SMM May 27 News:

As of May 26, the Shanghai-LME zinc price ratio stood at 6.97, continuing its downward trend from 7.4 recorded in late March, which has led to a widening import loss of refined zinc ingots in China. According to calculations by Shanghai Metals Market (SMM), the current import loss of China’s refined zinc ingots has expanded to approximately RMB 3,800 per metric ton of metal. While still some distance from the 2025 historical trough of RMB -6,393 per metric ton, the current loss level has fallen into a historically low range over the past decade, second only to the lows seen in 2022 and 2025. With the Shanghai-LME zinc ratio gradually approaching its historical lower bound, market attention toward domestic-overseas reverse spread arbitrage for zinc has continued to rise.

A clear divergence of strong offshore and weak onshore zinc prices has dominated the market since the start of the year. The overseas supply side faced frequent disruptions throughout Q1. Persistent flooding in Australia hampered zinc shipment schedules, while geopolitical tensions between the US and Iran disrupted zinc concentrate exports from Iran. Entering Q2, operational incidents further tightened overseas supply: an explosion at the Kazzinc smelter and a fire at Nexa Resources’ smelter triggered successive supply disruptions. These recurring supply-side disturbances have driven a rally in LME zinc prices and continuously depressed the onshore-offshore price ratio.

Fundamental supply-demand differentials between global and domestic markets further reinforce the price divergence. SMM data indicates that the global refined zinc market will register a surplus of over 100,000 metric tons in 2026, with the surplus concentrated entirely in the Chinese market, whereas the overseas refined zinc market remains broadly balanced. This structural imbalance is fully reflected in inventory metrics.

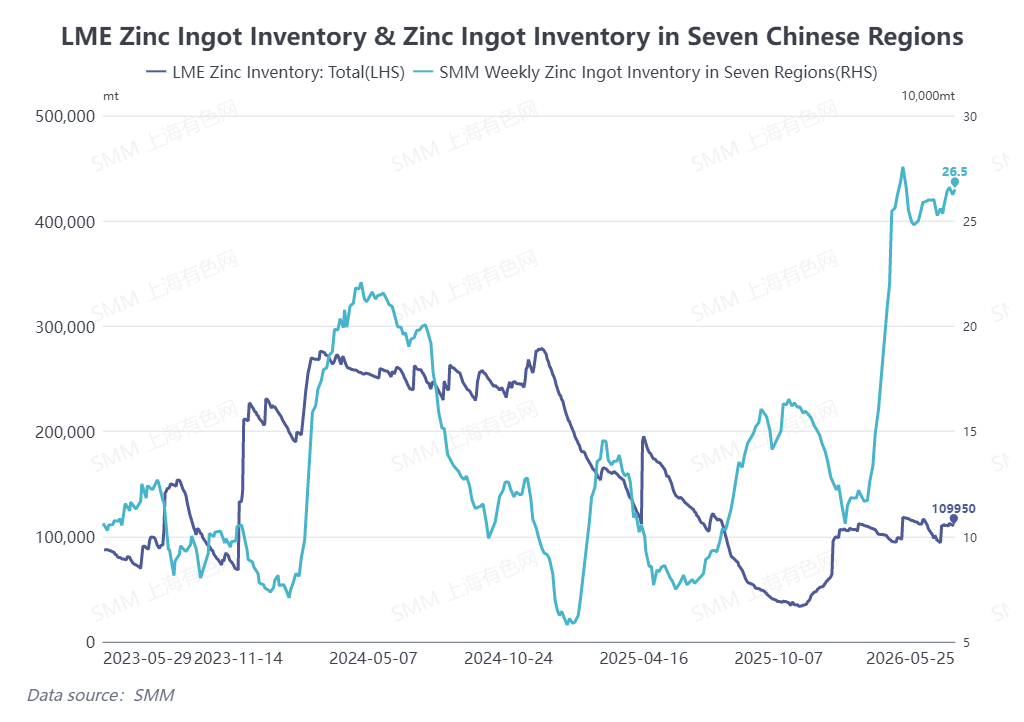

Driven by post-Spring Festival inventory accumulation, SMM’s seven-region domestic zinc ingot inventory has climbed markedly since early 2026 and failed to deliver a notable destocking cycle amid sluggish domestic zinc consumption. As of May 25, China’s seven-region zinc ingot inventory totalled 265,000 metric tons, hitting a four-year year-on-year high. In contrast, LME zinc inventories have remained subdued and range-bound, oscillating around 100,000 metric tons from January to May at a relatively low historical level. Against this backdrop, China’s refined zinc imports have remained in deficit since the start of the year, with import losses widening significantly in Q2.

With refined zinc imports stuck in deep deficit and the Shanghai-LME zinc ratio lingering at a depressed level, market interest in zinc reverse spread arbitrage strategies has surged recently. On the fundamental front, industry operating indicators point to tightening raw material supply and shrinking smelting margins.

