SMM News 27 พ.ค.:

ตลาดโลหะ:

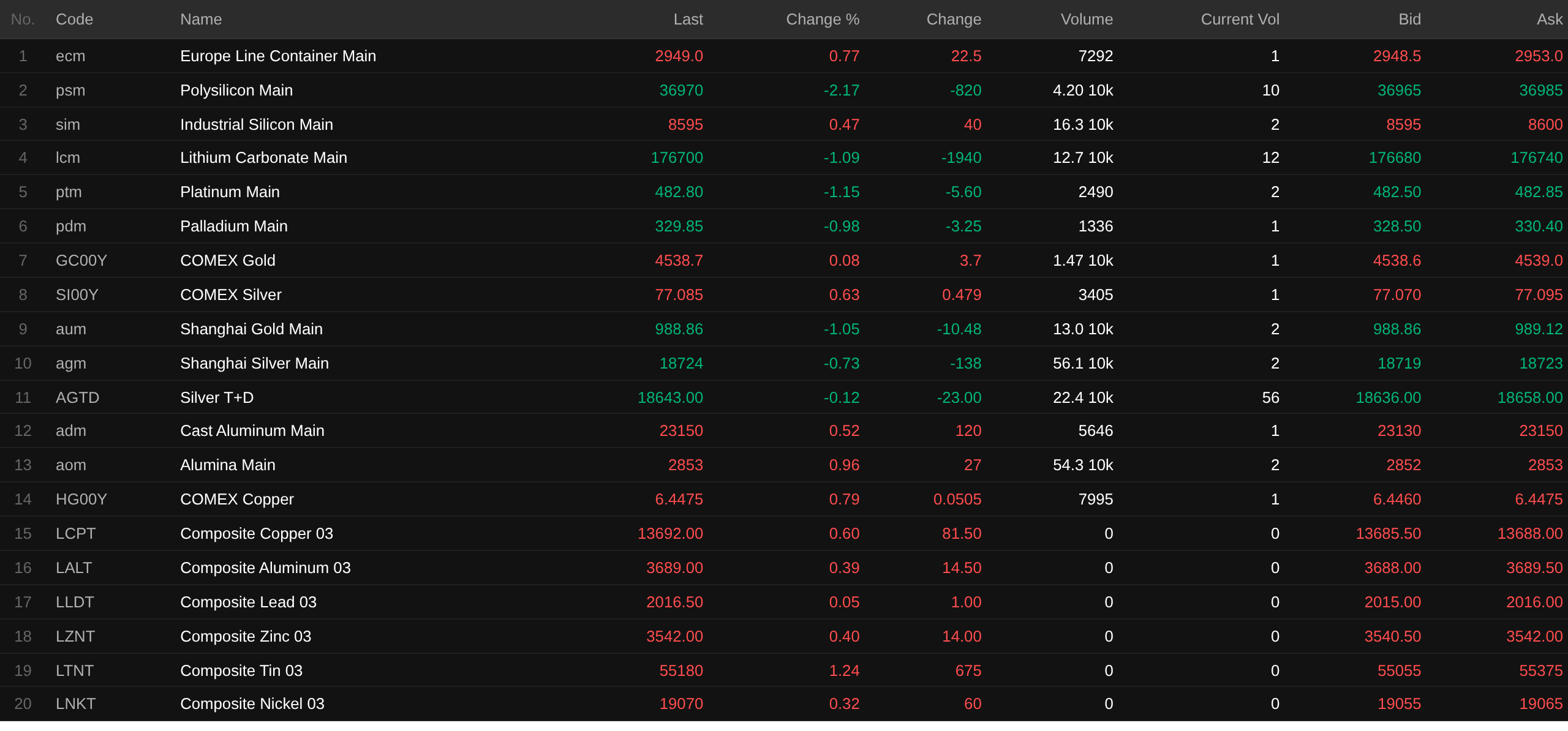

ณ ช่วงปิดตลาดภาคเช้า โลหะพื้นฐานในประเทศส่วนใหญ่ปรับตัวขึ้น ขณะที่ทองแดง SHFE ปรับลงเล็กน้อย อะลูมิเนียม SHFE เพิ่มขึ้น 0.8% ตะกั่ว SHFE เพิ่มขึ้น 0.33% สังกะสี SHFE ลดลง 0.72% ดีบุก SHFE เพิ่มขึ้น 0.63% นิกเกิล SHFE เพิ่มขึ้น 1.91%

