The global copper scrap market is entering a period of structural tightening as geopolitical tensions and industrial policy increasingly reshape trade flows. The relationship between the United States and China sits at the center of this transition, particularly as Washington considers restricting exports of high-quality copper scrap in 2027 while China remains heavily dependent on imported secondary copper feedstock.

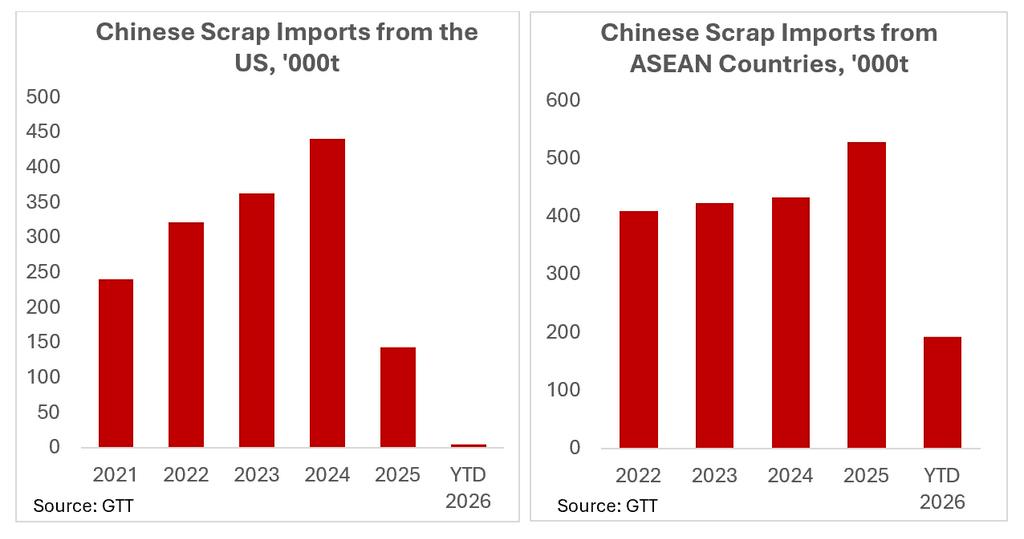

China’s copper scrap imports remained strong in 2024 at 441,080 MT, underscoring continued demand from secondary refiners serving the EV, renewable energy, power grid, and manufacturing sectors. However, imports have collapsed in 2025 to 143,271 MT, with current projections for 2026 falling further to just 5,305 MT. The sharp decline signals a rapid deterioration in China’s direct access to imported scrap feedstock amid rising geopolitical friction and tariffs. China’s existing 10% tariff on US-origin scrap has already reduced the competitiveness of direct shipments, although clean high-grade material has continued to move because of favorable processing economics.

Trade flows indicate that copper scrap is increasingly being rerouted through Southeast Asia rather than moving directly from the United States into China. US copper scrap exports to ASEAN rose from 170,687 tonnes in 2024 to 222,993 tonnes in 2025, while Chinese imports of copper scrap from ASEAN increased from 434,176 tonnes to 529,345 tonnes over the same period. The correlation strongly suggests ASEAN is emerging as a critical intermediary hub for scrap aggregation, processing, blending, and re-export into China.

This shift reflects a broader restructuring of the global scrap trade as market participants adapt to tariffs, geopolitical risk, and the growing probability of tighter controls on high-quality US scrap exports. Countries such as Malaysia, Thailand, and Vietnam are increasingly functioning as alternative routing channels within the global secondary copper supply chain.

The timing is significant because the United States continues to export around 1 million tonnes of copper scrap globally in 2025 while domestic secondary refinery production remains limited at approximately 50kt. This imbalance is becoming central to the policy debate in Washington. As US demand for copper accelerates through grid modernization, electrification, AI-driven data center expansion, and defense manufacturing, policymakers are increasingly questioning whether high-grade recyclable copper should continue flowing overseas while the US remains dependent on imported refined copper.

Current policy discussions focus on retaining a larger share of premium copper scrap within the domestic market beginning as early as 2027. Although proposals currently stop short of a full export ban, any retention mechanism would still materially reduce export availability for high-quality grades such as bare bright copper and No.1 copper scrap.

For China, tighter access to premium scrap has important implications beyond the secondary market. High-quality scrap directly competes with refined copper cathode because it offers high recovery rates with lower processing intensity than primary smelting. If imported scrap availability continues to tighten, Chinese refiners will likely need to increase refined copper purchases to maintain output levels.

This dynamic could become increasingly supportive for refined copper markets globally. The primary copper market is already facing structural constraints from weak mine supply growth, declining ore grades, permitting delays, and years of underinvestment in new projects. A simultaneous tightening in high-grade scrap availability would amplify pressure on refined copper balances precisely as demand linked to electrification continues to strengthen.

As a result, the market could see narrower scrap discounts relative to cathode, firmer copper premiums in Asia, and increased volatility across both COMEX and LME pricing. The secondary copper market is therefore becoming an increasingly important variable in the broader refined copper outlook.

Ultimately, the copper scrap market is no longer operating purely on economic arbitrage. Strategic resource security is becoming a defining driver of trade flows and policy decisions. The rapid growth in ASEAN intermediary trade, combined with collapsing direct Chinese scrap imports and growing US policy intervention, signals that the global copper supply chain is entering a new phase of fragmentation — one that is likely to tighten both scrap and refined copper markets into 2026 and beyond.

Author: Shairaz Ahmed, Principal Market Analyst

For more information or to discuss market dynamics, you can contact me on shairazahmed@smm.cn

![U.S.-Iran Strikes Spark Peace Talk Concerns, Intraday Copper Prices Decline [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/HaNSH20251217171714.jpeg)