SMM May 13 News:

Metals market:

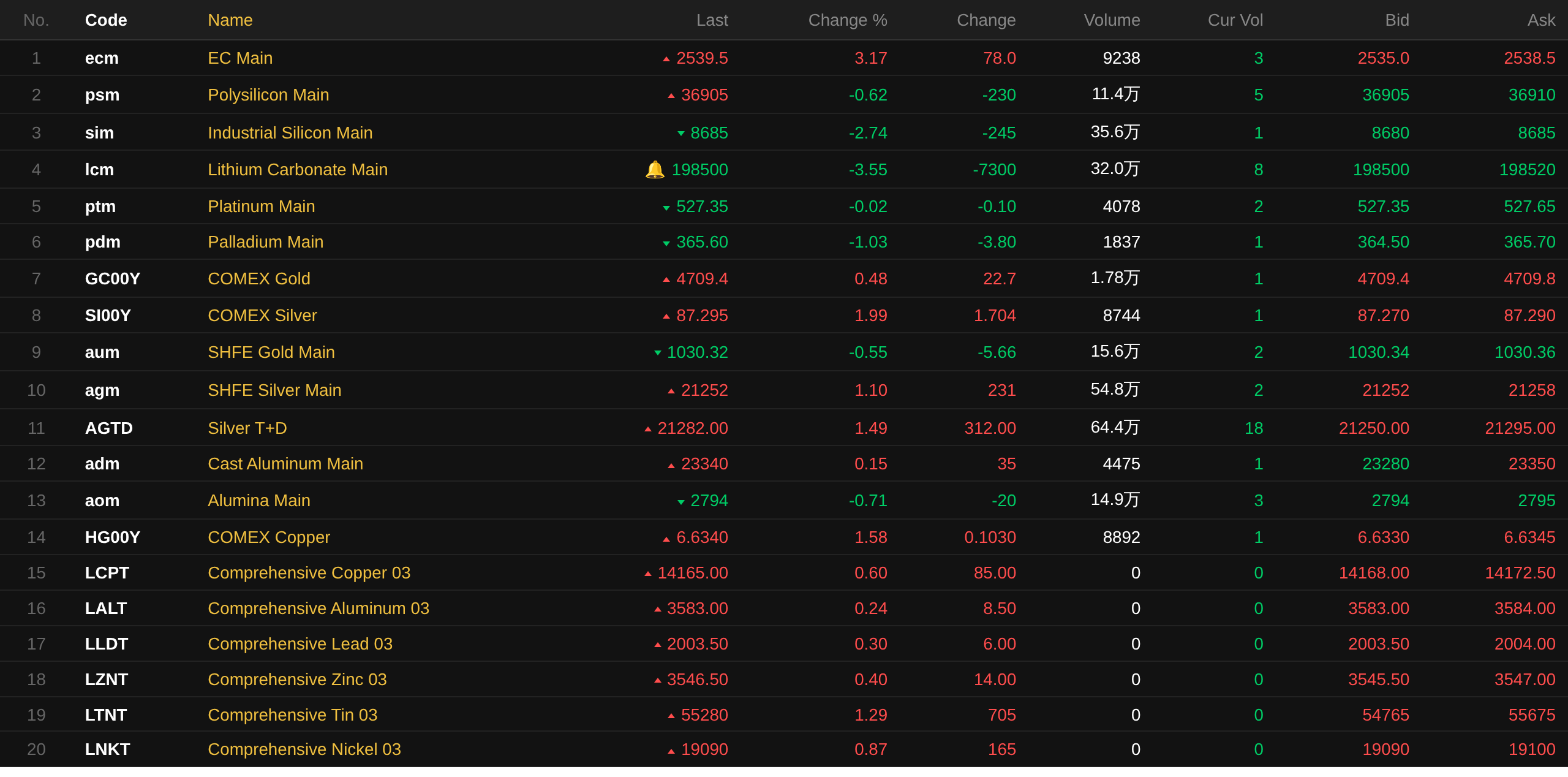

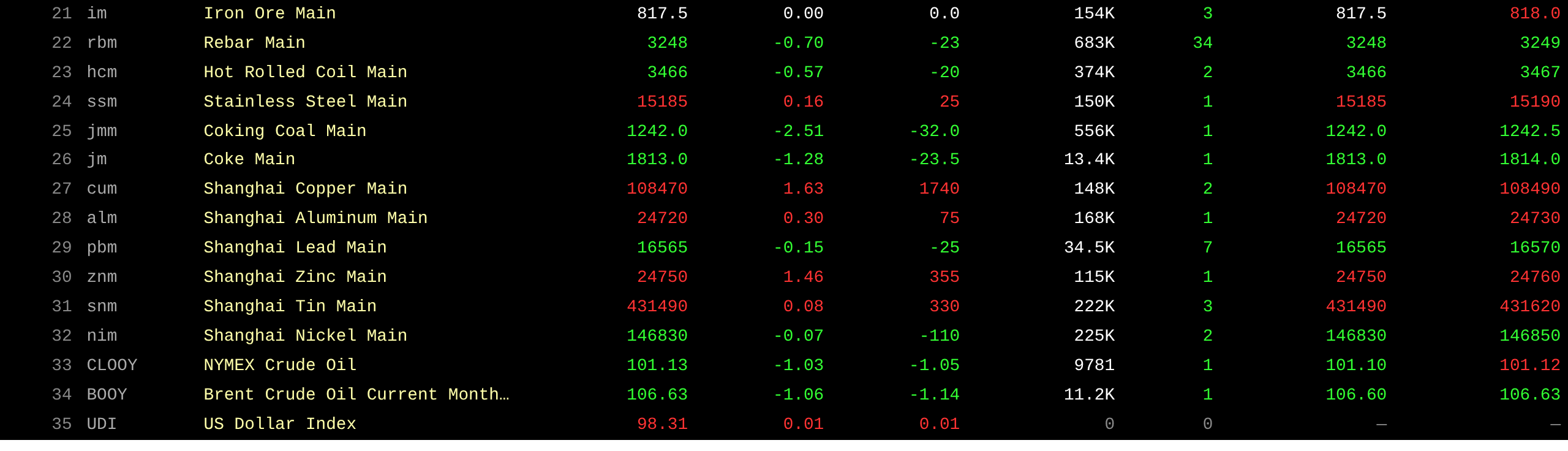

As of the midday close, base metals in the domestic market generally rose. SHFE copper gained 1.63%. SHFE aluminum rose 0.3%. SHFE lead fell 0.15%. SHFE zinc gained 1.46%. SHFE tin rose 0.08%. SHFE nickel edged down.

In addition, the most-traded casting aluminum futures rose 0.15%, the most-traded alumina futures fell 0.71%. The most-traded lithium carbonate futures fell 3.55%. The most-traded silicon metal futures fell 2.74%. The most-traded polysilicon futures fell 0.62%.

Ferrous metals mostly fell. Iron ore was flat at 817.5 yuan/mt. Rebar fell 0.7%. Hot-rolled coil fell 0.57%. Stainless steel rose 0.16%. Coking coal and coke: the most-traded coking coal contract fell 2.51%, and the most-traded coke contract fell 1.28%.

Overseas base metals, as of 11:41, LME metals rose across the board. LME copper gained 0.6%. LME aluminum rose 0.24%. LME zinc gained 0.4%. LME lead rose 0.3%. LME tin gained 1.29%. LME nickel rose 0.87%.

Precious metals, as of 11:41, COMEX gold rose 0.48%, and COMEX silver gained 1.99%. Domestic precious metals: the most-traded SHFE gold contract fell 0.55%, and the most-traded SHFE silver contract rose 1.1%.

In addition, as of the midday close, the most-traded platinum futures edged down, and the most-traded palladium futures fell 1.03%.

As of the midday close, the most-traded Europe containerized freight index contract rose 3.17%, closing at 2,539.5 points.

As of 11:41 on May 13, midday futures quotes for selected contracts:

Spot and Fundamentals

Copper:Looking ahead to tomorrow, copper prices continue to fluctuate at highs, downstream purchasing sentiment remains subdued, intraday buying and selling sentiment both pulled back, and spot discounts continued to widen. According to SMM, downstream orders continued to decline from the previous day...

Macro Front

[China-US Economic and Trade Consultations Begin in South Korea]At noon local time on May 13, the economic and trade teams of China and the US began China-US economic and trade consultations at Incheon International Airport in Seoul, South Korea. (Xinhua)

Domestic:

[PBOC Reverse Repo Operations Achieved Net Withdrawal of 25.5 Billion Yuan on the Day]The PBOC conducted 500 million yuan of 7-day reverse repo operations today. As 26 billion yuan of 7-day reverse repos matured today, a net withdrawal of 25.5 billion yuan was achieved on the day.