นอกจากนี้ สัญญาฟิวเจอร์สอะลูมิเนียมหล่อที่ซื้อขายมากที่สุดเพิ่มขึ้น 0.52% สัญญาอะลูมินาที่ซื้อขายมากที่สุดเพิ่มขึ้น 0.96% สัญญาลิเทียมคาร์บอเนตที่ซื้อขายมากที่สุดลดลง 1.09% สัญญาซิลิคอนเมทัลที่ซื้อขายมากที่สุดเพิ่มขึ้น 0.47% สัญญาฟิวเจอร์สโพลีซิลิคอนที่ซื้อขายมากที่สุดลดลง 2.17%

โลหะกลุ่มเหล็กส่วนใหญ่ปรับตัวลง แร่เหล็กลดลง 0.19% เหล็กเส้นลดลง 0.69% เหล็กแผ่นรีดร้อนลดลง 0.44% และเหล็กกล้าไร้สนิมเพิ่มขึ้น 1.49% ถ่านโค้กและโค้ก: สัญญาถ่านโค้กที่ซื้อขายมากที่สุดลดลง 1.48% และสัญญาโค้กที่ซื้อขายมากที่สุดลดลง 1.77%

โลหะพื้นฐานต่างประเทศ ณ เวลา 11:38 น. โลหะ LME ปรับตัวขึ้นทั้งกระดาน ทองแดง LME เพิ่มขึ้น 0.6% อะลูมิเนียม LME เพิ่มขึ้น 0.39% ตะกั่ว LME เพิ่มขึ้น 0.05% สังกะสี LME เพิ่มขึ้น 0.4% ดีบุก LME เพิ่มขึ้น 1.24% นิกเกิล LME เพิ่มขึ้น 0.32%

โลหะมีค่า ณ เวลา 11:38 น. ทองคำ COMEX เพิ่มขึ้น 0.08% เงิน COMEX เพิ่มขึ้น 0.63% โลหะมีค่าในประเทศ: สัญญาทองคำ SHFE ที่ซื้อขายมากที่สุดลดลง 1.05% สัญญาเงิน SHFE ที่ซื้อขายมากที่สุดลดลง 0.73%

นอกจากนี้ ณ ช่วงปิดตลาดภาคเช้า สัญญาฟิวเจอร์สแพลทินัมที่ซื้อขายมากที่สุดลดลง 1.15% และสัญญาฟิวเจอร์สแพลเลเดียมที่ซื้อขายมากที่สุดลดลง 0.98%

ณ ช่วงปิดตลาดภาคเช้า สัญญาดัชนีค่าระวางตู้คอนเทนเนอร์ยุโรปที่ซื้อขายมากที่สุดเพิ่มขึ้น 0.77% ปิดที่ 2,949 จุด

ณ เวลา 11:38 น. วันที่ 27 พ.ค. ราคาฟิวเจอร์สภาคเช้าของสัญญาที่คัดเลือก:

สินค้าสปอตและปัจจัยพื้นฐาน

อะลูมินา:สถิติของ SMM แสดงว่าขนาดของโครงการอะลูมินาที่อยู่ระหว่างก่อสร้างและวางแผนในกินีมีมูลค่าเกิน...

