SMM Apr 28 News:

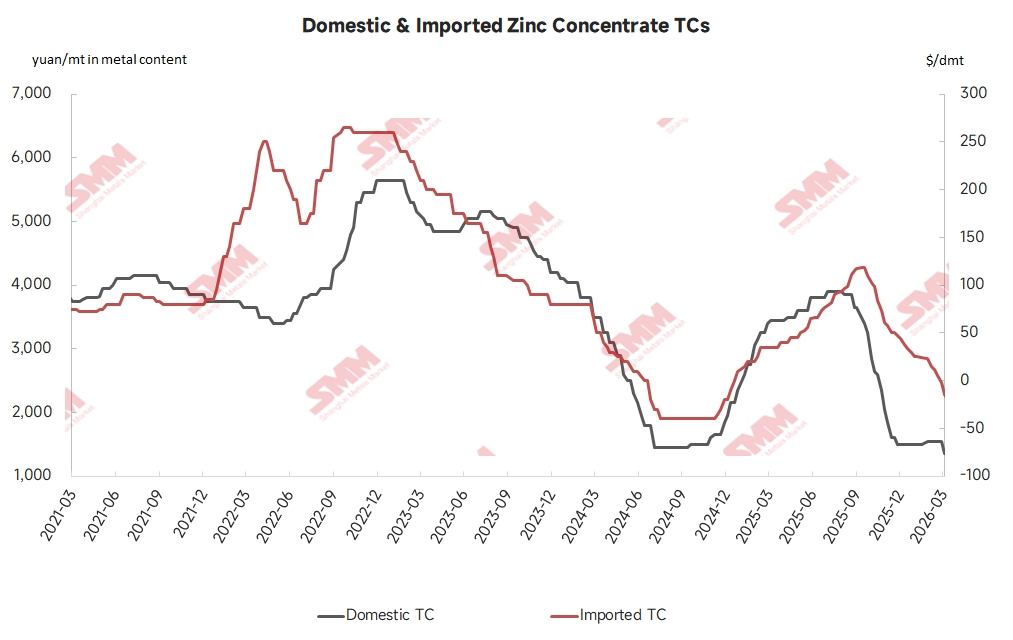

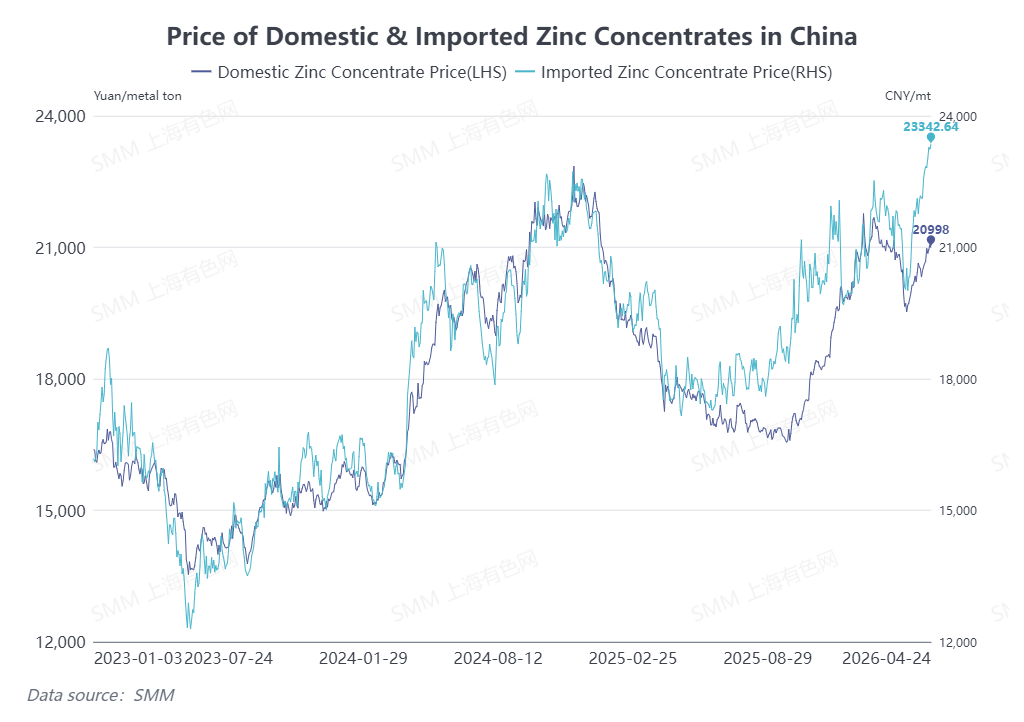

As of April 24, the average domestic zinc concentrate TC dropped to 1,050 yuan/mt in metal content, and the imported zinc concentrate TC fell to -$36.13/dmt. Overall, zinc concentrate TCs continued to decline, with imported zinc concentrate TCs deepening further into negative territory. In May, domestic zinc concentrate TCs in multiple regions plan to further drop to three-digit levels. Why is this happening?

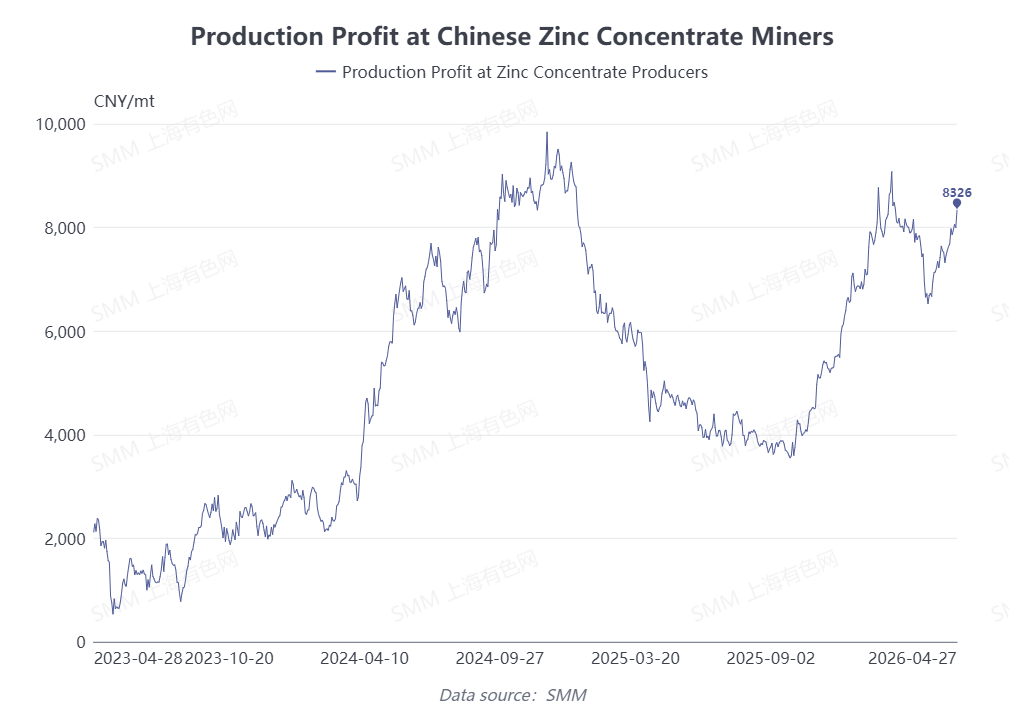

Supply side. Q2 is the regular production resumption season for domestic mines. Previously shut-down domestic mines gradually resumed production. Combined with rising zinc prices and low TCs, domestic zinc concentrate profits currently exceed 8,000 yuan/mt in metal content, and domestic mines actively resumed production, with overall production recovering largely on schedule. However, in terms of new capacity, the main incremental source this year is the Huoshaoyun mine, but the volume of ore flowing out from the Huoshaoyun mine is relatively small. As of now, the Huoshaoyun mine has only held one external tender this year, contributing limited supply to the domestic circulation market. Other new capacity is mostly expected to be released in H2 and is relatively small in scale, providing almost no notable supplement to domestic ore supply in H1.

