[SMM Global Steel Enterprise Special Report] A Detailed Analysis of US "Steel King" Nucor: 100% Electric Arc Furnace Forging High Profits, Vertical Integration Mitigating Cost Fluctuations

Nucor Corporation is a company incorporated in Delaware in 1958. The company and its subsidiaries are engaged in the manufacture of steel and steel products. It also produces and procures ferrous and non-ferrous metal materials, primarily for use in its steelmaking operations. Most of its operating facilities and clients are located in North America. Its operations include international trading and sales companies responsible for buying and selling steel and steel products manufactured by the company and others. Nucor is also the largest recycler in North America, using steel scrap as the primary raw material for producing steel and steel products. In 2025, it recycled approximately 20 million gross tons of steel scrap.

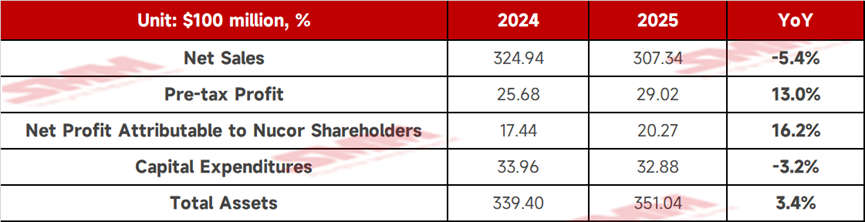

- Operating Performance

Data source: Nucor Corporation Annual Report、SMM

Reasons behind the performance changes:

① Decline in gross profit: The primary reason for the decline in gross profit in 2025 was the compression of profit margins in the steel products segment. Due to lower average selling prices, gross profits from the grating and decking, building systems, and rebar fabrication businesses under this segment all experienced significant declines.

② Steel mill segment growth: In contrast, gross profit in the steel mill segment increased, primarily driven by higher sales and improved steel industry spreads.

③ Investment expenditures: Over the past three years, Nucor invested approximately $9.73 billion in capital expenditures and acquisitions, aiming to expand its product portfolio and enhance operational flexibility.

- Segments, Major Products, and Marketing

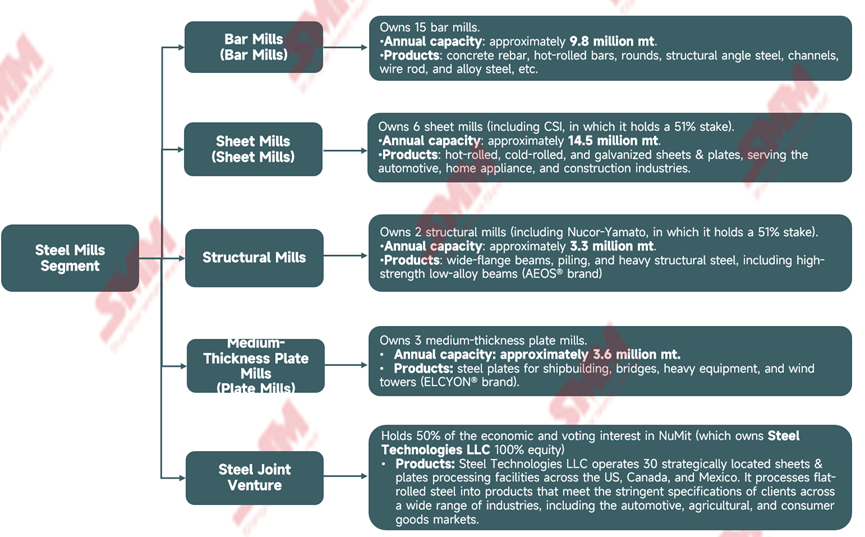

Nucor reports its results in three segments: the steel mills segment, the steel products segment, and the raw materials segment. The steel mills segment is Nucor's largest segment, accounting for 62% of the company's sales to external clients for the fiscal year ended 2025. It primarily sells its products to steel service centers, manufacturers, and fabricating enterprises located in the US, Canada, and Mexico. In 2025, the steel mills segment sold approximately 19,848 kt of products to external clients.