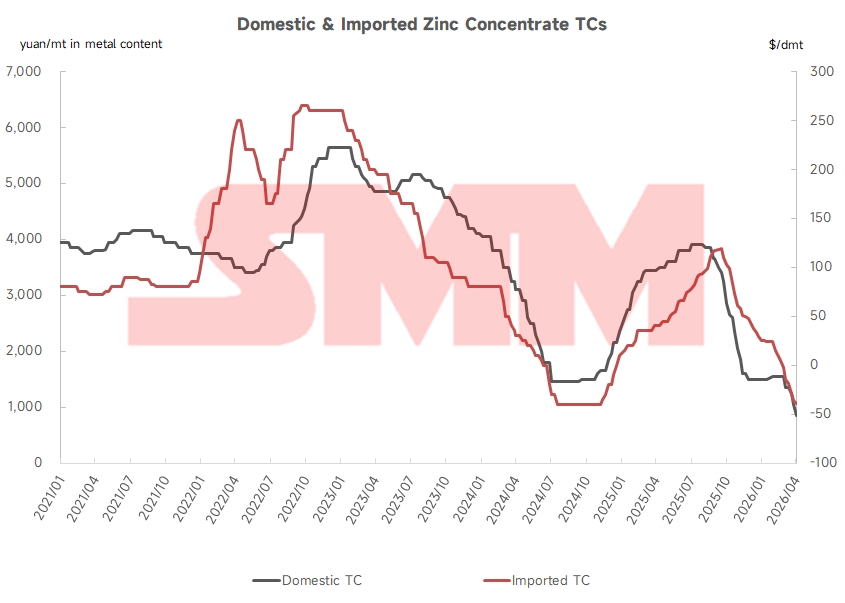

As of May 22, the domestic zinc concentrate treatment charge (TC) dropped to RMB 400 per metric ton of metal, refreshing historical lows repeatedly. Meanwhile, the import zinc concentrate TC fell to USD -56.25 per dry metric ton, with negative margins continuing to deepen, signalling persistent tightness in the zinc concentrate market. In addition, the rally in domestic sulfuric acid prices stalled across multiple regions in May, with spot prices correcting sharply in some provinces. This has further compressed the profit margins of domestic zinc smelters, curbing production enthusiasm.

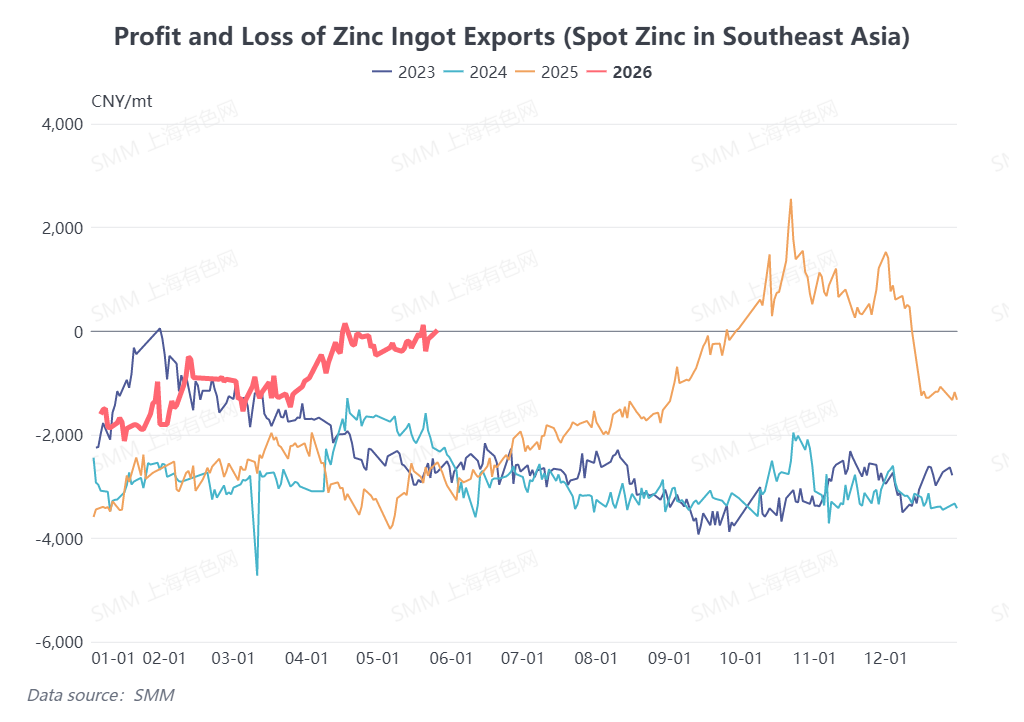

Maintenance schedules for domestic zinc smelters are set to increase in June and July, strengthening market expectations of onshore supply contraction. On the trade front, SMM data shows that as of May 25, China’s spot zinc ingot export window to Southeast Asian markets has reached a critical opening threshold, while exports for LME warrant delivery to Southeast Asia still carry a loss of approximately RMB 500 per metric ton.Looking ahead, if the onshore-offshore price ratio deteriorates further, sluggish domestic seasonal consumption and elevated domestic zinc inventories will drive traders to ramp up zinc ingot exports. Increased export volumes will underpin domestic zinc prices and facilitate a subsequent recovery in the Shanghai-LME zinc price ratio.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)