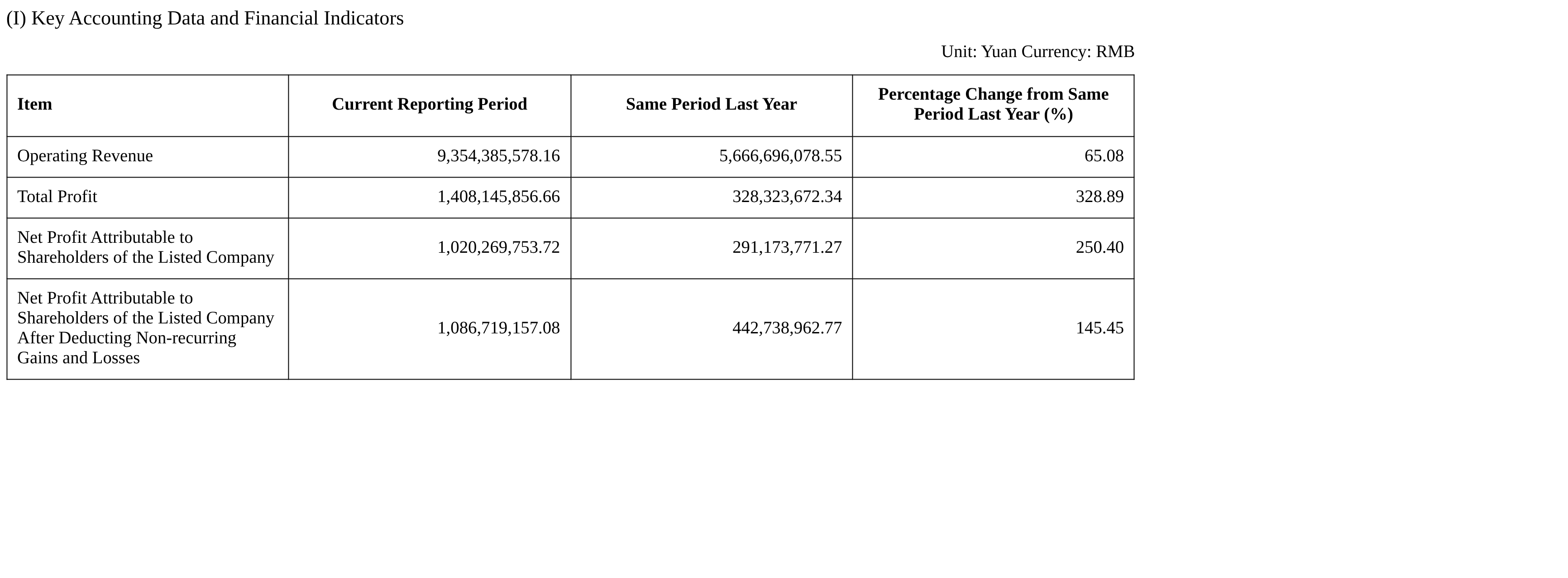

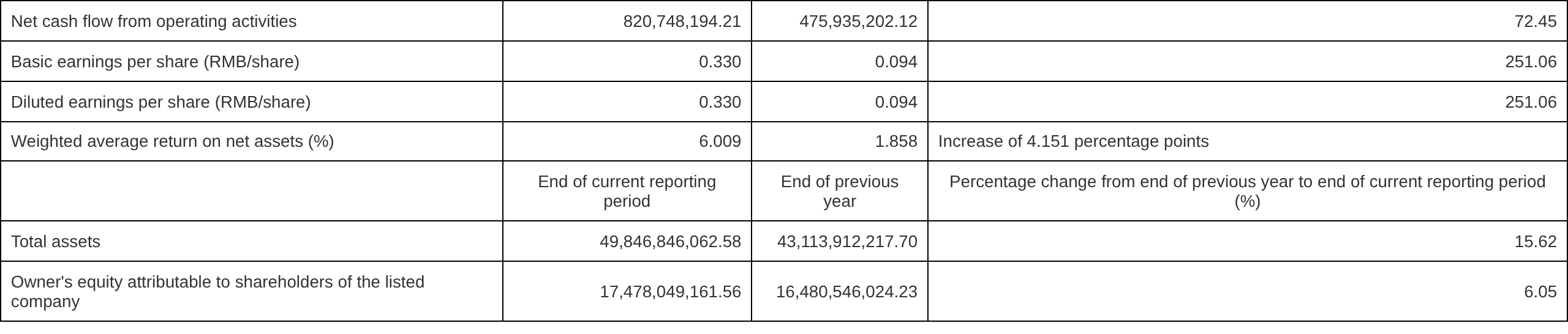

Le soir du 20 avril, le rapport du premier trimestre de Chengtun Mining a montré que l'entreprise a réalisé un chiffre d'affaires total de 9,354 milliards de yuans, en hausse de 65,08 % en glissement annuel ; le bénéfice net attribuable à la société mère s'est élevé à 1,02 milliard de yuans, en hausse de 250,40 % en glissement annuel.

Concernant les principales raisons de l'augmentation du chiffre d'affaires et du bénéfice net au premier trimestre, Chengtun Mining a indiqué que les volumes de production et de vente de ses principaux produits en cuivre ont augmenté en glissement annuel, que les prix du cuivre ont progressé en glissement annuel et que la rentabilité s'est améliorée ; l'entreprise a renforcé la qualité et l'efficacité de sa production et de ses opérations, les coûts maîtrisables ont diminué en glissement annuel et les performances ont progressé sur la période.

Par ailleurs, Chengtun Mining a également annoncé le 20 avril que, à la date de publication, le montant cumulé total des garanties externes en cours de la société cotée et de ses filiales contrôlées s'élevait à 10,854 milliards de yuans, représentant 65,86 % des actifs nets audités les plus récents de la société cotée. Parmi celles-ci, le montant cumulé total des garanties accordées aux entreprises associées s'élevait à 172,04 millions de yuans ; le montant cumulé total des garanties accordées aux filiales contrôlées s'élevait à 10,682 milliards de yuans, représentant 64,82 % des actifs nets audités les plus récents de la société cotée. Aucune des garanties externes de l'entreprise n'était en souffrance.