Data source: Nucor Corporation Annual Report、SMM

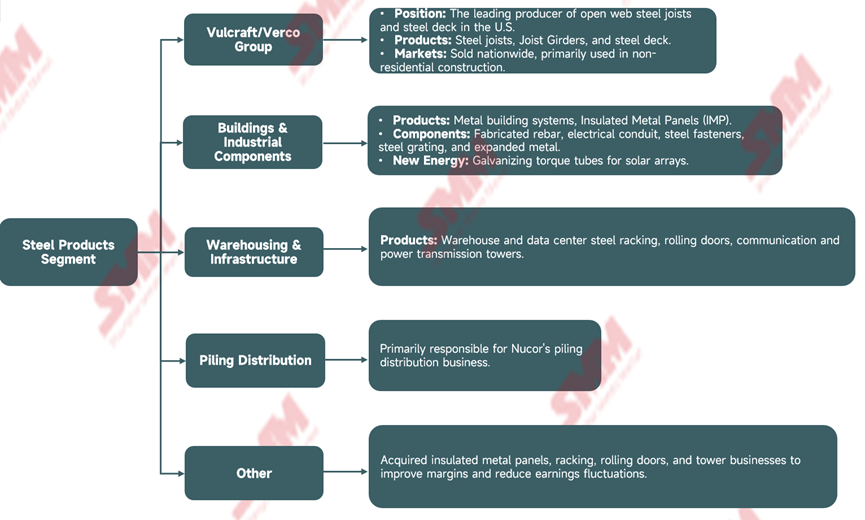

The Steel Products segment primarily produces high-value-added downstream construction and industrial components, holding leading positions across the U.S. in multiple sub-segments including steel joists, prefabricated metal buildings, and insulated metal panels. It accounted for 29% of the Company's net sales to external clients for the year ended 2025. In 2025, total sales of major products in the Steel Products segment were approximately 1.478 million mt, including approximately 658,000 mt of steel joists and joist girders, approximately 436,000 mt of steel deck, and approximately 384,000 mt of metal building systems. Although physical sales volume (tonnage) was far below that of the Steel Mills segment, the per-mt selling price and profit margin were much higher than those of basic steel, and the segment also ranked first in market share across the U.S. in multiple areas.

Data source: Nucor Corporation Annual Report、SMM

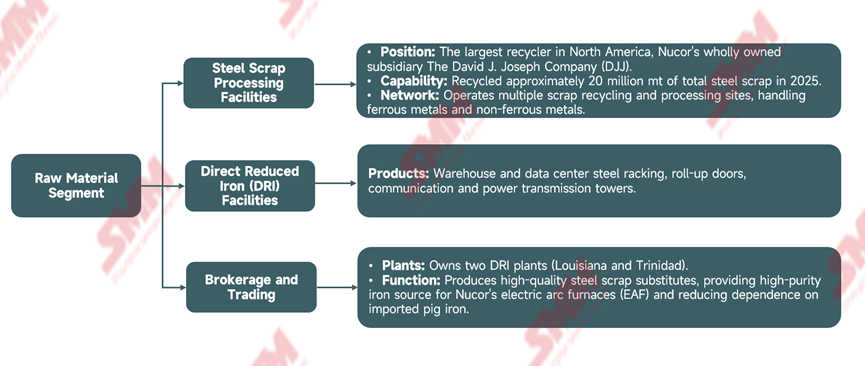

The Raw Materials segment is the cornerstone of Nucor's vertical integration strategy, primarily operated through its wholly-owned subsidiary The David J. Joseph Company (DJJ), and manages DRI production facilities in Louisiana and Trinidad. By blending DRI with steel scrap, it supports electric arc furnace (EAF) production of higher-grade sheets & plates while ensuring cost advantages and supply security of raw materials. It accounted for 9% of the Company's net sales to external clients for the year ended 2025. In 2025, approximately 20 million gross tons of steel scrap were recycled and processed.

