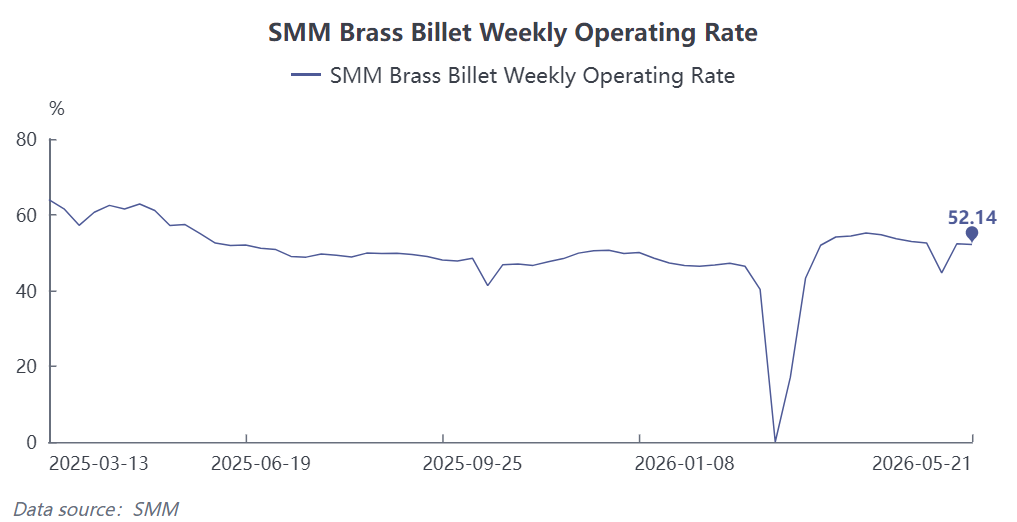

The brass billet industry continued to be in the doldrums under the triple pressures of the traditional off-season, high raw material costs, and weak demand. According to SMM data, the brass billet industry operating rate registered 52.14% this week (5.15-5.21), down 0.2 percentage points WoW, extending the low-level trend since late April. The "tight supply and high prices" pattern on the raw material side remained unbroken, the off-season effect on the demand side fully fermented, and the industry exhibited weak characteristics of constrained supply, soft demand, and slight inventory accumulation.

Supply side: Recycled raw materials remained tight and expensive, with production constraints intensifying

