Chinese stainless steel futures arrested their recent slide this week. The most-active SS2607 contract on the Shanghai Futures Exchange (SHFE) shifted from earlier weakness into a stable, range-bound pattern, driven by expectations around Indonesian industrial policy, and settled at roughly $2,180/mt (RMB 14,800/mt) on May 29.

The week was a tug-of-war between three forces: policy headlines providing a floor, rigid downstream demand offering support, and weak underlying fundamentals capping the upside. Futures firmed on the prospect of tighter Indonesian raw-material supply, while spot prices held broadly steady on low inventories and end-user restocking — even as stainless steel's own supply-demand balance stayed soft.

Macro caution, but policy expectations took the wheel

Overseas sentiment was cautious. Minutes from the U.S. Federal Reserve's April meeting struck a hawkish tone, further cooling expectations of a rate cut this year. Combined with sticky inflation and volatile energy prices, this kept the dollar index and Treasury yields elevated, weighing on commodities broadly.

Domestically, China's Ministry of Commerce said on May 28 that Beijing and Washington had agreed in principle to discuss a reciprocal tariff-reduction framework of comparable scale — $30 billion or more on each side — signaling continued de-escalation.

The decisive driver, though, was industrial policy. Indonesia announced that state-owned enterprises will become the single export channel for commodities including coal, palm oil and ferroalloys. Layered on expectations of tightening nickel ore supply, this raised concerns over forward raw-material costs and partly offset the gloomier macro backdrop — the main reason futures stabilized.

Destocking continues; spot rests on rigid demand

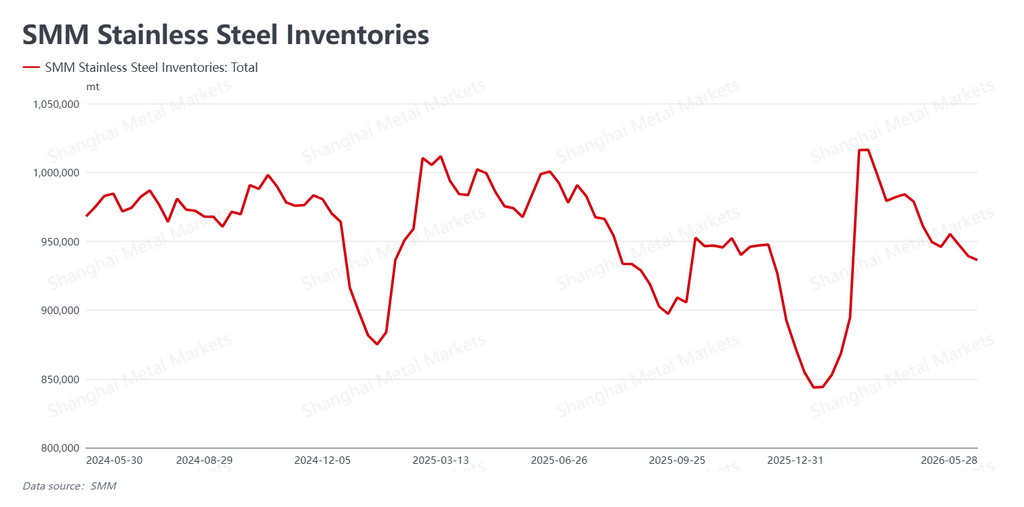

SMM data showed market inventory falling further to 939,200 mt, down 7,900 mt week-on-week. With the traditional off-season approaching in late May, this counter-seasonal drawdown gave spot prices a floor.

Spot stability rested on three factors. End-users stayed cautious on the outlook but kept lifting material for routine needs, so transactions did not stall. Agents and traders, prompted by earlier price cuts, sold actively, accelerating turnover. And with inventories at relatively low levels, limited circulating supply lent prices support.

The caveat: trader sentiment remained weak after the earlier downturn. The steadier spot market leaned on rigid demand and thin inventories, not a genuine return of restocking appetite.

Spot input costs ease, but the forward curve firms

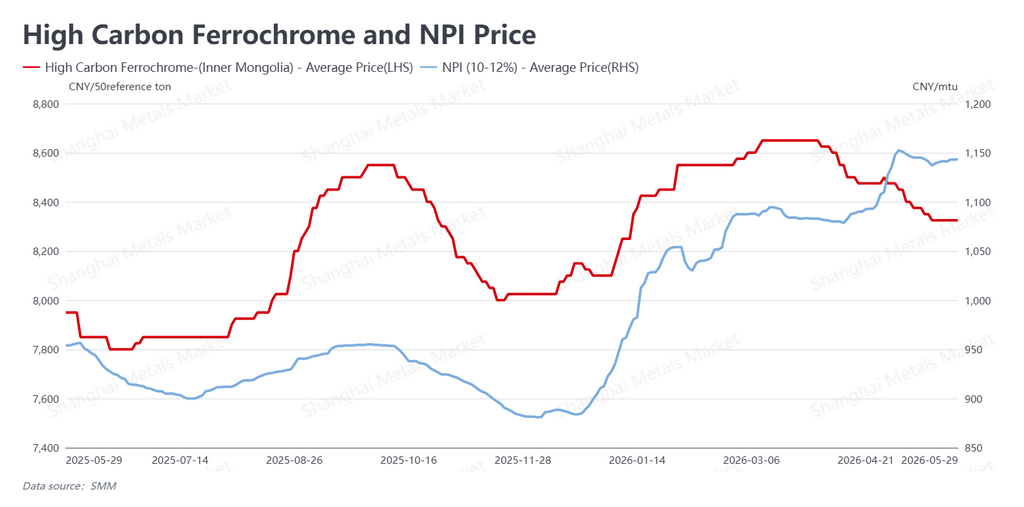

Raw-material spot prices drifted lower, pressured by weak finished-steel prices and squeezed mill margins. High-carbon ferrochrome slipped to $1,226 per 50-base-mt (RMB 8,325 per 50-base-mt) — China's pricing convention for ferrochrome on a 50% chromium-content basis — while Nickel Pig Iron (NPI), the low-grade ferro-nickel feed smelted from laterite ore for Chinese and Indonesian stainless production, edged down to about $168 per nickel point (RMB 1,140.5 per nickel point).

These near-term moves confirm that stainless steel's own fundamentals remain soft. The contrast is that expectations of tighter Indonesian ore supply and centralized ferroalloy export control are lifting the forward cost curve — the core logic behind the week's recovery. Lower input costs gave mills some margin relief, production appetite held, and the medium-term picture of ample supply stayed intact.

Outlook

The week was shaped by two supportive forces — Indonesian policy expectations and a spot-price floor — against a hawkish macro backdrop that capped gains. But this stabilization rests largely on external headlines; the underlying fundamentals are still weak.

As the seasonal demand lull nears, two questions will decide whether prices hold: whether downstream rigid demand keeps flowing, and whether Indonesian policy expectations translate into real cost increases. Expect SS2607 to stay range-bound in the near term, with headlines and fundamentals pulling against each other.

![[SMM Nickel Market Flash] Indonesia Nickel Industry Seeks Clarity on Whether NPI Falls Under Mandatory DSI Export Rule](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)

![[SMM Nickel Market Flash] Harita Nickel Reports Q1 2026 Revenue of Rp6.81T (~$418M), Full-Year 2025 at Rp29.63T](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Nickel Market Flash] First Atlantic Gets Newfoundland Permit to Advance Awaruite Ni-Co Project and Geologic H2 Test](https://imgqn.smm.cn/usercenter/sKmGT20251217171733.jpg)