In Q1 2026, China's hydrogen energy industry officially moved beyond the concept verification phase and fully entered a new stage of large-scale development. Two landmark events—the commissioning of Xinjiang Sunion Energy’s coke oven gas hydrogen production project and the cumulative hydrogen refueling volume exceeding 10,000 kilograms at the Batuta heavy-haul railway hydrogen refueling station in Inner Mongolia—have validated the core industry trend of cost reduction, scenario expansion and regional agglomeration from the two dimensions of low-cost hydrogen supply and diversified application scenarios respectively.

I. Market Status: Accelerated Large-scale Development, Dual Breakthroughs in Supply and Application

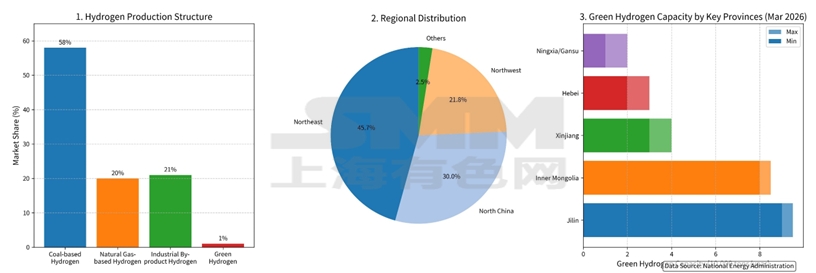

Hydrogen production capacity has achieved leapfrog growth, with Northwest and North China emerging as core agglomeration hubs. Driven by the dual-carbon strategy, China’s hydrogen production capacity has seen explosive growth. As of the end of March 2026, the completed and under-construction renewable energy hydrogen production capacity across China has surpassed 1 million tons per annum, among which the operational capacity exceeds 250,000 tons per annum, more than doubling compared with the end of 2024. The industrial layout shows a high geographical concentration; Northwest and North China have become core clusters by virtue of resource endowments.Jilin (over 90,000 tons per annum) and Inner Mongolia (over 80,000 tons per annum) have registered rapid development. The operational hydrogen production capacity in Northeast China accounts for 45.7% of the national total, shaping the initial industrial pattern of hydrogen supply from west to east and hydrogen transmission from north to south.

The supply structure continues to optimize, and industrial by-product hydrogen production has become the mainstay of low-cost hydrogen supply. Currently, profound adjustments are taking place in China’s hydrogen supply structure. Boasting low cost and waste-to-energy advantages, industrial by-product hydrogen production has become the most economical pathway at this stage. Purifying hydrogen from coal chemical by-product coke oven gas features nearly zero raw material cost, perfectly matching cost-sensitive industrial scenarios. Meanwhile, driven by technological iteration, the cost of green hydrogen in multiple regions of Northwest China has dropped to 12–15 RMB per kilogram, gradually approaching the cost of gray hydrogen and laying a foundation for long-term low-carbon hydrogen supply.

Application scenarios have evolved from demonstration to diversification, with industry and transportation acting as core growth engines. The year 2026 is regarded as the inaugural year for large-scale industrial application of hydrogen energy, with scenarios expanding rapidly into in-depth application fields. In the transportation sector, the commercial operation of hydrogen heavy-duty trucks has matured, with a thousand-unit scale put into operation in Lvliang, Shanxi. The launch of hydrogen refueling stations for heavy-haul railways fills the gap in carbon emission reduction for rail transit. In the industrial sector, a closed-loop model of on-site hydrogen production and consumption via by-product purification has taken shape among chemical enterprises. Industrial decarbonization has replaced transportation as the core driving force for industry growth.

II. Recent Project Highlights: Two Benchmark Projects Accurately Align with Market Trends

Xinjiang Sunion Energy’s coke oven gas hydrogen production project sets a model for industrial by-product hydrogen production. Recently, Xinjiang Sunion Energy’s 5,000 Nm³/h green hydrogen production project using coke oven gas was fully put into operation. The project converts waste industrial coke oven gas into high-purity clean hydrogen, realizing waste recycling and effectively solving exhaust emission problems, while supplying low-cost hydrogen to methanol plants. Furthermore, it provides a replicable development model for coal chemical agglomeration areas in Northwest China and boosts regional hydrogen supply capacity.

The Batuta Hydrogen Refueling Station in Inner Mongolia marks a milestone in hydrogen energy application for heavy-haul railways. As of April 16, 2026, China’s first hydrogen refueling station for heavy-haul railways—the Batuta Station—has recorded a cumulative hydrogen refueling volume of over 10,000 kilograms. Equipped with a 45 MPa skid-mounted compressor and a maximum hydrogen refueling flow rate of 7.2 kg/min, the station is specially built for high-power hydrogen-powered shunting locomotives. It marks substantive progress in the application of hydrogen energy to heavy-haul railways, addresses the high-emission pain point of traditional locomotives, and verifies the stability of high-flow hydrogen refueling equipment under extreme cold and high-load operating conditions.

III. Summary and Outlook

In Q1 2026, China's hydrogen energy industry has entered a pragmatic stage focusing on economic efficiency calculation. From the utilization of coke oven gas in Xinjiang to hydrogen refueling for railways in Inner Mongolia, the industrial development logic is shifting from policy-driven alone to multi-dimensional driving led by resources, application scenarios and economic viability, which is expected to reshape the energy consumption pattern of industrial and transportation sectors.