Chengtun Mining a annoncé le 8 avril que sa filiale en propriété exclusive Preeminence Holdings Limited prévoit d'acquérir 50 % du capital de Nkoyi Leopard Mining and Investment Limited, filiale en propriété exclusive de Novel Mining and Services Limited, société enregistrée dans l'Émirat d'Abu Dhabi, aux Émirats arabes unis, pour 300 millions de dollars, obtenant ainsi indirectement une participation de 30 % dans des droits miniers spécifiques de cuivre-cobalt situés en RDC. À l'issue de cette transaction, Nkoyi deviendra une entreprise associée de la société et ne sera pas consolidée dans les états financiers. Aux termes de l'accord, Preeminence prévoit d'acquérir 50 % du capital de Nkoyi pour 300 millions de dollars. La filiale en propriété exclusive de Nkoyi a conclu un accord de coentreprise portant sur des droits miniers spécifiques de cuivre-cobalt, détenant une participation de 60 % dans ces droits miniers. Par conséquent, après cette transaction, l'entreprise détiendra une participation de 30 % dans ces droits miniers. Nkoyi a été créée en octobre 2024 et n'a pas encore commencé ses activités de production ou d'exploitation ; son actif principal est la participation susmentionnée de 60 % dans le projet minier de cuivre-cobalt. La contrepartie, Novel Mining, a été créée en mars 2026 et enregistrée à Abu Dhabi, son projet principal étant les droits miniers sur le cuivre et le cobalt.

Le 2 avril, Chengtun Mining a répondu aux questions des investisseurs sur une plateforme interactive, déclarant que la société surveille en permanence les risques pertinents dans ses sites d'exploitation à l'étranger, et que ses projets opérationnels en RDC fonctionnent actuellement de manière stable.

