Chinese stainless steel futures staged a decisive breakout this week (April 13–17, 2026), with the most-traded SS2606 contract on the Shanghai Futures Exchange (SHFE) surging past the psychologically important 15,000 yuan/mt (approx. $2,200/mt) mark for the first time since 2023. The rally was driven by the combination of Indonesia's formal rollout of a new nickel ore pricing policy and stronger-than-expected Chinese macro data — a convergence that shifted both the cost floor and market sentiment simultaneously.

The SS2605 contract closed Friday at 15,095 yuan/mt (approx. $2,213/mt), up 625 yuan/mt (approx. $92/mt), or 4.32%, from the previous Friday's close of 14,470 yuan/mt (approx. $2,122/mt). The contract touched an intraday high of 15,175 yuan/mt (approx. $2,225/mt), setting a new multi-year peak. Notably, gains on the futures board significantly outpaced movements in the physical market and upstream raw materials, indicating that the rally was largely fund-driven rather than led by end-user demand.

Macro backdrop: synchronized positives at home and abroad

Chinese first-quarter GDP expanded 5.0% year-on-year, accelerating by 0.5 percentage points from the fourth quarter of 2025 and beating consensus expectations. M2 money supply grew 8.5% year-on-year at the end of March, and new yuan loans reached 8.6 trillion yuan (approx. $1.26 trillion) in the first quarter. While aggregate social financing came in slightly below the prior-year figure, overall liquidity remained supportive of the manufacturing recovery.

Overseas, U.S. PPI for March came in at 4.0% year-on-year, below the 4.6% consensus. The softer U.S. inflation print eased concerns of runaway price pressure and provided a more constructive backdrop for industrial metals, which trade with a meaningful financial component alongside their physical fundamentals.

Physical market: destocking continues, but buyers remain cautious at higher prices

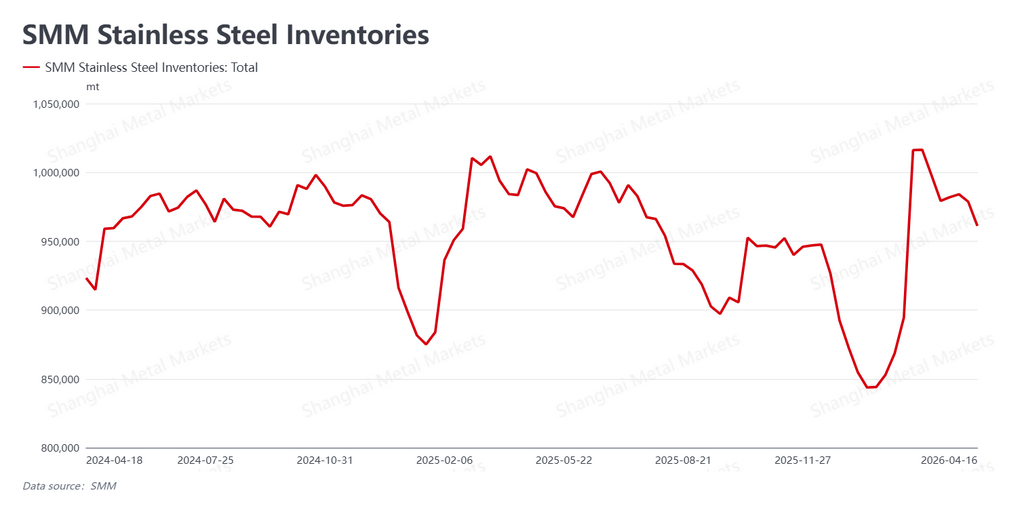

Chinese social inventory of stainless steel fell to 961,100 mt this week from 978,000 mt a week earlier, a drawdown of 16,900 mt. The continued destocking reflects typical April seasonal strength — traditionally a peak consumption window in the Chinese market, sometimes referred to as "silver April." However, much of the buying was attributable to arbitrage players taking advantage of the futures rally rather than organic end-user demand.

Physical traders raised offer prices in line with the futures, but downstream processors and fabricators remained hesitant to chase the move, concerned about near-term volatility. As a result, transaction volumes did not expand materially. Flow was sustained primarily by futures-physical arbitrage activity and the lifting of previously placed orders, suggesting that underlying demand has not yet caught up with the pace of price appreciation.

Cost side: Indonesia's HPM policy locks in the floor

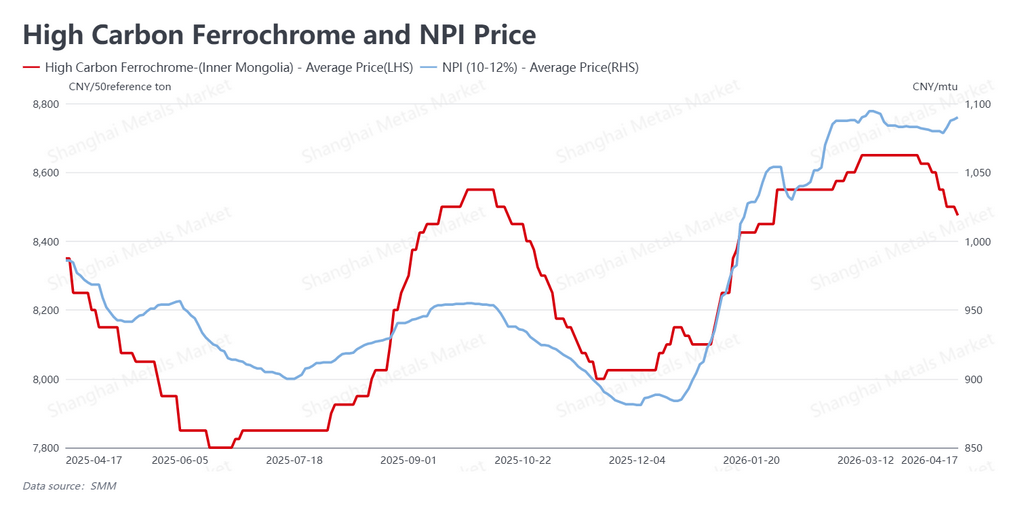

The decisive fundamental catalyst this week was Indonesia's formal publication of the revised coefficient for its HPM (Harga Patokan Mineral) nickel ore benchmark pricing system — the government-set reference price that determines domestic mining royalties and sales prices for nickel ore in Indonesia, the world's largest supplier. The new coefficients close off the downside for raw material costs and have fueled expectations of firmer ore prices going forward.

High-grade Nickel Pig Iron (NPI) rebounded in response, with prices recovering to 1,090 yuan per nickel point (approx. $160 per nickel point) by Friday. By contrast, high-carbon ferrochrome weakened to 8,475 yuan per 50-base mt (approx. $1,243 per 50-base mt). Because the futures rally has significantly outpaced NPI price appreciation, Chinese mill margins have improved meaningfully on a spot basis. However, this has also stretched the premium of futures prices over raw material costs, raising the risk of a pullback from current levels.

Outlook

This week's rally was a textbook fund-driven move. Indonesia's HPM rollout functioned as both a structural cost support and an emotional catalyst, and the combination with the stronger-than-expected Chinese GDP print provided the momentum for a clean breakout. That said, meaningful profit-taking is likely to accumulate above the 15,000 yuan/mt level, and organic downstream demand has not shown the kind of acceleration that would independently validate the move. The SS2605 contract is therefore likely to enter a period of heightened volatility in the coming week as longs and shorts contest the higher range.

![[SMM Nickel Sulphate Daily Review] June 30: Market Transactions Sluggish, Nickel Salt Prices Decline](https://imgqn.smm.cn/usercenter/UruWE20251217171732.jpg)