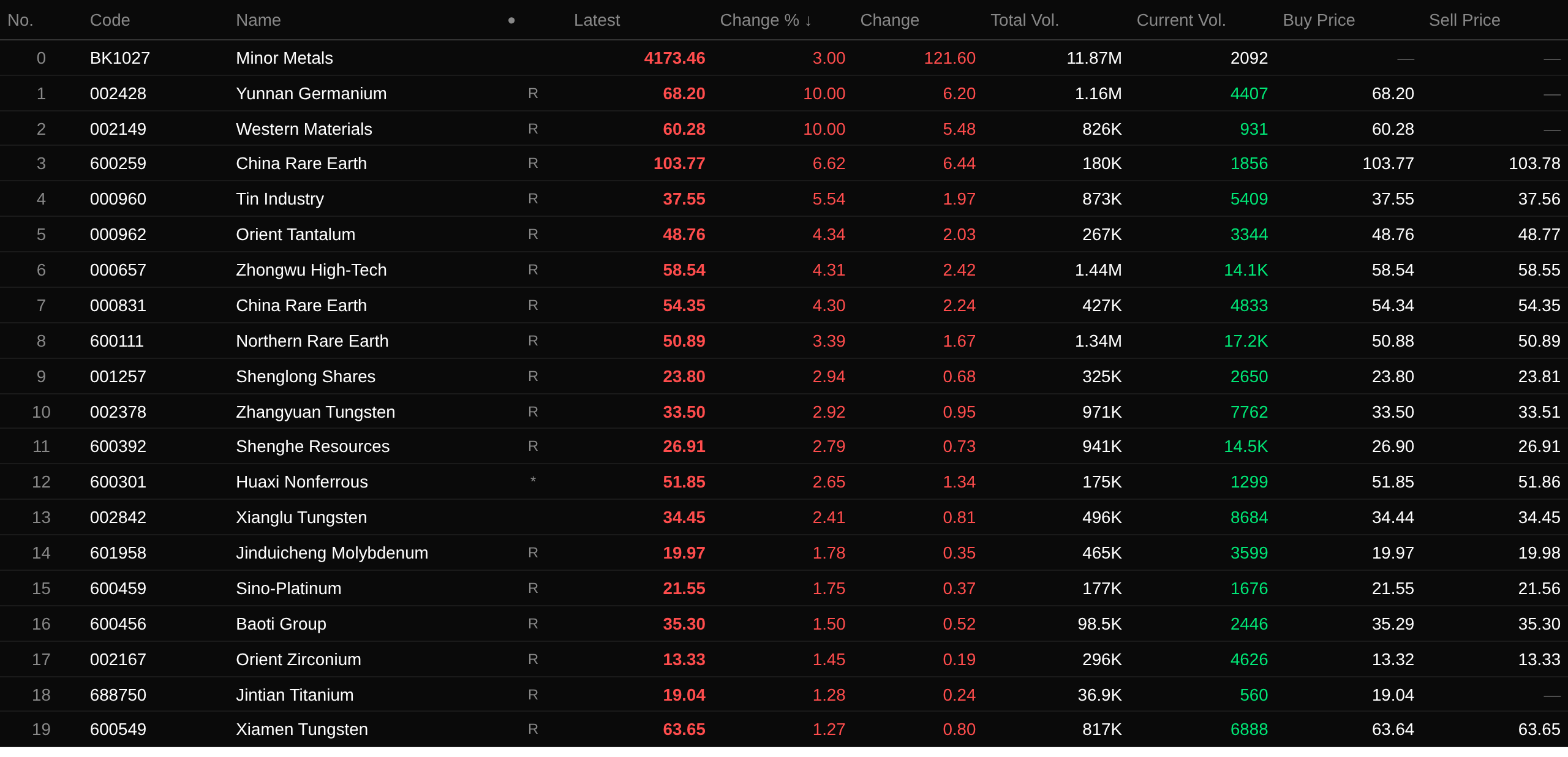

SMM April 20 News:

Affected by tight raw material supply, germanium prices rose over 27% in more than three months. Meanwhile, production halts at some separation plants provided supply-side support for rare earths. Combined with downstream enterprise inventories falling to low levels and downstream restocking demand, rare earth prices continued to rise. The surge in end-use demand from AI computing power, semiconductors, robotics, and other sectors also brought positive demand expectations to the minor metal sector. Coupled with inflows of some market funds, the minor metal sector rose for three consecutive trading days. As of the close on April 20, the minor metal sector gained 3%. In terms of individual stocks: Yunnan Germanium Industry and Western Metal Materials hit the daily limit, while China Rare Colored Metals, Tin Industry Co., Eastern Tantalum Industry, China Tungsten Hightech, China Rare Earth, and China Northern Rare Earth were among the top gainers.

Spot Market

Rare Earths

Spot market side, Pr-Nd oxide prices continued to strengthen over the past two trading days. On April 20, Pr-Nd oxide was quoted at 800,000-805,000 yuan/mt, with an average price of 802,500 yuan/mt, up 0.94% from the previous trading day. Driven by tight supply expectations from production halts at some separation plants, upstream suppliers had a strong mentality to hold prices firm and hold back from selling, while downstream enterprises were currently at low inventory levels. The rebound in rare earth prices brought some restocking demand into the market, further supporting continued rare earth price increases. As the average price of Pr-Nd oxide rose above 800,000 yuan/mt again, wait-and-see sentiment in the market gradually intensified, while downstream magnetic material enterprises had limited acceptance of high-priced metals, and purchasing enthusiasm declined. In the short term, supported by strong upstream confidence in holding prices firm, Pr-Nd product prices are expected to hover at highs.

Germanium

Affected by tight raw material supply, the price center of germanium shifted upward overall. On April 20, SMM germanium ingot was priced at 15,000-19,500 yuan/kg, with an average price of 17,250 yuan/kg, flat from the previous trading day. The average price of 17,250 yuan/kg on the 20th was up 3,750 yuan/kg from the low of 13,500 yuan/kg on January 14, a gain of 27.77% over more than three months.

Institutional Views

According to a Huafu Securities research report, the main drivers behind the sharp rise in rare earth Pr-Nd prices last week included the dual effects of supply-side tightening and demand-side recovery. In terms of supply, the market widely reflected tightening rare earth raw material supply, especially as news of significant production cuts or halts at some enterprises was circulating recently, with quotes continuing to tighten. From January to February 2026, cumulative rare earth exports reached 10,468 mt, up 23% YoY; of which February alone saw exports of 4,407 mt, up 37% YoY. Robust export demand diverted spot cargo resources in China, exacerbating the supply-demand imbalance. In the short term, the market is still expected to fluctuate upward, but caution is warranted against resistance to transactions at high levels. Individual stocks: for antimony, Hunan Gold, Huaxi Nonferrous, and Huayu Mining are recommended; for molybdenum, Jinduicheng Molybdenum, China Gold International, and CMOC; for tungsten, Jiaxin International Resources, China Tungsten High-Tech, Xiamen Tungsten, and Zhangyuan Tungsten; for rare earths, China Rare Earth, China Northern Rare Earth, JL MAG Rare-Earth, and Xiamen Tungsten.

A research report from Guojin Securities noted that the earlier impact of electronic trading platform liquidity was gradually being digested, and prices were stabilizing; combined with expectations of more relaxed exports going forward, we are more optimistic about subsequent demand; the export rush coupled with ongoing supply-side reforms points to a promising resonance in rare earth supply and demand.

A research report from Dongguan Securities stated that, looking ahead, the growth rate of rare earth supply-side quotas in China is expected to slow down. Demand side, humanoid robots, the low-altitude economy, and other sectors are expected to open up a second growth driver for rare earth demand this year, and the supply-demand logic of the rare earth industry is expected to be further optimized. The slowdown in quota growth in China, combined with limited incremental supply outside China, points to continued tightening of overall supply.

Recommended reading:

![Three consecutive rare earth price rises and zirconium price adjustments push minor metals sector higher at open; Oriental Zirconium, China Rare Earth Nonferrous hit limit up [SMM Flash]](https://imgqn.smm.cn/usercenter/YhgvU20251217171725.jpg)