ด้านมหภาค

จีน:

[NBS: ม.ค.-เม.ย. กำไรของวิสาหกิจอุตสาหกรรมขนาดใหญ่ของจีนเพิ่มขึ้น 18.2% กำไรภาคโลหะอโลหะเพิ่มขึ้นพุ่ง 117.8%] ข้อมูลของ NBS แสดงว่าในช่วง ม.ค.-เม.ย. กำไรรวมของวิสาหกิจอุตสาหกรรมขนาดใหญ่ของจีนอยู่ที่ 2.44 ล้านล้านหยวน เพิ่มขึ้น 18.2% เมื่อเทียบรายปีในช่วงเดือนมกราคมถึงเมษายน ภาคเหมืองแร่มีกำไร 361,840 ล้านหยวน เพิ่มขึ้น 26.0% เมื่อเทียบกับช่วงเดียวกันของปีก่อน ภาคการผลิตมีกำไร 1.80 ล้านล้านหยวน เพิ่มขึ้น 20.4% และภาคการผลิตและจัดจำหน่ายไฟฟ้า ความร้อน ก๊าซ และน้ำมีกำไร 272,010 ล้านหยวน ลดลง 1.9% ในช่วงเดือนมกราคมถึงเมษายน ความสามารถในการทำกำไรของอุตสาหกรรมหลักมีดังนี้: การถลุงและแปรรูปโลหะที่ไม่ใช่เหล็ก (เพิ่มขึ้น 1.2 เท่าเมื่อเทียบกับปีก่อน) การผลิตคอมพิวเตอร์ การสื่อสาร และอุปกรณ์อิเล็กทรอนิกส์อื่นๆ (เพิ่มขึ้น 1.1 เท่า) การผลิตวัตถุดิบเคมีและผลิตภัณฑ์เคมี (เพิ่มขึ้น 73.4%) การทำเหมืองและล้างถ่านหิน (เพิ่มขึ้น 21.0%) สิ่งทอ (เพิ่มขึ้น 11.2%) การสกัดปิโตรเลียมและก๊าซธรรมชาติ (เพิ่มขึ้น 8.1%) การแปรรูปปิโตรเลียม ถ่านหิน และเชื้อเพลิงอื่นๆ (พลิกจากขาดทุนเป็นกำไร) การผลิตอุปกรณ์ทั่วไป (ลดลง 0.6%) การผลิตและจัดจำหน่ายไฟฟ้าและความร้อน (ลดลง 2.5%) การผลิตอุปกรณ์เฉพาะทาง (ลดลง 7.2%) การผลิตเครื่องจักรและอุปกรณ์ไฟฟ้า (ลดลง 11.4%) การแปรรูปอาหารจากผลิตผลทางการเกษตรและผลพลอยได้ (ลดลง 11.8%) การผลิตรถยนต์ (ลดลง 16.8%) ผลิตภัณฑ์แร่อโลหะ (ลดลง 50.7%) และการถลุงและแปรรูปโลหะเหล็ก (ลดลง 51.5%)

[ธนาคารกลางจีนดำเนินการรีเวิร์สรีโปในตลาดเปิดมูลค่า 177,600 ล้านหยวน อัดฉีดสุทธิ 127,600 ล้านหยวนในวันเดียว] ธนาคารกลางจีนดำเนินการรีเวิร์สรีโป 7 วันในตลาดเปิดมูลค่า 177,600 ล้านหยวน อัตราดอกเบี้ย 1.40% ไม่เปลี่ยนแปลงจากวันก่อนหน้า รีเวิร์สรีโปครบกำหนดวันนี้ 50,000 ล้านหยวน

ดอลลาร์สหรัฐ:

ณ เวลา 11:38 น. ดัชนีดอลลาร์สหรัฐลดลง 0.05% อยู่ที่ 99.1 ตามรายงานของนิกเคอิ แคชคารีแห่งเฟดระบุว่าเฟดอาจดำเนินการขึ้นอัตราดอกเบี้ย "หลายครั้งต่อเนื่อง" เพื่อรับมือกับความกังวลด้านเงินเฟ้อที่เกิดจากสถานการณ์ตะวันออกกลาง ในการประชุม FOMC ปลายเดือนเมษายน เฟดคงอัตราดอกเบี้ยไว้ไม่เปลี่ยนแปลง แคชคารีและเจ้าหน้าที่อีกสองคนคัดค้านการตัดสินใจที่จะรวมถ้อยคำในแถลงการณ์ของเฟดที่ส่งสัญญาณการผ่อนคลายนโยบายการเงินในอนาคต ในการสัมภาษณ์เป็นลายลักษณ์อักษร แคชคารีกล่าวว่า: "ผมคิดว่าการปรับอัตราดอกเบี้ยครั้งต่อไปอาจเป็นการลดดอกเบี้ย หรืออาจเป็นการขึ้นดอกเบี้ย" เขาใช้ถ้อยคำนี้เพื่อแสดงมุมมองที่แตกต่าง แคชคารีกล่าวว่าผลลัพธ์จะขึ้นอยู่กับแนวโน้มเงินเฟ้อ ซึ่งขึ้นอยู่กับว่าช่องแคบฮอร์มุซจะเปิดใช้งานอีกครั้งในเร็วๆ นี้หรือยังคงปิดอยู่จริงเนื่องจากโครงสร้างพื้นฐานในภูมิภาคได้รับความเสียหายเพิ่มเติม ซึ่งกรณีหลังจะทำให้วิกฤตพลังงานโลกรุนแรงขึ้น แคชคารีกล่าวว่าสิ่งที่น่ากังวลคือการคาดการณ์เงินเฟ้อระยะยาวของภาคธุรกิจและครัวเรือน "อาจหลุดจากกรอบยึดเหนี่ยว" เขากล่าวว่า FOMC "อาจจำเป็นต้องตอบสนองอย่างเข้มแข็ง" และการขึ้นดอกเบี้ย หรือแม้แต่การขึ้นดอกเบี้ยหลายครั้งต่อเนื่อง อาจเป็นมาตรการที่จำเป็น

ตามข้อมูล CME "FedWatch": ความน่าจะเป็นที่เฟดจะคงอัตราดอกเบี้ยไว้จนถึงเดือนมิถุนายนอยู่ที่ 99.2% โดยมีความน่าจะเป็น 0.8% ที่จะลดดอกเบี้ยสะสม 25 จุดพื้นฐาน ความน่าจะเป็นที่เฟดจะคงอัตราดอกเบี้ยไว้จนถึงเดือนกรกฎาคมอยู่ที่ 88.6% โดยมีความน่าจะเป็น 11.3% ที่จะขึ้นดอกเบี้ยสะสม 25 จุดพื้นฐาน และความน่าจะเป็น 0% ที่จะลดดอกเบี้ยสะสม 25 จุดพื้นฐาน (Jin10 Data)

รายงานวิจัยของ CITIC Securities ระบุว่าความยืดหยุ่นของเศรษฐกิจโลกกำลังถูกทดสอบจากความขัดแย้งในตะวันออกกลาง ขณะที่มีแสงสว่างริบหรี่สำหรับการกลับมาเดินเรือผ่านช่องแคบฮอร์มุซ เศรษฐกิจสหรัฐมีแนวโน้มเติบโตอย่างอ่อนๆ แต่ไม่สม่ำเสมอในปีนี้ จังหวะการฟื้นตัวที่อ่อนแอของสหภาพยุโรปกำลังถูกชะลอ และอุปสงค์ภาคเอกชนของญี่ปุ่นหลีกเลี่ยงไม่ได้ที่จะถูกกระทบจากการขาดแคลนพลังงาน ราคาน้ำมันที่สูงกำลังผลักดันเงินเฟ้อทั่วโลกให้สูงขึ้น โดยอัตราเงินเฟ้อทั่วไปในยุโรปและสหรัฐมีแนวโน้มผันผวนอยู่ในระดับสูงในปีนี้ ขณะที่อัตราเงินเฟ้อทั่วไปของญี่ปุ่นอาจยังคงเคลื่อนไหวอย่างอ่อนๆ เฟดอาจไม่ลดดอกเบี้ยเลยในปีนี้ ขณะที่การขึ้นดอกเบี้ยของธนาคารกลางยุโรปและญี่ปุ่นใกล้จะเกิดขึ้น และท่าทีการคลังแบบ "ไร้ขอบเขต" ของวงการเมืองญี่ปุ่นและยุโรปอาจเป็นแหล่งความเสี่ยงของตลาดในปีนี้ เรายังคงมุมมองว่าหุ้นสหรัฐจะให้ผลตอบแทนดีกว่าพันธบัตรรัฐบาลสหรัฐ และดัชนีดอลลาร์สหรัฐจะได้รับแรงหนุน ขณะที่ราคาทองคำคาดว่าจะทะลุกรอบปัจจุบันเมื่อความเสี่ยงปลายด้านเงินเฟ้อคลี่คลาย

