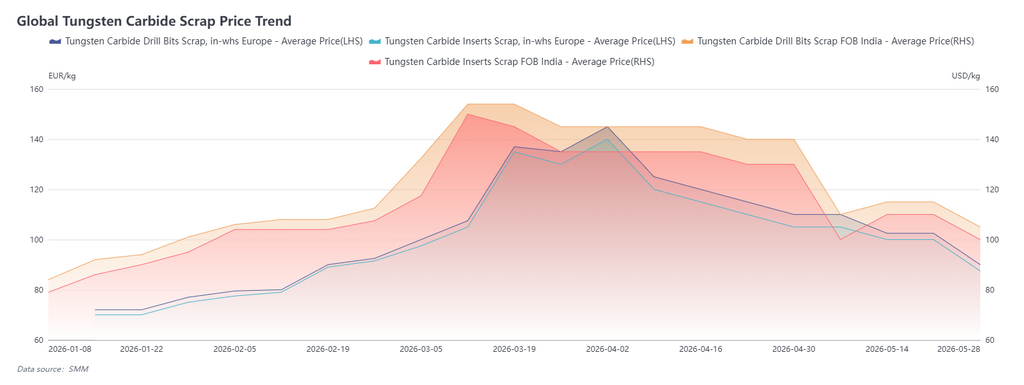

As of May 29, European scrap tungsten carbide inserts were quoted at 85-95 euros/kg, with an average price of 90 euros/kg, down 18% from the beginning of the month; Indian scrap tungsten drill bits FOB were quoted at $100-110/kg, with an average price of $105/kg, down 25% from the beginning of the month.

In May, the European tungsten scrap market saw a significant decline, mainly driven by sentiment spillover from two consecutive months of falling tungsten prices in China. Although local raw material prices in Europe showed no notable changes, large volumes of scrap originated from tool recycling enterprises and traders' earlier stockpiling. In mid-month, when scrap prices fell to around 100 euros/kg, some traders engaged in a price collapse of shipments, pushing prices further down. Looking ahead, as inventory is gradually cleared, coupled with persistently weak end-user tool production and reduced new scrap supply, the European scrap market is expected to gradually stop falling, and supply may tighten.

The Indian tungsten scrap market was significantly influenced by Chinese futures. In early May, driven by a sharp plunge in Chinese prices, Indian scrap prices saw panic-driven markdowns, but actual transactions were scarce, with trading mainly concentrated in India's domestic trade market. Entering mid-to-late May, prices gradually stabilized, with the market awaiting new guidance from Chinese price trends.

China Tungsten Market May Review: Prices Stop Falling and Rebound, Supply-Demand Improvement Boosts Market Sentiment

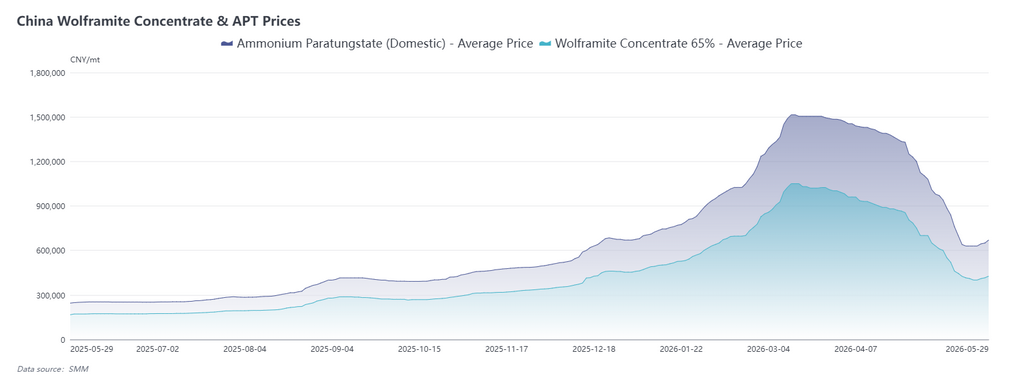

In May 2026, after a cumulative decline of 300,000 yuan/mt, China's 65% wolframite concentrates prices rebounded on May 27, edging up slightly. Miners maintained firm offers, while recent prices showed a daily slight correction trend.

There were two main reasons: first, on the supply side, retail miners' earlier inventory was partially digested, the industry gradually returned to long-term contract mode, and production and sales moved toward balance, driving prices to consolidate at lows on a phased basis; second, inquiry volumes from downstream traders increased recently, and combined with miners' weak willingness to sell at low prices, these factors jointly drove market sentiment to recover.

However, from the end-user perspective, new orders transmitted upward from cemented carbide were insufficient, and finished product inventory pressure at the powder end remained significant. Nevertheless, at month-end, tungsten powder prices rebounded slightly in sync with ore prices, strengthening expectations of prices consolidating at lows. Additionally, this month some mines in major producing areas such as Jiangxi and Hunan entered maintenance phases, with supply mainly concentrated on long-term contracts, significantly boosting market recovery expectations. However, since end-use demand had not yet shown a strong surge, the likelihood of a sharp price rally remained low.

Looking ahead to June, from a supply-demand fundamental perspective, the likelihood of Chinese tungsten prices bottoming out is increasing, with market sentiment simultaneously showing signs of recovery. If domestic tungsten prices continue to edge up, this is also expected to simultaneously stabilize sentiment in the European tungsten market. Going forward, close attention should be paid to mine maintenance and tender developments, as well as changes in end-user restocking pace.