SMM News, April 22:

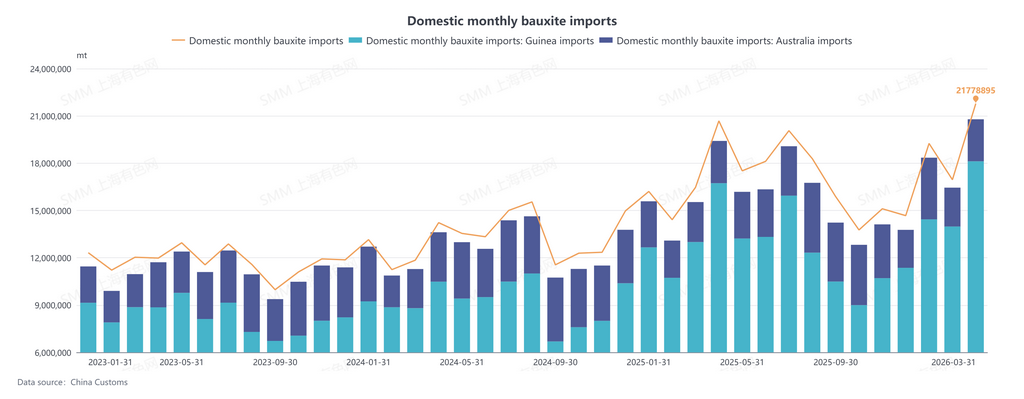

According to the General Administration of Customs, domestic bauxite imports reached 21.78 million tons in March 2026, rising 28.5% month-on-month and 32.3% year-on-year, hitting a record high for single-month imports. From January to March 2026, cumulative domestic bauxite imports stood at 57.98 million tons, a year-on-year increase of 23.1%.In March 2026, domestic imports of Guinean bauxite amounted to 18.12 million tons, up 29.6% month-on-month and 39.4% year-on-year. During the first three months of 2026, cumulative imports of Guinean bauxite reached 46.541 million tons, climbing 27.9% year-on-year. (HS Code: 26060000)

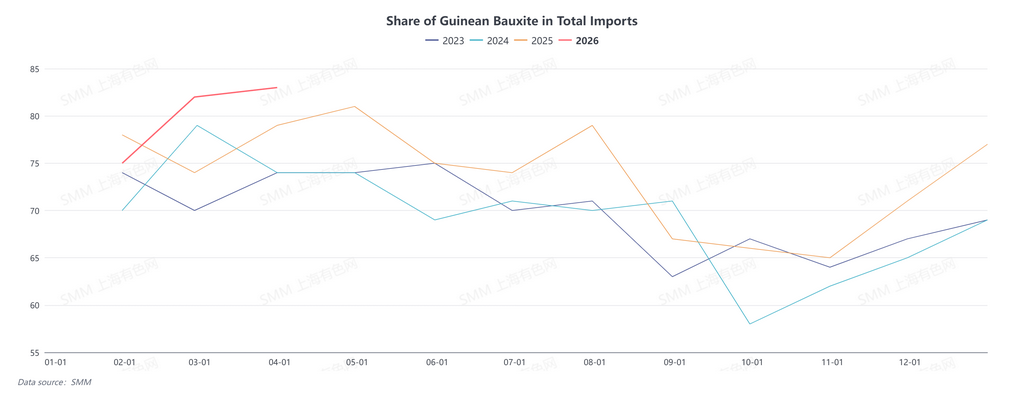

In the first quarter of 2026, Guinean bauxite accounted for over 80% of total domestic bauxite imports. Driven by the commissioning of new bauxite projects, the resumption of suspended operations and capacity expansion at existing mines, Guinea’s monthly bauxite exports have climbed continuously, leading to a rising concentration of domestic bauxite import sources. Nevertheless, such concentration is unlikely to rise further in the following period, mainly for the reasons below:

- Domestic alumina demand sees limited growth, and the local market has shifted to a net alumina import pattern. Bauxite demand is expected to decline rather than expand. With steady domestic bauxite output, overall demand for imported bauxite will weaken.

- Guinea plans to introduce relevant policies to curb bauxite export volumes and extend its local aluminum industrial chain, which will cap unlimited growth in the nation’s bauxite exports.

