From May 13 to 15, 2026, former US President and re-elected Republican leader Donald Trump paid a highly anticipated state visit to China. The scene was strikingly familiar, yet the world had changed dramatically. In November 2017, Trump embarked on his first state visit to China, during which the two sides signed commercial contracts totaling a staggering $250 billion—a figure that epitomized the "you in me, me in you" prosperity of globalization. However, less than six months after that 2017 visit, in March 2018, the China-US trade war officially erupted.

Amidst the turbulence of these nine years, one strategic variable—buried deep underground but capable of choking modern industry and national defense—is rare earth. In particular, "Terbium Oxide" (氧化铽), a representative element of heavy rare earths, has acted as an invisible red line connecting the entirety of the China-US trade war from 2017 to 2025.

If we wind the clock back to 2017, China-US economic and trade relations were in the twilight of a "honeymoon period." Back then, rare earth permanent magnet trade faced occasional friction but operated smoothly under the drive of commercial interests. However, with the full outbreak of the China-US trade conflict in 2018, rare earths gradually became a focal point of contention.

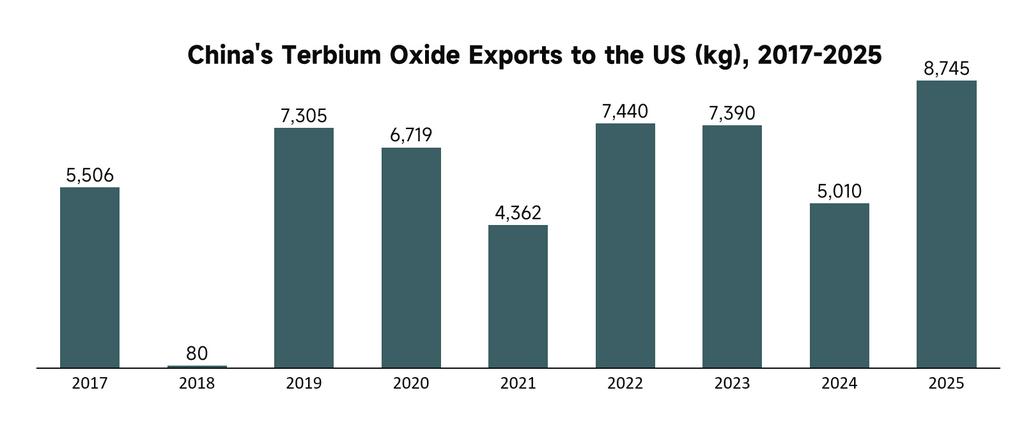

In 2018, China's direct exports of Terbium Metal to the US plummeted to zero, dropping instantly from 160 kg in 2017 to 0 kg. In the face of harsh tariffs, businesses vote with their feet. Confronted with the aggressive tariff hikes imposed by the US on Chinese goods, Chinese rare earth enterprises displayed acute sensitivity. Amidst soaring policy uncertainties, the proactive suspension of high-purity strategic metal exports was both a reluctant measure to avoid tariffs and a silent form of strategic deterrence. Enterprises began converting Terbium Metal into downstream magnetic materials or hoarding Terbium Oxide inventories to weather the crisis indirectly.

Simultaneously, US imports of Chinese Terbium Oxide collapsed to a mere 80 kg in 2018—less than one-tenth of normal export volumes. For the first time, rare earths essentially served as a substantive check on US industrial capabilities.

Time advanced to 2019, and the trade war rapidly escalated into a technological conflict. The Huawei incident brought bilateral contradictions in high-end manufacturing into the open. During this period, China's perception of its rare earth supply chain shifted fundamentally from "commercial monetization" to "strategic defense."

From 2019 to 2022, China's exports of Terbium Metal to the US remained at a steadfast zero. This four-year "supply cutoff" was not due to a lack of production capacity, but rather a proactive national security measure. It must be clearly understood that Terbium-based metals are indispensable core coatings and alloy materials for high-end military equipment (such as F-35 fighter jet radar systems and precision missile guidance systems). China has a responsibility to ensure such materials are used in ways that benefit human development, rather than fueling hegemony. Allowing the export of such strategic resources while the US arbitrarily suppressed Chinese tech firms and cut off chip supplies would have been tantamount to abetting the wrongdoer.