สกุลเงินอื่นๆ:

ธนาคารกลางนิวซีแลนด์ (RBNZ) คงอัตราดอกเบี้ยไว้ไม่เปลี่ยนแปลงเป็นการประชุมที่สามติดต่อกัน โดยเลือกที่จะติดตามผลกระทบของวิกฤตพลังงานโลกต่อการบริโภคในประเทศและเงินเฟ้อระยะกลางต่อไป คณะกรรมการนโยบายการเงินของ RBNZ เมื่อวันพุธคงอัตราดอกเบี้ยนโยบาย (OCR) ไว้ที่ 2.25% สอดคล้องกับความคาดหมายของตลาด ประมาณการล่าสุดของ RBNZ แสดงให้เห็นว่ามีความเป็นไปได้สูงขึ้นที่จะขึ้นดอกเบี้ยอย่างน้อยสองครั้ง ครั้งละ 25 จุดพื้นฐานก่อนสิ้นปี ในแถลงการณ์หลังการประชุม RBNZ ระบุว่า: "โดยรวมแล้ว OCR มีแนวโน้มที่จะต้องปรับขึ้นเร็วกว่าและมากกว่าที่คาดการณ์ไว้ในแถลงการณ์นโยบายการเงินเดือนกุมภาพันธ์" "จังหวะการขึ้นดอกเบี้ยจะขึ้นอยู่กับผลกระทบเปรียบเทียบระหว่างพฤติกรรมค่าจ้างและการตั้งราคาที่คงอยู่ กับกิจกรรมทางเศรษฐกิจที่อ่อนแอลง ต่อแรงกดดันเงินเฟ้อระยะกลาง" หลังจากแถลงการณ์ NZD/USD ปรับตัวขึ้น (Jin10 Data)

ผู้ว่าการธนาคารกลางญี่ปุ่น (BoJ) อุเอดะ คาซูโอะ กล่าวว่าจำเป็นต้องเฝ้าระวังผลกระทบของราคาน้ำมันที่พุ่งสูงต่อแนวโน้มเงินเฟ้อพื้นฐาน แต่ไม่ได้ส่งสัญญาณชัดเจนว่าปัจจัยนี้จะมีอิทธิพลต่อผลการประชุมนโยบายเดือนหน้าอย่างไร อุเอดะกล่าวเมื่อวันพุธว่า: "ประสบการณ์ของญี่ปุ่นแสดงให้เห็นว่าวิกฤตราคาน้ำมันไม่เคยเป็นเพียงวิกฤตราคาน้ำมัน แต่เป็นการทดสอบกลไกเงินเฟ้อทั้งระบบ" เมื่อทบทวนผลกระทบของวิกฤตน้ำมันตั้งแต่ทศวรรษ 1970 เขากล่าวว่า: "ที่จริงแล้วเรากำลังประสบกับวิกฤตราคาน้ำมันครั้งที่ห้า" "หากวิกฤตชั่วคราวเปลี่ยนแปลงค่าจ้าง การคาดการณ์เงินเฟ้อ และพฤติกรรมการตั้งราคาของภาคธุรกิจ ก็อาจพัฒนาเป็นเงินเฟ้อที่ยืดเยื้อ" อุเอดะไม่ได้ส่งสัญญาณโดยตรงเกี่ยวกับทิศทางนโยบายในอนาคต แต่เนื่องจากถ้อยแถลงของเขาสะท้อนความกังวลเกี่ยวกับผลกระทบของราคาน้ำมันที่สูง ตลาดอาจเพิ่มการคาดเดาเกี่ยวกับโอกาสการขึ้นดอกเบี้ยในการประชุม BoJ เดือนมิถุนายน การกำหนดราคาในตลาดสวอปข้ามคืนแสดงให้เห็นว่าเทรดเดอร์ให้ความน่าจะเป็นประมาณ 75% ที่ BoJ จะขึ้นดอกเบี้ย 25 จุดพื้นฐานในเดือนหน้า (Jin10 Data)