Data source: Nucor Corporation Annual Report、SMM

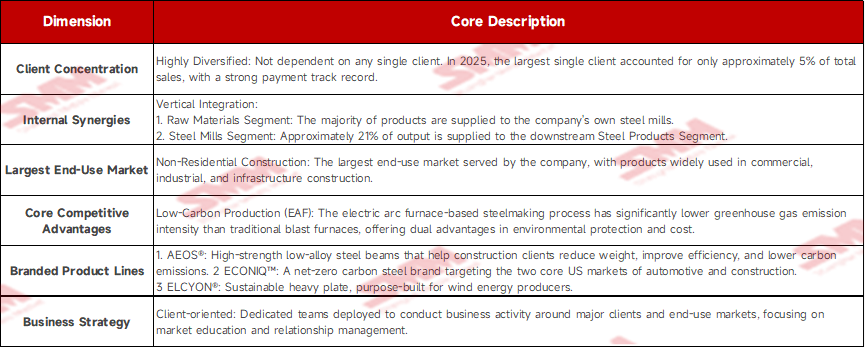

- Clients and Markets

Data source: Nucor Corporation Annual Report、SMM

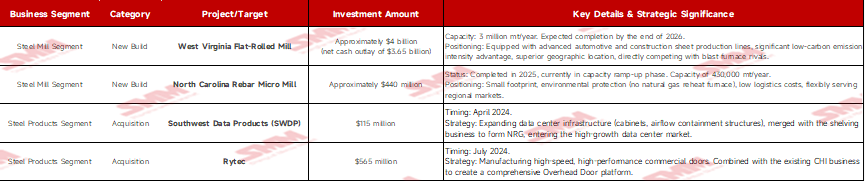

- Major Development Projects in Recent Years

The vast majority (91%) of Nucor's capital was allocated to internal construction (CapEx), strengthening core competitiveness through technology upgrades (such as electric arc furnaces and micro mills); a small portion was used for strategic acquisitions to achieve "outward expansion" into high-margin downstream areas. Through acquisitions such as SWDP, the company quickly entered high-barrier, high-growth sub-segments including data centers and green energy, making its business structure more resilient to cyclical downturns.

Data source: Nucor Corporation Annual Report、SMM

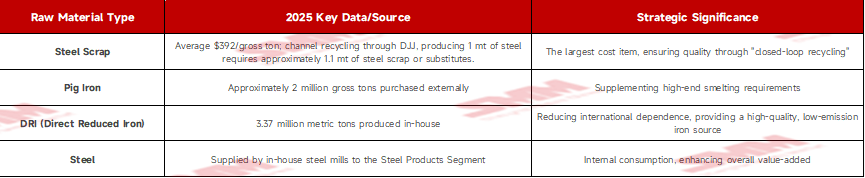

- Core Logic of Vertical Integration for Cost Reduction: Raw Material Supply Structure

Data source: Nucor Corporation Annual Report、SMM

- Core Risk Factors

The greatest risk facing Nucor is a combination of internal and external challenges — internally, cost fluctuations in steel scrap and energy; externally, the impact of low-priced imported steel resulting from global (especially China's) overcapacity. Specifically:

1. Core Industry Risks

① Severe global supply-demand imbalance: Global steel surplus capacity reached 704 million net mt in 2025 (8 times US annual production). It is expected to further increase to 795 million mt by 2027.

② Regional impact: China's annual production has exceeded 1 billion mt in each of the past 8 years, and Chinese steelmakers continue to invest in new capacity in Southeast Asia and Africa.

② Import shock: This surplus leads to a flood of low-priced steel into the US market, creating significant downward pressure on Nucor's product prices, sales, and profit margins.

2. Production Cost Risks

① Steel scrap price sensitivity: Nucor uses 100% electric arc furnaces (EAF), with steel scrap being the largest cost item. Steel scrap prices fluctuate significantly and are beyond Nucor's control.

② Supply chain uncertainty: Although Nucor has achieved a degree of self-sufficiency through its DRI plants and DJJ recycling system, pig iron and iron ore pellets still rely on international procurement, facing geopolitical risks (e.g., Ukraine, Russia, Brazil).

3. Operational Challenges

① Energy-intensive nature: Steelmaking relies on large amounts of electricity (for melting) and natural gas (for heating and DRI production).

② Cost pass-through: Energy prices are affected by demand, the regulatory environment, and transmission infrastructure (pipelines/power grid), and cost surges may erode profits.

4. Compliance and ESG Risks

① Emission reduction pressure: The steel industry faces intense scrutiny due to greenhouse gas (GHG) emissions.

② Policy risk: Although Nucor's emission intensity is far lower than its blast furnace peers, increasingly stringent environmental protection laws and regulations may increase capital expenditures or restrict operations at existing facilities.

5. End-Use Market Risks

① Industry cyclicality: The steel industry is highly correlated with the macro economy.

② End-use market fluctuations: Nucor's largest market is non-residential construction. If this sector (e.g., commercial offices, industrial facilities) contracts due to high interest rates or economic recession, it will directly impact Nucor's performance severely.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Iron & Steel] US Iron & Steel Scrap Exports Fall 27.1% MoM in April 2026](https://imgqn.smm.cn/usercenter/Zznfn20251217171716.jpg)