Simultaneously, China's domestic rare earth industry underwent a painful but necessary restructuring. The outdated model of selling primary mineral products for foreign exchange was abandoned, replaced by industrial policies encouraging innovation and extending the value chain downstream into high-value-added permanent magnetic materials. The confidence for this industrial upgrade lay in the reality that, despite subsequent US attempts to decouple, American industry remained fundamentally reliant on Chinese supply chains.

Against this macro backdrop, the 2021 Terbium Oxide export data revealed a profound shift: exports to the US plummeted to only 4,362 kg, far below normal levels for surrounding years.

This sharp decline was essentially an early manifestation of the US "small yard, high fence" strategy backfiring. In 2021, driven by political motives, the US aggressively pushed for the "localization" of its rare earth supply chain, attempting to rebuild capacity with allies. However, this politically driven, non-market procurement failed to meet domestic demand and instead massively increased compliance and trial-and-error costs due to an immature supply chain. In this distorted trade environment, China's direct exports of Terbium Oxide to the US were forced down to 4,362 kg. This was by no means an indication that China needed the US market; rather, it proved that the high walls the US built in the tech sector ultimately ended up blocking its own path.

As the timeline moved into 2023 and 2025, the China-US rivalry entered even more treacherous waters. The US imposed extreme sanctions on China in semiconductors and new energy vehicles, attempting to stifle China's high-tech development. In response, China's counter-strategies became increasingly precise and forceful.

If the zero exports of 2018 were a corporate stress reaction, and the 2019-2022 cutoff was industrial strategic defense, then the 2025 export controls on heavy rare earths represented a perfected, legally grounded system of precise control.

In April 2025, China's Ministry of Commerce and the General Administration of Customs announced strict export controls on seven categories of heavy rare earth items—including Samarium, Gadolinium, and Terbium—mandating that all exports require a special state-issued license. As strategic metals indispensable to industry, it is necessary to ensure they are applied in fields that promote human development and well-being, rather than supporting the滋生 (breeding) of hegemony.

Consequently, in 2025, US imports of Chinese Terbium Metal were once again unsurprisingly zero. Unlike in 2018, this zero was not passive risk avoidance, but a highly institutionalized, normalized control. Any attempt to funnel Terbium Metal into the US military-industrial complex would face severe legal penalties.

On the oxide front, the 2025 policy shift fundamentally altered the previous trade balance. China's export controls were not a blanket embargo, but rather a precise exercise in "extraterritorial jurisdiction" (long-arm jurisdiction). For high-performance magnetic materials and key raw materials (like Terbium Oxide) with dual-use potential, drastically lengthened approval processes led to a cliff-edge drop in trade volumes.

The data shows that the sharp decline in US imports of Terbium Oxide in 2025 was not due to a disappearance of demand from US high-tech and military sectors, but rather a severe supply-demand mismatch caused by rising trade barriers and compliance costs. In the past, US companies could procure freely based on market demand; today, every transaction involving controlled items must undergo rigorous end-user verification and usage commitments. This "passive reduction caused by rising compliance costs" has become the new normal in China-US rare earth trade. Through the licensing system, China has effectively installed a "remote switch" over critical US supply chains, forcing the US to think twice before imposing any new technological blockades against China.

Finally, let us return to the present: May 13-15, 2026, and Trump's return to China.

When Air Force One landed again at Beijing Capital International Airport, it resonated strongly with that November day nine years prior. However, the chessboard has fundamentally changed. After nine years of fierce博弈 (fierce competition), both China and the US clearly realize that a simple "decoupling and severing of supply chains" regarding rare earths—a resource vital to national fortunes—will only lead to mutual defeat.

During the behind-the-scenes negotiations of this 2026 visit, rare earths are undoubtedly one of the core agenda items. The US will inevitably present a long "procurement exemption list" for restricted rare earth elements, specifically pleading for the resumption of normal supplies of heavy rare earths like Terbium Oxide to sustain its defense industrial base. In turn, China will naturally use this leverage to demand substantial concessions from the US regarding high-tech export restrictions and tariff barriers.

Of course, as a third-party observer of the rare earth market, SMM does not presume to judge the absolute rights or wrongs of national strategies. We sincerely hope for world peace and smooth trade, and we look forward to a future filled with more opportunities and mutual expectations.