Abstract: SMM data shows that during the week of May 18–22, 2026, overseas stainless steel markets recorded their first price correction following six consecutive months of gains. The pullback was short-lived, however, as the release of Indonesia's ferroalloy export control framework and news of NPI output cuts at the IWIP industrial park quickly refocused market attention on the supply side. Indonesia's leading stainless mills lowered FOB 304 cold-rolled export prices by USD 30/mt at the start of the week, bringing the run of uninterrupted increases stretching back to December 2025 to a close. LME nickel subsequently surged above USD 18,800/mt on the supply disruption narrative. The week's defining tension was the tug-of-war between a cost floor being repeatedly shored up by policy and a demand side that remains stubbornly resistant to high prices rather than any genuine improvement in underlying supply-demand fundamentals.

I. Macro & Policy: Export Control Framework Emerges, Mining Compliance Enforcement Escalates

The week's most consequential development came from Jakarta rather than from demand-side data. According to materials from a ministerial coordination meeting at Indonesia's Ministry of Trade, the government intends to bring ferroalloys, including ferronickel, under a strategic natural resource export governance framework. Under the proposed structure, a transition period runs from June 1 to December 31, 2026, during which exports must be routed through designated state-owned enterprise (SOE) channels and accompanied by a pre-shipment inspection report. From January 1, 2027, PT Danantara Sumberdaya Indonesia, the export vehicle under Indonesia's sovereign wealth fund Danantara, will become the sole authorised exporter of ferroalloys, completing a full nationalisation of export rights. Danantara's CEO confirmed that existing long-term supply contracts will be honoured, but warned that contracts involving under-invoicing or transfer pricing significantly below international benchmarks will be subject to rigorous retrospective review. If strictly enforced, this framework would fundamentally restructure the global ferroalloy trade: export pricing would shift from market-determined to state-controlled and fully transparent, displacing the current commercial pricing system.

Regulatory pressure from Indonesia's Ministry of Energy and Mineral Resources (ESDM) also intensified this week. According to SMM, more than 50 mining companies, which included 34 Nickel mining projects, that failed to submit their 2026 RKAB work plans on time have had their IUP mining licences suspended, with a 90-day remediation window before possible permanent revocation. Separately, production line rotational maintenance at the IWIP industrial park is expected to reduce high-grade NPI output by 10–15% over the coming months; SMM further understands that some lines have already been in a curtailed state since March–April due to ore shortages and elevated operating costs, with no clear near-term recovery. This constitutes the fourth consecutive tightening measure on Indonesia's strategic resource supply chain, following the reduced of the RKAB annual quota, and the revised HPM formula.

That said, a notable disconnect remains between cost-side support and actual price transmission downstream. Despite the cost floor being repeatedly reinforced by policy action, physical demand recovery has remained limited, and buyer resistance to elevated prices continues to suppress real transaction volumes.