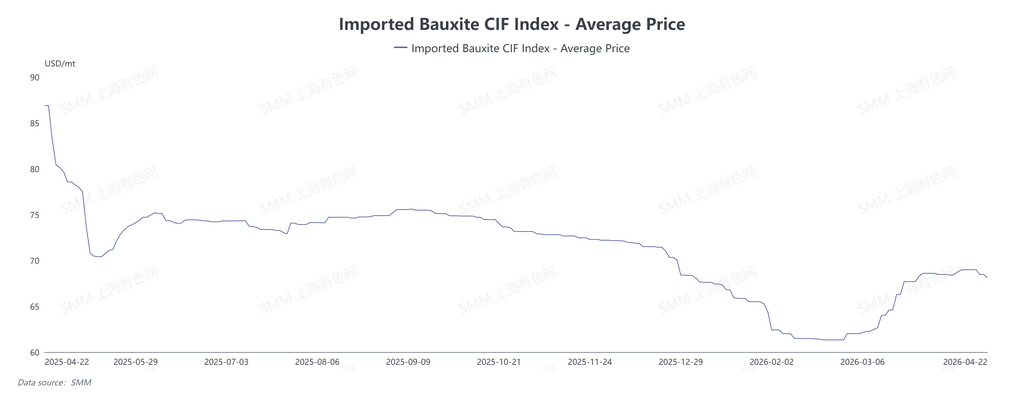

In February, market rumors spread that Guinea would formulate policies to restrict bauxite exports. Affected by the news, imported bauxite prices halted declines and rebounded. Meanwhile, surging ocean freight rates amid geopolitical tensions in the Middle East pushed up bauxite CIF prices. By mid-April, the SMM imported bauxite CIF index rebounded to a peak of USD 68.99 per ton, rising by USD 7.66 per ton from the February low. Latest market information indicates that detailed policy updates will be released from late April to early May, later than the previously expected early April timeline, cooling bullish market sentiment.

In mid-to-late April, bauxite freight rates edged lower. Coupled with high port inventories and sufficient circulating cargo supply, buyers lowered their offered prices, and market acceptance of high-priced cargo weakened alongside growing wait-and-see sentiment, resulting in a slight downward shift in spot bauxite prices.

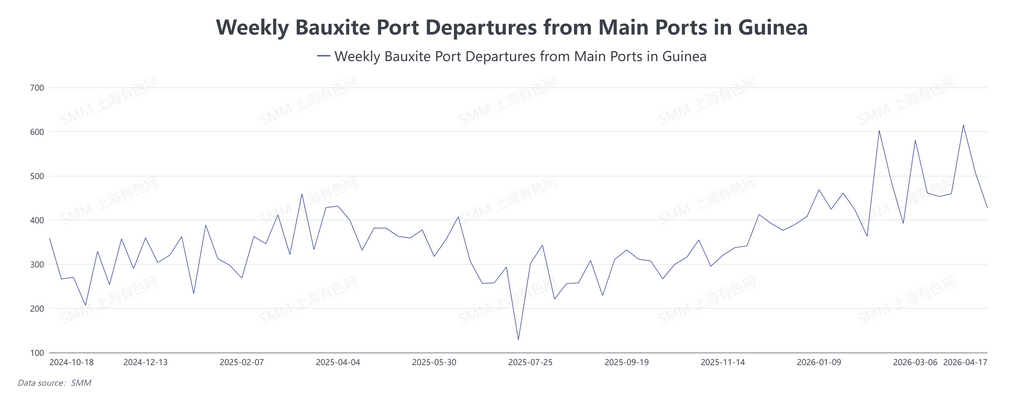

Judging from bauxite shipment volumes at major Guinean ports, shipment levels in February and March were higher than those recorded in January and February. Based on shipping schedules, average daily arrivals of Guinean bauxite are expected to increase month-on-month in April. In addition, Guinean bauxite shipments have remained stable since March, while Australian bauxite exports have not posted notable declines. From May to mid-June, overall domestic bauxite arrivals will stay at a high level, with imported volumes remaining elevated in the short term. Ample domestic bauxite supply will cap upward price momentum and put pressure on price highs.