The Shanghai stainless steel futures contract (September 2026 contract, following a contract rollover) traded in a weak, range-bound pattern through the week ending May 22, 2026, caught between external macro headwinds and resilient spot-market fundamentals. The contract closed at approximately $2,176/mt (RMB 14,800/mt) as of May 22.

The week laid bare a sharp disconnect between paper and physical markets. Futures faced downward pressure from shifting expectations around overseas monetary policy, while the spot market proved remarkably resilient, buoyed by tight inventory levels and steady downstream demand. This divergence proved to be the defining tension of the week.

Macro sentiment stumbles; policy expectations recalibrate

The proximate driver of futures weakness was a notable shift in Fed communications. Published notes from the April monetary policy meeting showed less hawkish positioning on near-term rate cuts than markets had priced. This triggered a broad reassessment of the liquidity outlook, causing the US dollar index and Treasury yields to stabilize at elevated levels — a headwind for all commodities priced in dollars.

Domestically, however, a positive development partially offset external pressure. China and the US agreed in principle to discuss a parallel tariff reduction framework under their trade council structure, with both sides potentially cutting duties on goods worth $300 million or more. The signal offered by this bilateral détente helped absorb some of the bearish sentiment that might otherwise have weighed more heavily on local commodities.

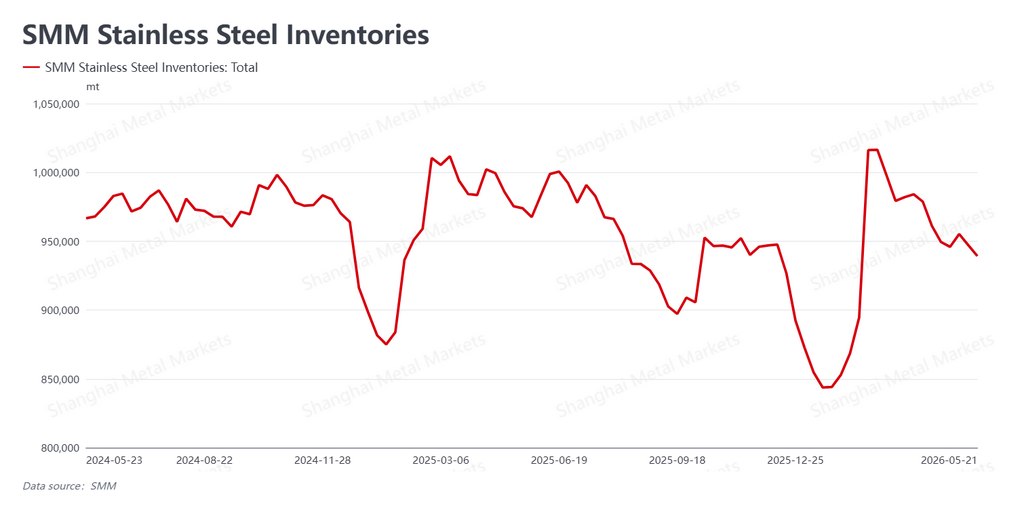

Inventory falls further; demand holds steady

The spot market's resilience rested on a pair of concrete fundamentals. SMM data showed social inventory fell further this week to 939,200 mt, down 7,900 mt week-over-week. At a time when the stainless steel sector is entering its traditional demand trough in late May, this counter-seasonal inventory compression provided the cash market with a structural bid.

Three factors explained the spot market's ability to resist the price declines seen on the futures board. First, mills have been parceling out supply more cautiously than usual, leaving traders with lower near-term delivery pressure. Second, trading houses are being measured about accumulating high-price inventory; their own stock positions remain tight, preventing the kind of panic liquidation that sometimes pressures physical prices. Third, and perhaps most important, end-use demand — while cautious — has not faltered. Downstream buyers continue to pull material at a steady pace despite a guarded outlook on longer-term prospects.

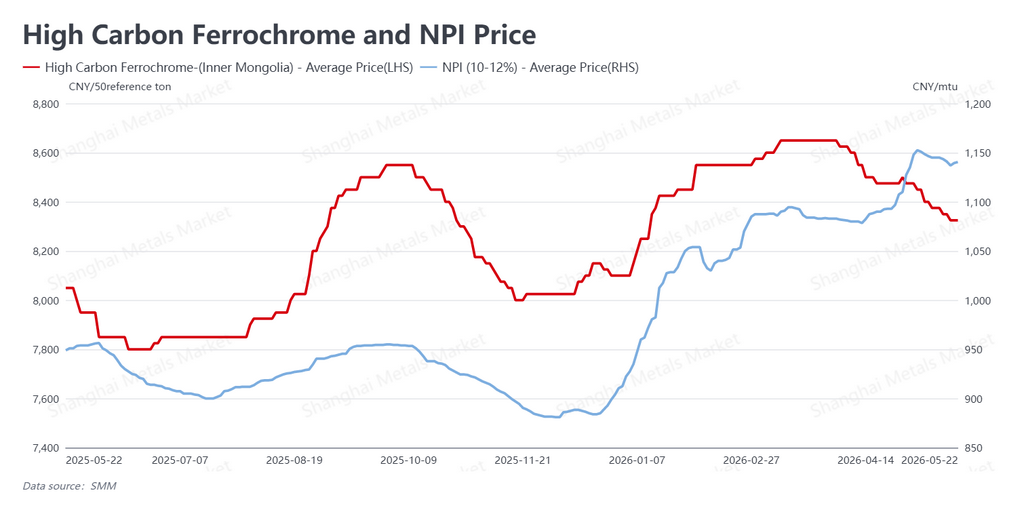

Raw materials ease; production remains brisk

Feedstock prices moved down modestly as a ripple effect from softer finished-steel prices and compressed mill margins. High-carbon ferrochrome fell to approximately $1,224/50-kg unit (RMB 8,325/50-kg unit), while Nickel Pig Iron (NPI) quotes eased to $168/nickel percentage point (RMB 1,140.5/nickel percentage point). Despite margin compression, stainless mills retain sufficient profitability to sustain high production rates, and run rates have remained elevated. This signals that the industry's longer-term supply surplus has not yet reversed course.

Looking ahead: weakness amid support

As late May gives way to June, stainless steel faces a seesaw dynamic: macro uncertainty continues to weigh on the futures contract, while tight inventory and resilient cash demand provide a floor beneath physical prices. The market's near-term character will likely hinge on whether downstream demand can sustain itself as the traditional summer lull approaches.

Near term, the main contract is expected to trade in a weak band with intermittent attempts to find bottom support. A sustained rally would require either a material pivot in Fed policy expectations or a significant deterioration in spot inventory — neither of which appears imminent. Traders should prepare for continued range-trading conditions, with spot-futures basis increasingly the focal point.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] Supply-Demand Price Spread Hard to Converge, Prices to Fluctuate in the Short Term](https://imgqn.smm.cn/usercenter/LNpBh20251217171732.jpeg)

![[SMM Analysis] Overseas Stainless Steel Weekly Review: Indonesia Export Control Policy Ignites Market Expectations](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)