Recently, major PV listed enterprises have successively disclosed their 2025 annual reports. Based on these publicly available annual report data, a comprehensive review of the industry's overall operational trajectory and development trends is as follows:

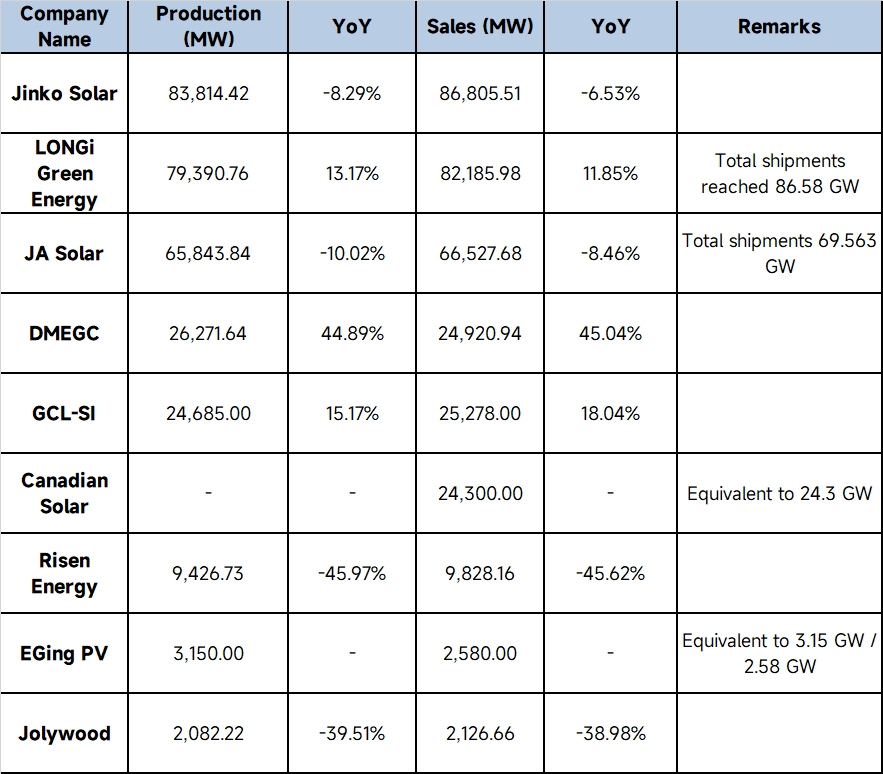

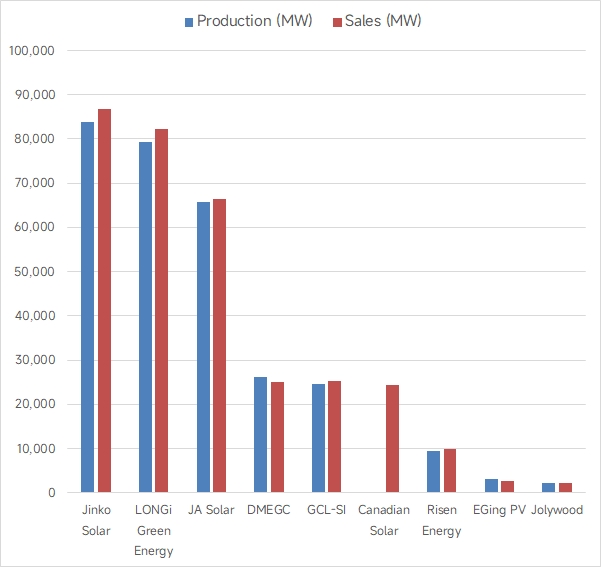

Source: Annual reports of respective companies, 2025

In 2025, after a period of rapid expansion, China's PV module enterprises entered a critical phase of deep adjustment and strategic transformation.

I. Overall Development

1 Supply-demand mismatch and profitability under pressure: The industry faced severe overcapacity, periodic supply-demand imbalance, and cutthroat low-price competition driven by involution, compounded by fluctuations in raw material prices such as polysilicon and silver paste, which severely compressed profit margins across the industry chain. Most top-tier enterprises, including Jinko Solar, LONGi Green Energy, JA Solar Technology, Jolywood, and Yijing Solar, saw declines in operating revenue accompanied by significant losses.

2 Clear divergence, with some enterprises achieving counter-cyclical profitability: Against the backdrop of industry-wide pressure, a few enterprises achieved profitability against the trend through differentiated strategies or diversified businesses. For example, DMEGC achieved growth in both revenue and net profit through differentiated products (all-black modules, greenhouse systems, etc.) and forward-looking supply chain synergies; Canadian Solar Inc., supported by its rapidly growing energy storage business, delivered strong profit performance, with net profit reaching 1.016 billion yuan.