Le 2 avril, Chengtun Mining a répondu aux questions des investisseurs sur une plateforme interactive, déclarant que pour gérer efficacement les fluctuations des prix des métaux non ferreux et les risques de change, la société a adopté plusieurs mesures de gestion des risques, notamment la couverture et le verrouillage des prix de vente d'une partie des stocks de produits miniers et des produits en cuivre, or et autres par le biais de contrats à terme vendeurs. Lorsque les prix de marché des produits métalliques augmentent, les pertes se reflètent du côté des contrats à terme. En 2025, les prix de marché du cuivre, de l'or et d'autres métaux ont augmenté de manière significative, entraînant d'importantes pertes latentes du côté des contrats à terme, compensées par des gains correspondants du côté des marchandises au comptant. L'équipe de contrats à terme mènera avec diligence les opérations de couverture de manière prudente, centrées sur l'activité principale de la société, dans le cadre des systèmes de gestion de la société.

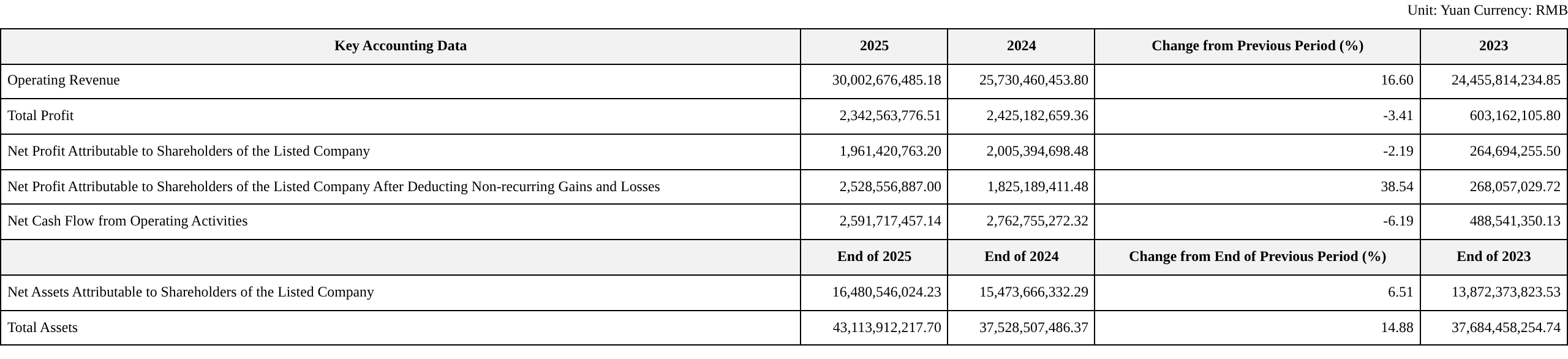

Le rapport annuel 2025 précédemment publié par Chengtun Mining a montré qu'en 2025, l'industrie mondiale des métaux non ferreux est entrée dans une nouvelle phase de développement caractérisée par la restructuration de l'offre et de la demande et la réévaluation de la valeur. Les métaux énergétiques tels que le cuivre, le cobalt et le nickel ont été stimulés par la demande rigide des secteurs des nouvelles énergies, de la puissance de calcul de l'IA, de la modernisation des réseaux électriques mondiaux et d'autres secteurs, conjuguée à des contraintes rigides du côté de l'offre, poussant le centre de prix continuellement à la hausse. Les métaux précieux tels que l'or ont vu une opportunité de valorisation dans un contexte de conflits géopolitiques mondiaux et de demande croissante de valeurs refuges. L'industrie des batteries pour nouvelles énergies a réalisé une progression de haute qualité grâce à des opportunités structurelles. Face aux nouvelles opportunités de développement du secteur, la société a maintenu sa stratégie axée sur les ressources et l'internationalisation, approfondi sa disposition sur l'ensemble de la chaîne industrielle consistant à « contrôler les ressources en amont et développer les matériaux en aval », renforcé les mesures opérationnelles de « maîtrise des coûts, attention aux détails et amélioration de la qualité et de l'efficacité », consolidé en permanence ses capacités fondamentales en matière d'exploration, de construction et d'exploitation des ressources mondiales, et amélioré la valeur d'extension de la chaîne industrielle dans la fonderie, la transformation et la fabrication de matériaux, renforçant continuellement la qualité opérationnelle et la résilience face aux fluctuations cycliques dans un contexte de restructuration de la valeur du secteur. En 2025, l'entreprise a réalisé de nouvelles percées dans le déploiement mondial des ressources et les capacités opérationnelles de la chaîne industrielle. Les projets clés à l'étranger ont obtenu des résultats remarquables en matière d'amélioration de la qualité et de l'efficacité. Après l'achèvement de l'expansion de la Phase II du projet de fonderie de cuivre BMS, la capacité a augmenté significativement, atteignant 120 000 tonnes en contenu métallique en fin d'année, avec une production annuelle de 106 300 tonnes en contenu métallique, et la résilience de la rentabilité de l'activité cuivre-cobalt a continué de se renforcer. Le projet intégré d'exploitation minière et de fonderie de Kalongwe en RDC a mené une transformation technologique et une construction d'ingénierie sur l'ensemble du processus, réalisant des améliorations globales en matière de contrôle qualité des produits, de réduction de la consommation énergétique de production, d'utilisation intégrée des ressources et de gestion affinée des coûts. Youshan Nickel en Indonésie a maintenu des opérations stables malgré les fluctuations du secteur. Le segment national a progressé sur plusieurs fronts : le projet du Guizhou a davantage libéré la valeur d'extension de la chaîne industrielle, Huajin Mining a réalisé une croissance régulière de la production d'or, et la construction de la mine de cuivre Dali Sanxin a progressé de manière ordonnée. En 2025, l'entreprise a réalisé un chiffre d'affaires de 30,003 milliards de yuans, en hausse de 16,60 % en glissement annuel ; le bénéfice net attribuable aux actionnaires de la société cotée s'est élevé à 1,961 milliard de yuans, en baisse de 2,19 % en glissement annuel.

