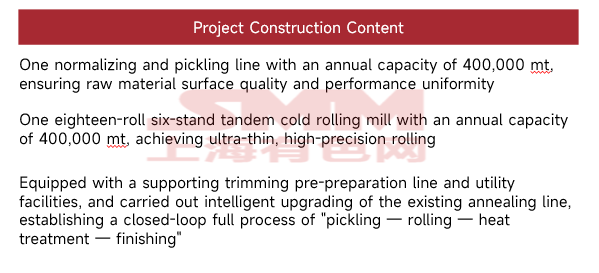

(1) Project Overview

Recently, Bao Gang United Steel (600010), a leading enterprise in China's steel and rare earth industries, officially announced a major investment: the company plans to build a green high-end new energy rare earth silicon steel project in Kundulun District, Baotou City, with a total investment of approximately 1.015 billion yuan, entirely self-funded, to create a world-leading rare earth non-oriented silicon steel production site, precisely targeting demand from high-end sectors such as NEVs, wind power, and high-efficiency industrial motors.

The project is located on the west side of the wide and heavy plate production line at Bao Gang United Steel's thin plate plant. Leveraging Bao Gang's existing production facilities and industrial cluster advantages, the construction period runs from March 2026 to December 2027. The project plans to build an annual 400,000 mt rare earth non-oriented silicon steel production line. Once it reaches full production, it will significantly enhance China's self-sufficient supply capability of high-end silicon steel, breaking the monopoly of ex-China technologies and capacity.

Source: Publicly available data

On the technical level, the core highlight of the project lies in the scaled application of rare earth micro-alloying technology — by precisely adding rare earth elements to non-oriented silicon steel, the technology significantly enhances the magnetic induction performance of the material, reduces iron loss, and addresses the pain points of high-frequency loss and low energy efficiency in traditional silicon steel. This technology originated from Baosteel's years of collaborative innovation through the "industry-academia-research-application" model, leveraging the unique resource advantage of the "iron-rare earth symbiosis" at the Bayan Obo mine. It has completed laboratory and pilot-scale verification and is ready for industrialisation.

The product performance benchmarks against the world's top standards, meeting the stringent requirements of high-frequency, high-efficiency application scenarios such as NEV drive motors, industrial motors, and wind power inverters. Currently, high-end non-oriented silicon steel for NEV drive motors has long relied on imports, and significant supply gaps also exist in the wind power and high-efficiency industrial motor sectors. Once Baosteel's project is implemented, it will effectively fill the capacity gap in China and support the independent controllability of China's new energy industry chain.

(II) Subsequent Impact

Data source: compiled from public data

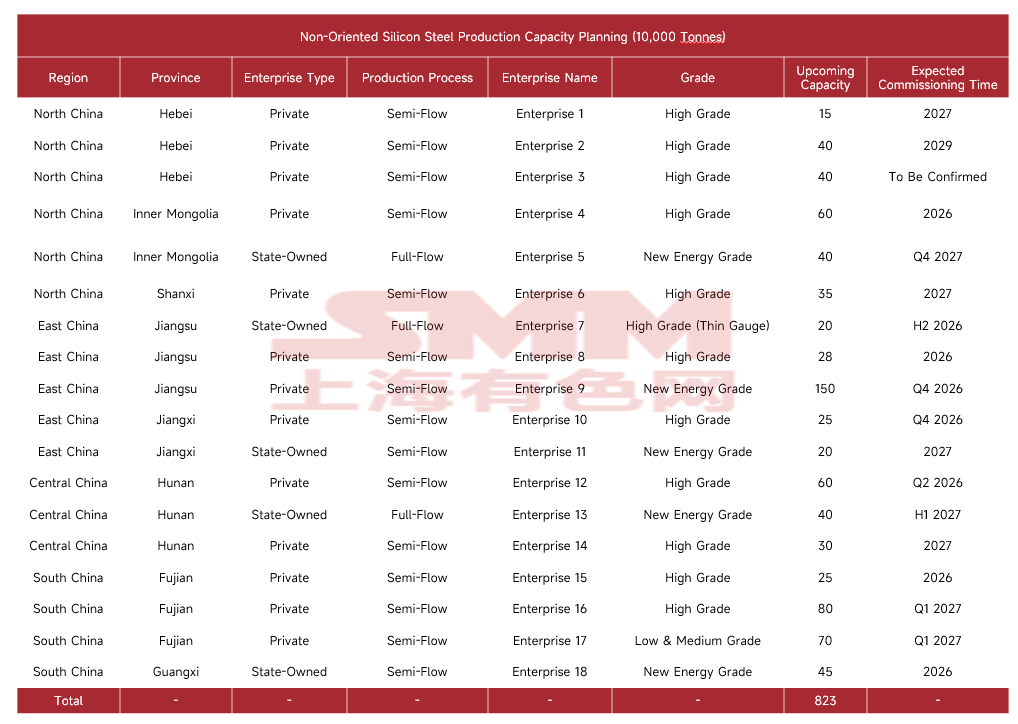

Currently, China's non-oriented silicon steel industry is already mired in a structural predicament of overcapacity, with the supply-demand balance in a state of prolonged fragile imbalance. Baotou Steel's renewed plan to commission new capacity has become yet another heavy weight on the supply side, further exacerbating the already severe surplus.

Capacity currently planned and pending commissioning has reached 8.23 million mt. The pace of supply expansion across the industry has never ceased, and Baotou Steel's additional capacity continues to fuel this round of expansion. Its planned 400,000 mt new energy grade non-oriented silicon steel project, leveraging the industrial advantages of a state-owned fully integrated process, targets the high-value-added segment with intensified investment. This not only directly expands total industry supply but also further intensifies competitive involution in the high-end segment, where players have already begun to crowd into the new energy dedicated grade space.

Commissioning time, Baotou Steel's project is scheduled for commissioning in December 2027, though the timing may fluctuate. This forms a successive wave of impact together with the concentrated capacity release of 600,000 mt in Inner Mongolia and 1.5 million mt in Jiangsu in 2026, subjecting the non-oriented silicon steel industry to sustained heavy pressure on the supply side over the next two years. Industry landscape, as a core state-owned steel enterprise in north China, Baotou Steel's expansion not only amplifies the oversupply pressure in the North China region but also disrupts the regional market's supply-demand balance, driving the surplus impact to spread across the national market.

Against the backdrop of continuously slowing downstream demand growth that struggles to match the pace of capacity expansion, Baotou Steel's renewed commissioning is expected to further intensify the industry's overcapacity tensions, drive market price competition to a more heated level, continuously squeeze industry profit margins, and deepen the industry's predicament of overcapacity.

![[SMM HRC Daily Trading Volume] Spot HRC Trading Weak](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)

![[SMM Sheets & Plates Daily Review] Limited Room for Short-Term Pullback in Sheets & Plates](https://imgqn.smm.cn/usercenter/niwZw20251217171715.jpg)