US dollar:

As of 11:41, the US dollar index rose 0.01%, at 98.31. The US CPI rose faster than expected in April, further intensifying concerns about the impact of inflation on the US economy. The Bureau of Labor Statistics reported on Tuesday that, after seasonal adjustment, the overall CPI rose 0.6% MoM and 3.8% YoY. The monthly increase was in line with expectations, but the YoY increase was 0.1 percentage point higher than market expectations. Core CPI, excluding food and energy, rose 0.4% and 2.8% respectively, indicating that although inflation remained well above the US Fed's 2% target, pressure mainly came from non-core areas, especially energy. Energy prices rose 3.8%, once again becoming one of the main drivers of rising inflation; food prices also rose 0.5%. For the full year, energy prices rose 17.9% and food prices rose 3.2%. Gasoline price index was up 28.4% YoY. Although energy, especially gasoline, was the main news focus, inflationary pressures also came from multiple other areas. Housing costs rose 0.6%, tariff-sensitive apparel prices rose 0.6%, airfares rose 2.8% with a YoY increase of 20.7%. Tariffs also appeared to have affected other areas, with household furnishings and related expenditures rising 0.7%. (Jin10 Data)

According to the CME "Fed Watch": the probability of the US Fed maintaining rates unchanged through June was 97.1%, with a 2.9% probability of a cumulative 25 basis point interest rate cut. The probability of the US Fed maintaining rates unchanged through July was 96%, with a 3.9% probability of a cumulative 25 basis point interest rate cut. (Jin10 Data)

A CITIC Securities research report stated that US April inflation continued to run hot, the spillover effects of the Middle East conflict persisted, and compensatory increases in rent inflation pushed up core readings. High inflation continued to erode the real purchasing power of US households, with low-income households facing stronger cost shocks, and real hourly wages YoY turned negative for the first time in three years. We believe the risk of a second wave of US inflation is relatively small, but high oil prices will constrain the room for inflation to pull back within the year. Under the base case scenario, the US Fed is still expected to cut interest rate by 25bps within the year. US Treasuries are currently more suited for trading opportunities. After the strong earnings season nears its conclusion, US equities should be watched for short-term risks of profit-taking. The US dollar index may remain in the doldrums below 100 rather than on a sustained downtrend.

Other currencies:

According to a latest estimate by the OECD, the Bank of Japan's benchmark interest rate is expected to reach 2% by the end of 2027. The report noted that, assuming inflation remains around 2%, the current interest rate is still close to the lower bound of the neutral rate range for the economy. The report also recommended that the Bank of Japan should continue to gradually raise interest rates to prevent the economy from overheating. The Bank of Japan previously estimated that Japan's nominal neutral interest rate was between 1.1% and 2.5%, but noted that there was significant uncertainty regarding the specific level. (Jin10 Data)

On the macro front:

Data to be released today include France's Q1 ILO unemployment rate, France's April CPI MoM final reading, eurozone Q1 GDP YoY revised reading, eurozone Q1 seasonally adjusted employment QoQ final reading, eurozone March industrial output MoM, US April PPI YoY, and US April PPI MoM.

In addition, attention should be paid to: Chicago Fed President Goolsbee participating in a Q&A session hosted by a local chamber of commerce; 2028 FOMC voter and Boston Fed President Collins delivering a speech at the Boston Economic Club; Vice Premier He Lifeng leading a delegation to South Korea from May 12–13 for trade consultations with the US side; and US President Trump's state visit to China.

Crude oil:

As of 11:41, oil prices in both markets fell, with WTI down 1.03% and Brent down 1.06%. Iran presented its "entry ticket" for nuclear talks with the US, including unfreezing assets and recognizing sovereignty over the Strait of Hormuz. Trump stated: "When negotiating with Iran, I don't consider the financial situation of the American people. I don't consider anyone." Meanwhile, the US Secretary of Defense said the Iran ceasefire agreement remained in effect. (Jin10 Data)

American Petroleum Institute (API) data showed that US crude oil inventory fell for the fourth consecutive week last week, while gasoline inventory increased. US API crude oil inventory for the week ending May 8 was -2.188 million barrels, versus expectations of -1.654 million barrels and a prior reading of -8.141 million barrels. US API gasoline inventory for the week ending May 8 was 502,000 barrels, versus expectations of -2.549 million barrels and a prior reading of -6.107 million barrels.

The EIA Short-Term Energy Outlook report indicated that if the Strait of Hormuz were closed through the end of June, crude oil prices would be $20/barrel higher than the current forecast, which assumes reopening by the end of May. (Jin10 Data)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

![US Dollar Weakens on Weekly Chart, Metals Broadly Rise, LME Tin Up Nearly 5%, LME Zinc and COMEX Silver Up Over 2%, Gold, Silver End Week Higher [Overnight Market]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)

![In the short term, ferrous metals are consolidating at lows, and close attention should be paid to steel mill maintenance situations [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/nDTpN20251217171748.jpg)

![[SMM Analysis]Aluminum Billet Inventory Falls to 130,000 mt, Warehouse Withdrawals Rebound, Processing Fees Soften](https://imgqn.smm.cn/usercenter/DRlGu20251217171652.jpg)