Chengtun Mining a déclaré dans son rapport annuel 2025 que l'entreprise se consacre au développement et à l'utilisation des ressources en métaux énergétiques, en particulier les variétés métalliques nécessaires aux batteries pour les nouvelles énergies, tout en se développant dans les métaux précieux tels que l'or.L'entreprise se concentre sur le cuivre, le nickel, le cobalt et l'or.Ses principaux segments d'activité comprennent les métaux énergétiques, les métaux de base, le négoce de métaux et autres.

Concernant ses principales activités opérationnelles, Chengtun Mining a fourni l'aperçu suivant :

1. Activité métaux énergétiques :Au cours de la période de reporting, l'activité métaux énergétiques de l'entreprise a réalisé un chiffre d'affaires de 20,384 milliards de yuans, avec une marge brute de 25,69 %, en baisse de 2,71 points de pourcentage par rapport à l'année précédente. En 2025, la production de produits en cuivre a atteint 207 400 tonnes en contenu métallique, en hausse de 17,48 % par rapport à l'année précédente ; le chiffre d'affaires des produits en cuivre a atteint 14,071 milliards de yuans, en hausse de 34,20 % en glissement annuel, avec une marge brute de 28,88 %, en baisse de 6,35 points de pourcentage en glissement annuel ; la production de produits en cobalt a été de 9 200 tonnes en contenu métallique, en baisse de 30,58 % par rapport à l'année précédente, avec un chiffre d'affaires de 1,011 milliard de yuans, en baisse de 30,64 % par rapport à l'année précédente, et une marge brute de 53,76 %, en hausse de 10,21 points de pourcentage par rapport à l'année précédente ; la production de produits en nickel a été de 49 400 tonnes en contenu métallique, en hausse de 50,42 % par rapport à l'année précédente, avec un chiffre d'affaires de 4,286 milliards de yuans, en hausse de 13,16 % par rapport à l'année précédente, et une marge brute de 0,32 %, en baisse de 3,25 points de pourcentage par rapport à l'année précédente. (1) Segment cuivre-cobalt : ① La société a activement fait progresser la production, la construction, l'amélioration de la qualité et le renforcement de l'efficacité de son segment cuivre-cobalt en RDC. À la fin de la période de reporting, la capacité totale de production de cuivre de la société en RDC atteignait 230 000 tonnes en contenu métallique par an. Les projets de fonderie cuivre-cobalt CCR et CCM de la société ont maintenu une production et des opérations stables tout en optimisant continuellement les flux de processus, maintenant les taux de conformité des produits à des niveaux élevés. BMS a achevé avec succès son expansion de Phase II, entrant officiellement dans le rang des entreprises disposant d'une capacité de production annuelle de cuivre supérieure à 120 000 tonnes en contenu métallique. Le projet cuivre-cobalt de Kalongwe a coordonné la transformation technologique de l'ensemble du processus et la construction d'ingénierie en 2025, achevant avec succès la mise en œuvre des projets de transformation technologique essentiels, réalisant des améliorations globales en matière de contrôle qualité des produits, de réduction de la consommation énergétique de production, d'utilisation intégrée des ressources et de gestion affinée des coûts, avec des résultats significatifs en termes de réduction des coûts et d'amélioration de l'efficacité. ② Dali Sanxin a activement traité les permis liés à la construction de la mine et a obtenu le rapport d'approbation du projet, entre autres. Les procédures d'utilisation des terres et d'évaluation de la sécurité et de l'environnement progressent de manière régulière. ③ Au cours de la période de reporting, la société a activement recherché une sécurité durable des ressources par l'exploration dans des zones à fort potentiel et la poursuite d'opportunités de fusions-acquisitions