อัตราเงินเฟ้อพื้นฐานเดือนเมษายนของออสเตรเลียยังคงอยู่เหนือขอบบนของกรอบเป้าหมายของธนาคารกลางออสเตรเลีย (RBA) ยิ่งตอกย้ำความคาดหมายของตลาดว่า RBA จะคงท่าทีเข้มงวดหลังจากขึ้นดอกเบี้ยติดต่อกันในปีนี้ ข้อมูลเมื่อวันพุธแสดงให้เห็นว่าตัวชี้วัดเงินเฟ้อพื้นฐานที่จับตามองอย่างใกล้ชิด ได้แก่ อัตราเงินเฟ้อเฉลี่ยตัดปลายรายปีที่ไม่รวมรายการผันผวน เพิ่มขึ้น 3.4% เมื่อเทียบกับปีก่อน สอดคล้องกับความคาดหมายของนักเศรษฐศาสตร์ RBA ตั้งเป้าให้เงินเฟ้ออยู่ใกล้จุดกึ่งกลางของกรอบเป้าหมาย 2%-3% ตลาดสวอปอัตราดอกเบี้ยปัจจุบันกำหนดราคาความน่าจะเป็นของการขึ้นดอกเบี้ยอีกครั้งในเดือนสิงหาคมอยู่ที่ประมาณ 50% ลดลงจาก 64% ก่อนการเปิดเผยข้อมูล ภายใต้แรงกดดันสองทางจากต้นทุนการกู้ยืมที่สูงและราคาเชื้อเพลิงที่พุ่งสูงจากสงครามอิหร่าน เศรษฐกิจออสเตรเลียเริ่มแสดงสัญญาณอ่อนแอ อัตราการว่างงานเดือนเมษายนเพิ่มขึ้นสู่ระดับสูงสุดในรอบสี่ปีครึ่ง ขณะที่ประมาณหนึ่งในสามของธุรกิจรายงานรายได้ลดลงในช่วงสี่สัปดาห์ที่ผ่านมา และครึ่งหนึ่งรายงานต้นทุนดำเนินงานที่เพิ่มขึ้น ตลาดคาดกันอย่างกว้างขวางว่าหลังจากขึ้นดอกเบี้ยในการประชุมทั้งสามครั้งก่อนหน้าในปีนี้ RBA จะคงอัตราดอกเบี้ยนโยบายไว้ที่ 4.35% ในเดือนมิถุนายน ซู-เอลเลน ลุค หัวหน้าสถิติราคาของสำนักงานสถิติออสเตรเลีย กล่าวว่า: "ราคาเชื้อเพลิงรถยนต์ในปัจจุบันยังคงสูงกว่าก่อนเกิดความขัดแย้งในตะวันออกกลาง 23.5% ผลกระทบของราคาน้ำมันที่สูงขึ้นยังสะท้อนในสินค้าและบริการที่มีต้นทุนการขนส่งและโลจิสติกส์สูงขึ้น" (Jin10 Data)

ข้อมูล:

วันนี้จะมีการเปิดเผยการตัดสินใจอัตราดอกเบี้ยของ RBNZ ณ วันที่ 27 พฤษภาคม ดัชนีความเชื่อมั่นนักลงทุน ZEW เดือนพฤษภาคมของสวิตเซอร์แลนด์ การเปลี่ยนแปลงการจ้างงาน ADP รายสัปดาห์ของสหรัฐสำหรับสัปดาห์สิ้นสุดวันที่ 9 พฤษภาคม และดัชนีภาคการผลิต Richmond Fed เดือนพฤษภาคมของสหรัฐ เป็นต้น นอกจากนี้ ควรจับตา: ผู้ว่าการธนาคารกลางญี่ปุ่น อุเอดะ คาซูโอะ กล่าวสุนทรพจน์ในการประชุมนโยบายการเงินที่จัดโดย BOJ; RBNZ เปิดเผยการตัดสินใจอัตราดอกเบี้ยและแถลงการณ์นโยบายการเงิน; ผู้ว่าการ RBNZ เบรแมนจัดแถลงข่าวนโยบายการเงิน