II. Market Fundamentals: "Buy the Rally, Not the Dip" Keeps Volumes Depressed After Price Cut

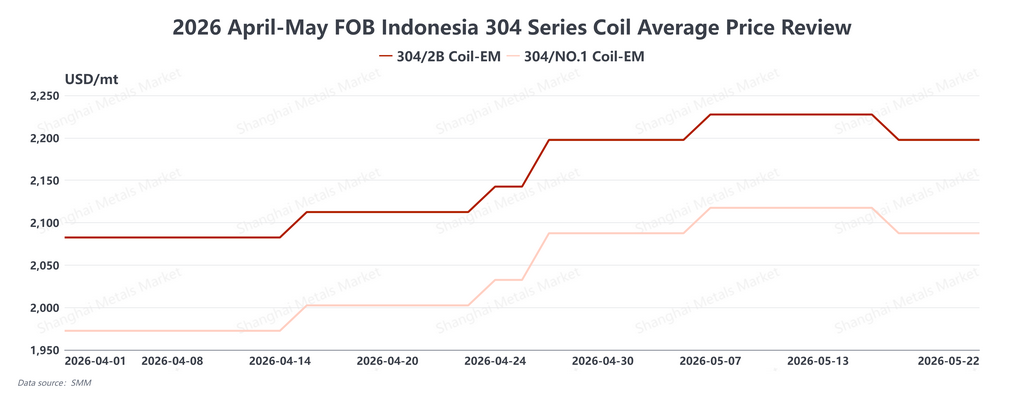

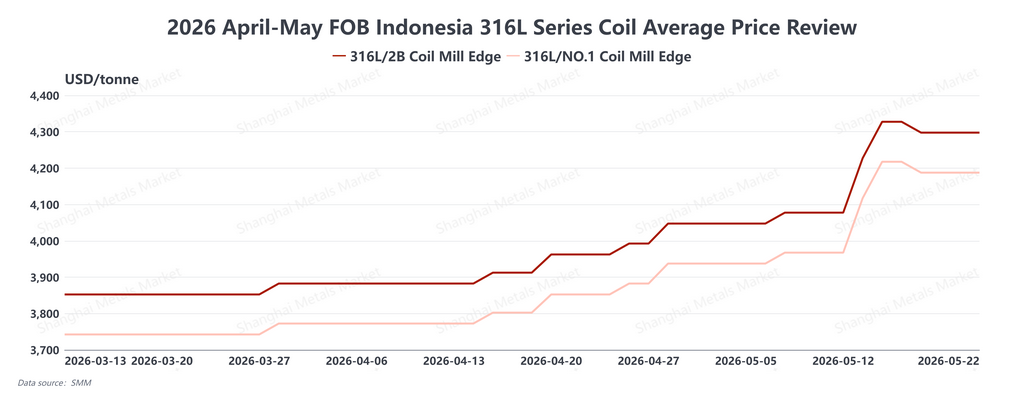

Overseas stainless steel spot markets generated no meaningful demand recovery signals this week, despite the price reduction. Indonesia's mainstream mills lowered FOB export quotes by USD 30/mt at the start of the week. The latest indicative prices are: Indonesia FOB 304 cold-rolled at USD2197.50/mt and hot-rolled at USD2087.50/mt; 316L cold-rolled at USD 4297.50/mt and hot-rolled at USD 4187.50/mt. Rather than stimulating restocking, however, the price cut reinforced a "buy the rally, not the dip" mentality among buyers, who interpreted the reduction as a signal to wait rather than to act. Transaction activity across Southeast Asia remained thin and the market settled into an uneasy holding pattern.

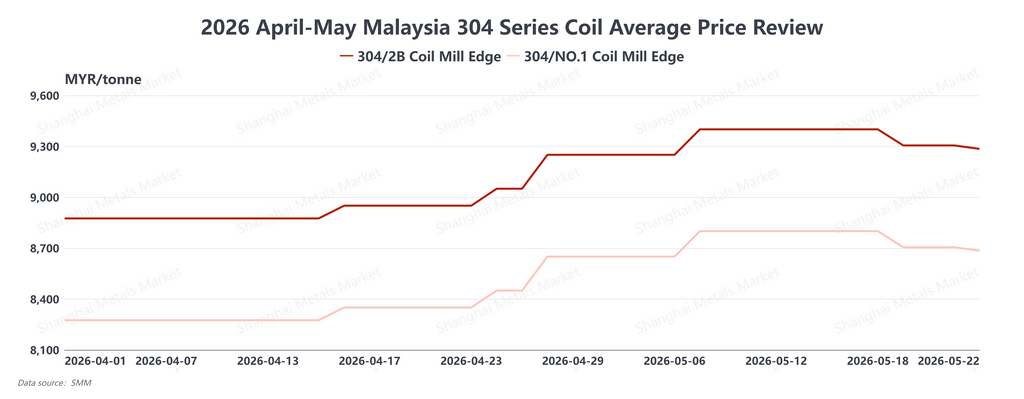

Malaysia's domestic 304 stainless prices reduced twice during the week for a combined reduction of MYR 115/mt, bringing the latest price to MYR9285/mt for 304 cold-rolled and MYR8685/mt for hot-rolled coil. The broader Southeast Asian market is effectively in a standoff, further complicated by Malaysia's unresolved anti-dumping review against Indonesian and Vietnamese stainless imports, a policy vacuum that leaves both upstream suppliers and downstream buyers reluctant to commit. Chinese Taiwan's stainless market faced additional headwinds: April export volumes fell 10.4% month-on-month while import volumes remained elevated at around 103,000mt with declining average import prices, squeezing local mills from both ends. India, by contrast, remained a positive outlier, local end-users have broadly accepted the increment in prices, and sectors such as automotive and process industries, where stainless represents a modest share of total input costs, continue to absorb increases; yet this pocket of demand strength is insufficient to offset the softness across Europe, Southeast Asia, and Taiwan, China. Across the overseas market as a whole, procurement remains driven by immediate operational needs rather than any proactive inventory build.

III. Summary and Outlook

This week's overseas stainless steel market was driven by policy expectations rather than any substantive improvement in supply-demand fundamentals. The price reduced at the start of the week was an reflection of demand-side resistance; the rapid re-emergence of bullish expectations that followed was a policy-driven re-anchoring of the cost floor.

Looking ahead to the next two weeks, the market is likely to enter an active policy-window negotiation phase. With Indonesia's ferroalloy export control transition period commencing on 1st of June, there is a meaningful probability of a pre-deadline export acceleration as mills and traders seek to complete shipments under the existing commercial framework. This could support another FOB 304 price increase of USD 30–60/mt. Simultaneously, buyers in India and other markets that rely heavily on Indonesian slab and NPI imports, including the huge amount of India's stainless slab import volumes, have begun assessing supply chain diversification options. The structural reconfiguration of the downstream supply chain is likely to become one of the defining themes for the overseas stainless market through Q2 2026.

To conclude, the majority of Indonesia's policy boots have now landed, RKAB quotas reduced, HPM revision, and the export control framework still transitioning. Until the final framework is fully operational, the overseas stainless market's pricing equilibrium will continue to oscillate between cost-side support and demand-side ceiling, with June set to be the most critical testing ground.

![[SMM Analysis] Philippine Inventory Continues to Accumulate, Indonesia Premium Narrows, and RKAB Flexible Policy Opens a New Stage](https://imgqn.smm.cn/usercenter/VstiG20251217171732.jpeg)

![[SMM Conference] ICM 2026: Global Ni & Co Outlook: Mine Opportunities & Challenges, Investment in Indonesia](https://imgqn.smm.cn/production/admin/votes/imagesozMBI20260610115722.jpeg)