et de coopération pour des ressources de minerai de cuivre. (2) Segment nickel en Indonésie : Au cours de la période de reporting, le projet Youshan Nickel a atteint une production et des opérations stables. En 2025, les prix du nickel ont globalement fluctué à la baisse dans un contexte de suroffre, avec un rebond en fin d'année dû aux perturbations liées à la politique indonésienne. Grâce à des mesures globales incluant l'amélioration de la gestion, l'optimisation des processus de production et l'organisation rationnelle de la production et des opérations, ainsi que la création de synergies dans la chaîne industrielle avec les industries nationales connexes, la résistance aux risques de la chaîne industrielle a été renforcée. La société continuera à rechercher des opportunités de développement supplémentaires dans le segment nickel, tant du côté des ressources minières que du côté de la fonderie. (3) Segment transformation en profondeur et matériaux : ① En 2025, dans un contexte de grave pénurie de matières premières causée par l'« interdiction d'exportation de cobalt » de la RDC, Kelixin a réalisé une maximisation de la valeur grâce à un contrôle précis du rythme de production et d'expédition et à une allocation efficace des ressources limitées en matières premières. ② Zhonghe Nickel a optimisé la technologie de procédé, approfondi la gestion raffinée des sites de production, obtenu des résultats dans le contrôle des procédés pour les matériaux de type laitier à haute teneur en magnésium, et amélioré l'adaptabilité du système aux matières premières provenant de multiples canaux. ③ Fin décembre 2025, le projet Phase I du Guizhou a achevé sa montée en puissance et atteint le plein régime de production, tandis que la construction du projet Phase II du Guizhou progressait activement. La société a mené un benchmarking systématique des procédés, optimisé davantage les flux de procédés du système, renforcé les exigences de gestion et de contrôle raffinés pour les différentes tâches, et assuré le fonctionnement continu et stable des systèmes de production.

2. Activité métaux de base : (1)Au cours de la période considérée, Chengtun Zinc & Germanium a exploité sa fonderie de zinc à pleine capacité et récupéré de manière exhaustive les métaux précieux, notamment le germanium, l'argent, le cuivre, l'indium et l'or. La production de produits à base de germanium a augmenté de 37,18 % en glissement annuel, et l'industrialisation de la récupération globale de l'indium métallique a connu un succès par étapes.Une percée a été réalisée dans la technologie de contrôle des fours de fusion, avec des volumes de traitement des laitiers et des taux de récupération des métaux précieux en amélioration constante, et des bénéfices économiques significativement renforcés. (2) Au cours de la période considérée, la société a activement fait avancer le traitement des permis miniers nationaux afin d'assurer une construction ordonnée. Baoshan Hengyuan Xinmao a obtenu l'approbation de la NDRC provinciale pour le projet d'ingénierie minière en septembre 2025. Huajin Mining a fonctionné conformément au plan en 2025, vendant 320,75 kg d'or et réalisant un chiffre d'affaires de 244 millions de yuans. 3. Activité de négoce de métaux et autres : Au cours de la période considérée, le négoce de métaux a réalisé un chiffre d'affaires de 999 millions de yuans, en baisse de 24,46 % en glissement annuel, ne représentant que 3,33 % du chiffre d'affaires total. Actuellement, l'activité principale de la société connaît une croissance régulière. Alors que l'échelle et la proportion de la production industrielle et manufacturière ont augmenté, l'échelle de l'activité de négoce a été progressivement réduite, obtenant de bons résultats sur la voie d'un développement de haute qualité, durable et stable.

