SMM May 6 News:

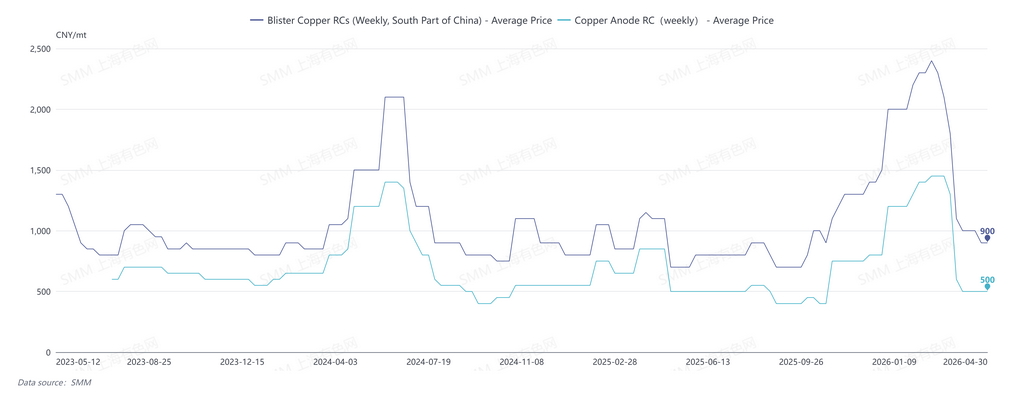

On April 30, SMM's monthly blister copper RCs in south China was 850-1,050 yuan/mt, with an average of 950 yuan/mt, down 850 yuan/mt MoM.

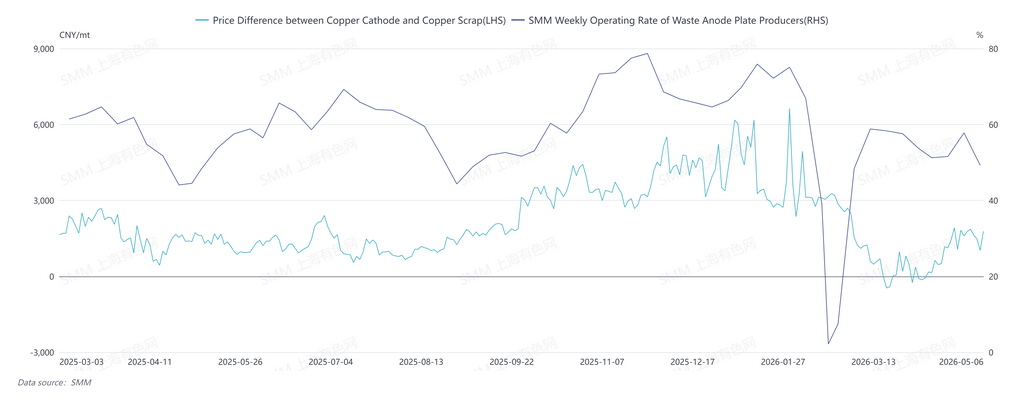

After Q2 2026, the blister copper market entered a tight state, and blister copper RCs in China reached an inflection point after March and pulled back rapidly. The primary reason was a supply decline: copper prices weakened after mid-to-late March, and the narrowing price difference between primary metal and scrap reduced copper scrap supply. Combined with the disruption from policy tightening, both factors led to a decline in the supply of scrap-derived blister copper and copper anodes. Meanwhile, smelters entered a concentrated maintenance period in Q2, driving up demand for copper anodes, thus tightening the supply-demand pattern.

On April 30, SMM's weekly blister copper RCs in south China was 800-1,000 yuan/mt, with an average of 900 yuan/mt; the weekly copper anode RCs in China was 450-550 yuan/mt, with an average of 500 yuan/mt.

SMM expects the tight blister copper market to see little improvement in May. Although copper anodes from DRC's Kamoa copper smelting facility (with annual blister smelting capacity of 500,000 mt), which commenced production at year-end 2025, have been gradually arriving in China and import supply may increase, the core issue remains the supply constraints on domestic scrap-derived blister copper and copper anodes. On one hand, copper prices are in a volatile adjustment trend, and if the price difference between primary metal and scrap fails to widen, it will be difficult to support large volumes of secondary copper flowing into the smelting segment. On the other hand, the market is currently heavily influenced by policy direction—strict requirements on invoices combined with reduced policy and financial support have caused tight tax-inclusive raw material supply, rising wait-and-see sentiment among producers, and declining production willingness in the short term. Additionally, a producer of ore-derived copper anodes is commissioning refining capacity in May, which will also reduce the circulating volume of ore-derived copper anodes in the market.

Demand side, smelters will still be undergoing maintenance in May and June, and as cold charge inventory levels at smelters tend to gradually decline, market demand is expected to remain firm.

Overall, market supply is expected to see little growth in May, and blister copper RCs in China are unlikely to rebound. In the short term, policy direction and copper price trends will be the key variables.