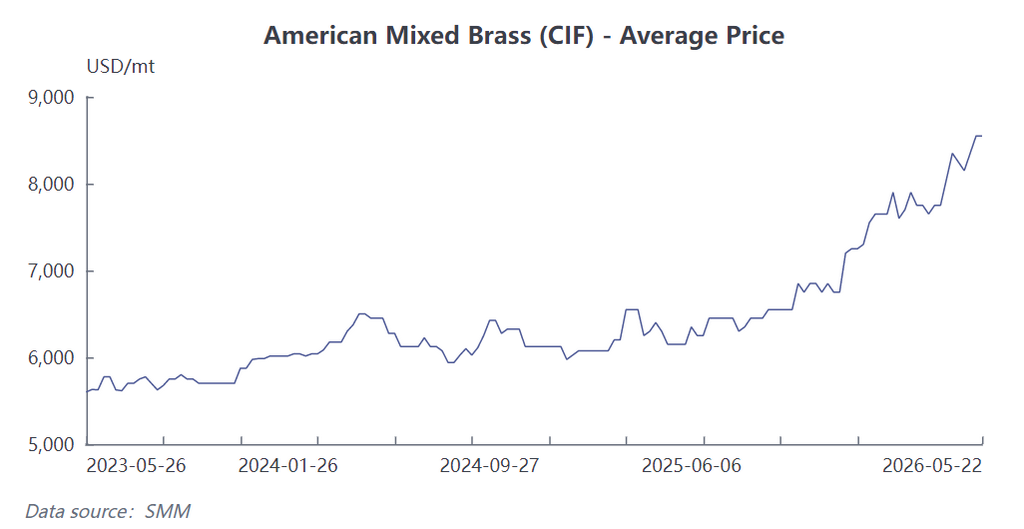

The recycled brass raw materials market continued in an imbalanced state of tight supply and high prices, imposing hard constraints on enterprise production. On one hand, the tight supply of imported secondary brass showed no signs of easing, compounded by limited domestic scrap brass recycling volume, market circulating resources remained tight, and raw material procurement difficulty increased. On the other hand, raw material prices stayed high, continuously squeezing enterprise profit margins. Most enterprises maintained low raw material inventory levels to control costs, while some small and medium-sized enterprises were forced to slow down their production pace due to raw material procurement difficulties, with production cuts becoming more common.

Demand side: Traditional off-season dragged down downstream orders across the board. The industry has entered the traditional consumption off-season, with weak end-use demand showing no improvement whatsoever, becoming the core factor dragging down industry operations. Orders from core downstream sectors such as home appliances, refrigeration, and bathroom hardware followed up weakly. End-users exhibited strong wait-and-see sentiment, with low purchase willingness, mostly making just-in-time procurement, and very few new orders.

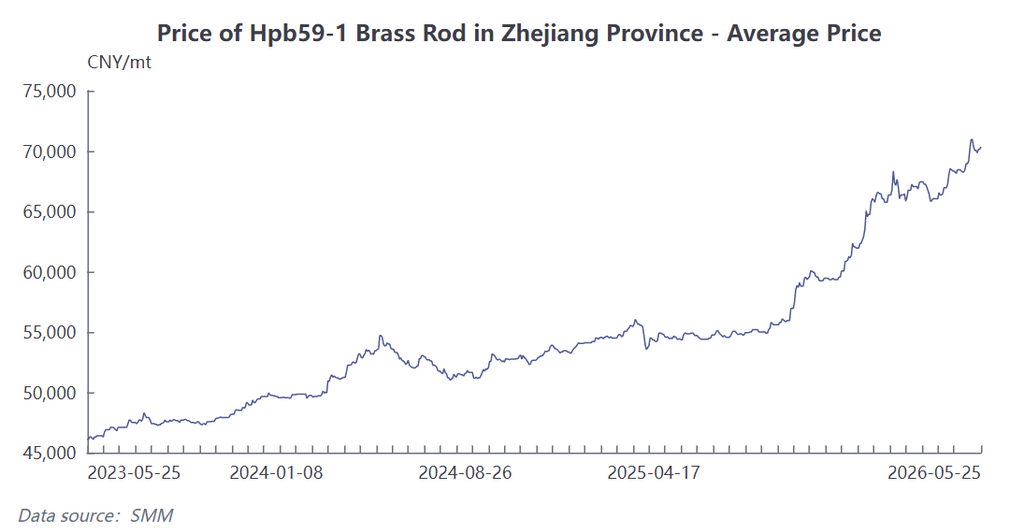

By sub-sector, demand in areas such as refrigeration valve components that previously supported industry production schedules also cooled as the off-season arrived. Orders in traditional hardware, plumbing, and other general sectors performed even weaker. After completing prior contracts, enterprises showed extremely low willingness to take orders, with a strong wait-and-see atmosphere in the market. Affected by this, the pace of brass billet enterprises taking orders slowed significantly. Meanwhile, copper billet prices remained high, downstream willingness to pick up goods was insufficient, and product shipments were sluggish, leading to continued accumulation of finished product inventories at relatively high levels, with increasing capital turnover pressure.

Looking ahead to this week (5.22-5.28), the traditional off-season nature of the brass billet industry is unlikely to reverse, and end-use demand is not expected to recover substantially in the short term. Meanwhile, copper prices are expected to continue fluctuating at highs, cost side disturbances will persist, the tight supply of recycled brass raw materials is unlikely to ease in the short term, and raw material constraints on production will continue to manifest. SMM forecasts that the brass billet industry operating rate will continue to run at low levels this week, edging down 0.06 percentage points WoW to 52.08%. Overall, the industry is expected to remain in the doldrums in the short term amid the interplay of high costs, weak demand, and high inventory, with little relief from enterprise operational pressure.