น้ำมันดิบ:

ณ เวลา 11:38 น. ราคาน้ำมันทั้งสองเกณฑ์อ้างอิงปรับตัวลดลง โดย WTI ลดลง 2.03% และเบรนท์ลดลง 1.75% ราคาน้ำมันร่วงลงในช่วงเช้าของตลาดเอเชีย ขณะที่เทรดเดอร์ชั่งน้ำหนักโอกาสของข้อตกลงสหรัฐ-อิหร่าน น้ำมันดิบเบรนท์สัญญาเดือนถัดไปปรับตัวลดลง แม้จะมีการปะทุของการสู้รบอีกครั้ง แต่ยังคงมีความหวังสำหรับข้อตกลงเปิดช่องแคบฮอร์มุซ เตหะรานส่งสัญญาณว่าการโจมตีจะไม่ทำให้การเจรจาตกราง ขณะที่รัฐมนตรีต่างประเทศสหรัฐ รูบิโอ กล่าวว่าจะใช้เวลาอีกไม่กี่วันในการสรุปข้อตกลงที่อาจเกิดขึ้น ความไม่แน่นอนยังคงสูง เคียแรน ทอมกินส์ จาก Capital Economics ระบุว่าแม้ข้อมูลออปชันน้ำมันดิบบ่งชี้ว่านักลงทุนคาดว่าราคาจะปรับตัวลดลงในสามเดือนข้างหน้า แต่ความเชื่อมั่นอยู่ในระดับต่ำผิดปกติ เขากล่าวว่าออปชันบ่งชี้ว่านักลงทุนมองว่าการกลับมาส่งอุปทานผ่านช่องแคบอย่างรวดเร็วเป็นผลลัพธ์ที่มีโอกาสมากที่สุด แต่ความคาดหมายโดยนัยบ่งชี้ว่ามีความน่าจะเป็น 37% ที่ราคาน้ำมันจะเกิน 100 ดอลลาร์ต่อบาร์เรลในสามเดือน (Zhitong Finance)

เมื่อค่ำวันที่ 26 พฤษภาคม ตามเวลาท้องถิ่น กรมประชาสัมพันธ์ของกองทัพเรือกองกำลังพิทักษ์การปฏิวัติอิสลาม (IRGC) ประกาศว่าในช่วง 24 ชั่วโมงที่ผ่านมา เรือ 25 ลำ รวมถึงเรือบรรทุกน้ำมัน เรือคอนเทนเนอร์ และเรือพาณิชย์อื่นๆ ผ่านช่องแคบฮอร์มุซโดยได้รับอนุญาต ภายใต้การประสานงานและการรับประกันความปลอดภัยของกองทัพเรือ IRGC ขณะเดียวกัน กองทัพเรือ IRGC ระบุว่ากำลังใช้การควบคุม "อย่างมีประสิทธิภาพและเด็ดขาด" เหนือช่องแคบฮอร์มุซ และการกระทำรุกรานใดๆ จะถูกตอบโต้อย่างรุนแรง (CCTV News) (Jin10 Data APP)

ภาพรวมตลาดสปอต:

►

►

►

►

►

►

►

►

►

►

►

►

►

![[SMM Flash News] อินโดนีเซียเสนอเพิ่มปริมาณน้ำมันดีเซลและน้ำมันก๊าดที่ได้รับเงินอุดหนุนสำหรับปี 2027](https://imgqn.smm.cn/usercenter/BVoXk20251217171736.jpg)

![อลูมิเนียมสปอตร่วงลงอย่างกะทันหัน, ในขณะที่การซื้อขายโดยรวมเป็นที่น่าพอใจ [SMM South China Aluminum Spot Daily Review]](https://imgqn.smm.cn/usercenter/TFHUe20251217171651.jpg)