Concernant le plan d'activité de la société, Chengtun Mining a déclaré :En 2026, les objectifs de production et d'exploitation de la société sont : production de produits cuivrés de 230 000 tonnes en contenu métallique ; production de produits cobaltifères de 15 000 tonnes en contenu métallique ; production de produits nickelifères de 60 000 tonnes en contenu métallique ; production de produits zincifères de 300 000 tonnes ; et production de produits aurifères de 380 kg. Dans d'autres domaines, les mines nationales comprennent la poursuite de la construction à grande échelle et de la mise en service de la mine de cuivre Dali Sanxin, l'avancement du projet minier Baoshan Hengyuan Xinmao conformément au calendrier prévu, l'augmentation de la production de Huajin Mining et la mise en service complète du projet Phase II du Guizhou. Compte tenu de l'environnement de marché complexe et volatil, ce plan d'activité ne sert que d'indicateur directeur, est soumis à des incertitudes et ne constitue pas un engagement à atteindre les objectifs de production énoncés. Afin de protéger les intérêts de l'ensemble des actionnaires, la société se réserve le droit de réviser ce plan d'activité en temps opportun en fonction de l'évolution des conditions de marché, des ajustements de politique sectorielle et des besoins réels de production et d'exploitation. Il est conseillé aux investisseurs de prêter une attention particulière aux risques spécifiques au secteur, de reconnaître rationnellement les incertitudes des informations prévisionnelles et de prendre des décisions d'investissement prudentes.

Citi a relevé sa prévision du prix du cuivre à 0-3 mois à 13 000 $ par tonne.

ANZ estime que la résilience de la demande portée par la transition énergétique et la croissance des centres de données maintiendra le marché dans un déficit d'approvisionnement de 4 % à 5 %, soutenant ainsi les prix du cuivre.

Un rapport de recherche de Huafu Securities daté du 8 mars indiquait : Cuivre — à court terme, les anticipations de baisse des taux de la Fed américaine persistent et les fondamentaux tendus continuent de soutenir les prix du cuivre ; à moyen et long terme, des baisses de taux plus prononcées de la Fed stimulant l'investissement et la consommation tout en ouvrant des marges de manœuvre pour la politique monétaire chinoise, conjuguées à un potentiel rebond inflationniste lié à un éventuel assouplissement budgétaire de l'administration Trump, devraient entraîner un déplacement à la hausse du centre de gravité des prix du cuivre, et la forte demande liée aux nouvelles énergies creusera l'écart offre-demande, maintenant une perspective haussière sur les prix du cuivre. Aluminium — à court terme, les prix de l'aluminium sont principalement portés par le sentiment macroéconomique et les flux de capitaux. Actuellement, l'ampleur de la hausse des prix de l'aluminium dépendra de la durée du blocus du détroit ; si la perturbation du transport maritime est brève, l'impact sur les prix devrait être limité, mais un blocus prolongé pourrait pousser les prix de l'aluminium vers de nouveaux sommets. Actions individuelles : Cuivre — focus sur Zijin, CMOC, JCC, Chengtun Mining, Zangge, Jchx et Beibu-Gulf Copper, et pour les actions H, focus sur China Nonferrous Mining et Minmetals, etc. Aluminium — focus sur Hongqiao Holdings, Tianshan, Yunnan Aluminum, Shenhuo, Huatong et Zhongfu, etc.

![Hunan Shizhuyuan Nonferrous Metals a lancé aujourd'hui un appel d'offres pour 800 tonnes métriques de concentrés de bismuth en contenu physique pour livraison en juillet [Rapport de suivi du marché du bismuth de SMM]](https://imgqn.smm.cn/usercenter/mLwgx20251217171723.jpeg)