Import market. In Q1, Australia experienced frequent severe weather including floods and typhoons, which affected zinc concentrate transportation. Although overall transportation largely recovered in April, shipment schedules were delayed. Based on shipping cycles, this is expected to affect Australian zinc concentrate arrivals in China from April to May. Moreover, according to customs data, China imported a total of 1.09 million mt of zinc concentrates from Australia in 2025, ranking first among all source countries by imports. Therefore, the periodic reduction in imported ore directly affected domestic ore market supply.

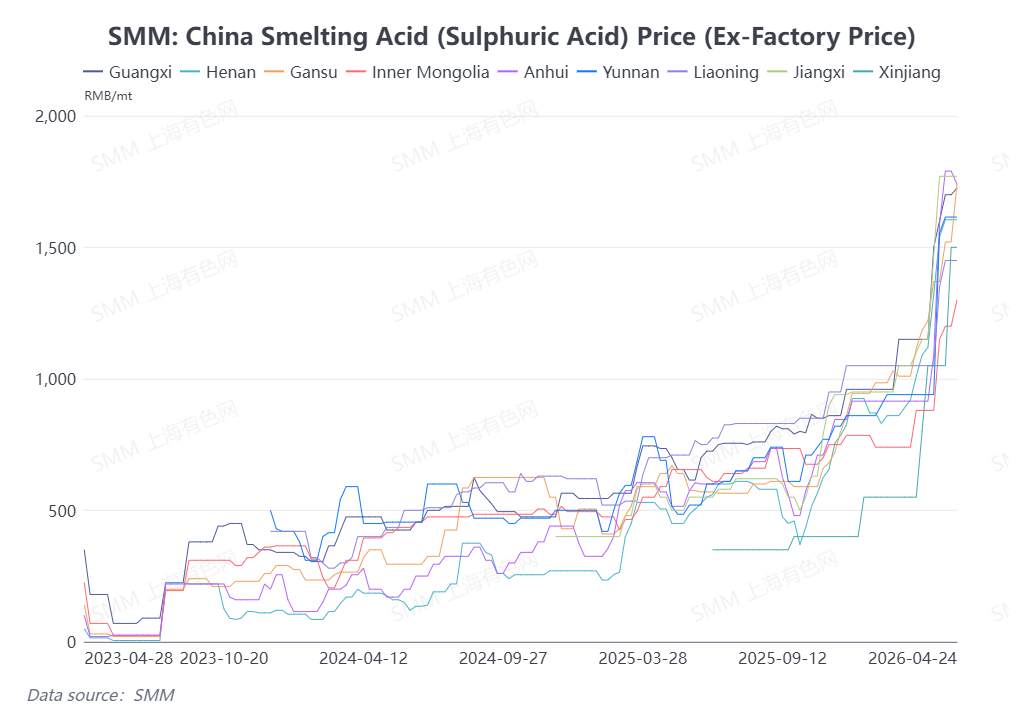

Demand side. After Chinese New Year, domestic smelters gradually recovered. Although domestic and imported zinc concentrate TCs continued to decline, sulphuric acid prices rose significantly, with ex-factory prices in multiple domestic regions recently rising to around 1,300-1,800 yuan/mt. According to SMM estimates, smelter revenue including sulphuric acid and TCs can basically cover production costs. Factoring in revenue from other metals contained in zinc concentrates, most domestic smelters still maintain certain profit margins.

Overall, supported by by-product profits, domestic smelters actively operated, with robust demand for zinc concentrates in April and May. In addition, the zinc domestic-to-overseas price ratio continued to deteriorate. According to SMM estimates, as of April 24, importing zinc concentrates into China incurred losses exceeding 2,000 yuan/mt in metal content. Therefore, considering the overall price advantage, smelters chose to actively purchase domestic zinc concentrates, driving domestic zinc concentrate TCs to decline rapidly.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Monthly Production Declined: Refined Zinc Faces Dual Pressure from Raw Material Supply and Costs [SMM Analysis]](https://imgqn.smm.cn/usercenter/qdibi20251217171755.jpg)