3 Market landscape shifting outward, with emerging markets becoming growth engines: The Chinese market experienced a notable slowdown in installation growth due to power grid absorption bottlenecks and policy adjustments. Facing trade barriers and policy uncertainties in traditional markets such as Europe and the US, Chinese enterprises accelerated their expansion into emerging markets including the Middle East, Africa, Latin America, and Southeast Asia, where rapidly growing PV demand became a key driver to boost China's module exports.

4 Strategic transformation and capacity going global: The development logic of enterprises shifted comprehensively from "competing on scale and price" to "competing on technology, quality, and value." To cope with increasingly high international trade barriers (such as anti-dumping and countervailing duty investigations, the UFLPA Act in the US, and localization requirements in the Middle East), PV enterprises accelerated the nearshoring or localization of critical global supply chains and advanced overseas capacity construction.

II. Current Development Trends of PV Modules

In response to industry cycles and changes in end-use demand, the technology and market development of PV modules at the current stage exhibit the following distinct trends:

First, N-type technology achieved full dominance, with perovskite tandem cells becoming an R&D focus: P-type (PERC) cells had largely exited the mainstream market, fully replaced by N-type technology. Among them, TOPCon technology held an absolute dominant position, with mass production efficiency continuously breaking through. Meanwhile, HJT (heterojunction) and BC (back contact) technologies were also accelerating large-scale mass production, capturing high-end markets with advantages such as high conversion efficiency, high bifaciality, and aesthetic appeal. Regarding next-generation frontier technologies, crystalline silicon-perovskite tandem cells were the R&D focus of major enterprises, with laboratory conversion efficiencies frequently setting new world records (e.g., Jinko surpassing 34.76% and LONGi surpassing 35.1%), pointing the way toward breaking through crystalline silicon efficiency limits.

Second, "silver reduction" and "wafer thinning" dominated cost reduction and efficiency improvement: Due to sharp increases in silver prices, silver paste became the largest cost item for battery modules, and "silver reduction" or "silver elimination" became the core industry consensus for cost reduction. Enterprises widely adopted 0BB (zero busbar) technology, silver-coated copper paste, and even pure copper electroplating and other new-type metallization technologies to significantly reduce silver consumption. Additionally, continuous thinning of silicon wafer thickness was an important trend for reducing silicon consumption and production costs.

Third, application scenarios became segmented, with products moving toward customization and differentiation: A single standard module could no longer meet market demand, and enterprises launched customized products deeply adapted to different scenarios. For example:

- "Offshore PV modules" for high salt spray and strong wind-wave environments in marine/tidal flat areas.

- "Anti-dust accumulation and sand-resistant modules" for desert-Gobi-wasteland and other hot, arid, and sandy regions.

- "Anti-glare modules" for light-sensitive areas such as airports and highways.

- "All-black modules," "colored modules," "balcony PV," and "lightweight modules" for distributed rooftop and building-integrated PV (BIPV).

Fourth, "PV+ESS integration" became an inevitable path: As the grid connection ratio of new energy increased, addressing the intermittency and fluctuations of PV power generation became a rigid demand, and the energy storage market was shifting from "mandatory energy storage allocation" to "economically driven voluntary energy storage allocation." Module enterprises were accelerating their transformation into "integrated green energy system solution providers," enhancing power grid stability and project returns through PV+ESS integration (covering large-scale ground-mounted, commercial and industrial, and household ESS). Fifth, stricter green low-carbon and ESG requirements: Facing global carbon constraint mechanisms (such as the EU CBAM), the low-carbon footprint of modules has become an important market access threshold. Enterprises significantly reduced the full life cycle carbon emissions of products by using composite/steel frames to replace traditional aluminum frames, applying secondary polysilicon and retired module recycling technologies, building a green supply chain moat.

![[SMM PV] Diversified Development: First Enters the Supply Chain of China's Leading PCB Enterprises](https://imgqn.smm.cn/usercenter/XoZQc20251217171737.jpg)

![[Solar: India rejects blanket extension for ALMM-II cell deadline]](https://imgqn.smm.cn/usercenter/WUJtg20251217171743.jpg)

![Polysilicon Spot Cargo Weakened, High Prices in the Mid-Layer Sand Range Slightly Adjusted Downward [SMM Silicon-Based PV Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/GHTIQ20251217171741.jpg)