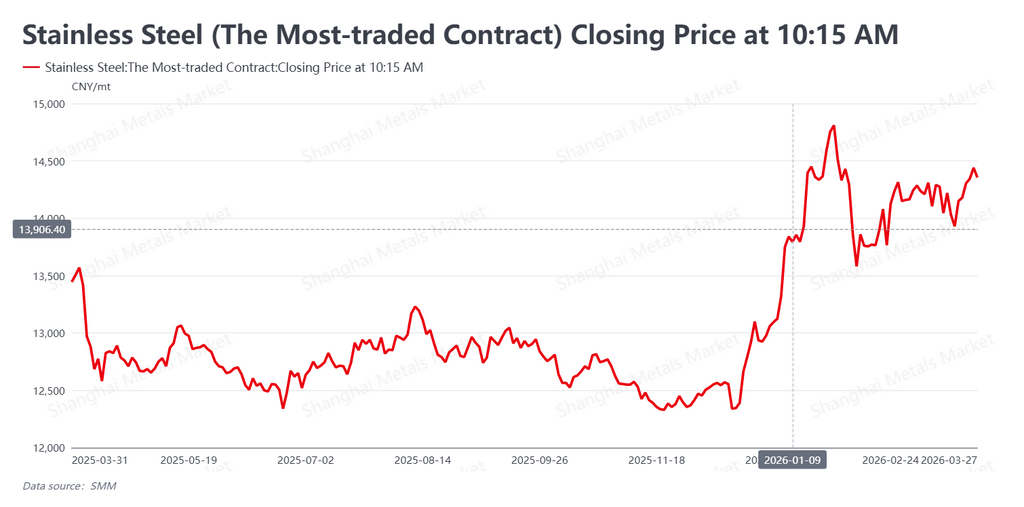

According to SMM data, the week of March 23–27, 2026 marked the final stretch of China’s traditional peak-demand season known as “Golden March.” During the week, the most-active stainless steel futures contract (SS2605) posted a firmer, rangebound rebound as weak fundamentals clashed with renewed macro support. By the close on March 27, the contract had risen to RMB 14,355/mt (about USD 2,076/mt), up RMB 205/mt (about USD 29.65/mt) from RMB 14,150/mt (about USD 2,047/mt) a week earlier.

The week’s defining feature was a sharp contrast between weak spot fundamentals and resilient market expectations. Physical demand remained mediocre, and social inventories moved back into accumulation. Even so, stainless futures found strong support from easing concerns over the Middle East, policy-related uncertainty in Indonesia’s nickel sector, and liquidity support from China’s central bank. As a result, prices managed to hold the lower end of the recent trading range and rebound from there.

Macro backdrop: easing geopolitical stress, but rates remain a headwind

At the macro level, both overseas and China-related developments saw important shifts. In the Middle East, the nearly month-long Strait of Hormuz crisis showed signs of easing after Iran’s mission to the United Nations said that non-hostile vessels could still pass safely through the strait in coordination with Iranian authorities. That helped cool fears of a major energy supply disruption.

However, the inflation fallout from the earlier oil price spike has already shown up in global rates markets. US Treasury yields remained elevated, further reducing room for aggressive Fed easing expectations. In China, the central bank conducted a RMB 500 billion one-year MLF operation, equivalent to about USD 72.32 billion, helping keep liquidity conditions reasonably ample. While this was largely a routine move, it did help ease some of the valuation pressure created by a high global interest-rate environment and offered a degree of support to the market floor.

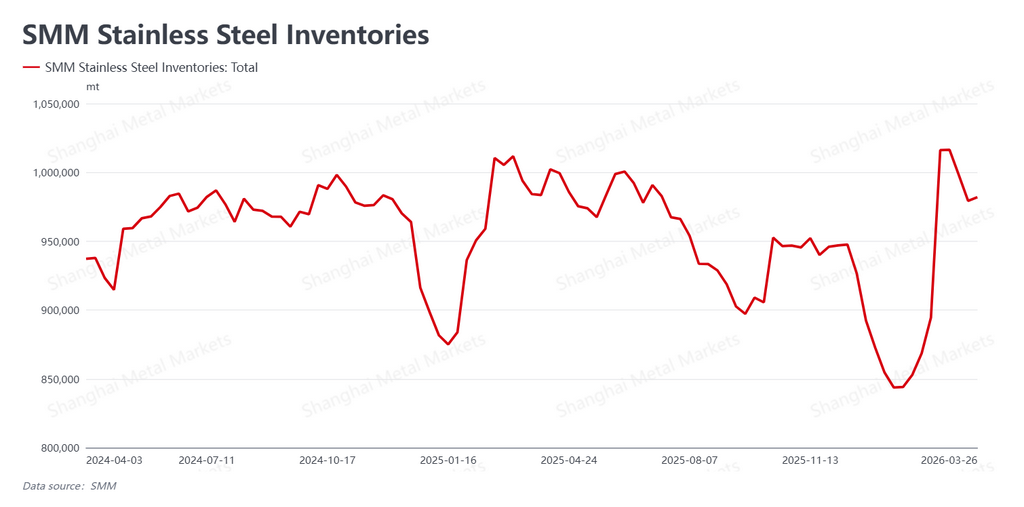

Fundamentals: destocking stalls as inventories edge higher again

On the fundamentals side, the destocking trend came to an abrupt halt, and “Golden March” ended on a disappointing note. The latest SMM data showed that social inventories failed to extend the declines seen over the previous two weeks and instead edged up to 982,000 mt, from 979,300 mt the week before, an increase of 2,700 mt.

That renewed inventory build hit a sensitive spot for the market. In the spot market, downstream buyers continued to replenish only as needed, with very little appetite for stocking up. Throughout March, trading activity never showed the kind of momentum normally associated with a true seasonal demand peak. At the same time, mills have maintained relatively high production schedules, creating a mismatch between concentrated arrivals and lukewarm demand. As a result, inventory digestion is becoming more difficult rather than less, placing a clear cap on further upside in both futures and spot prices.

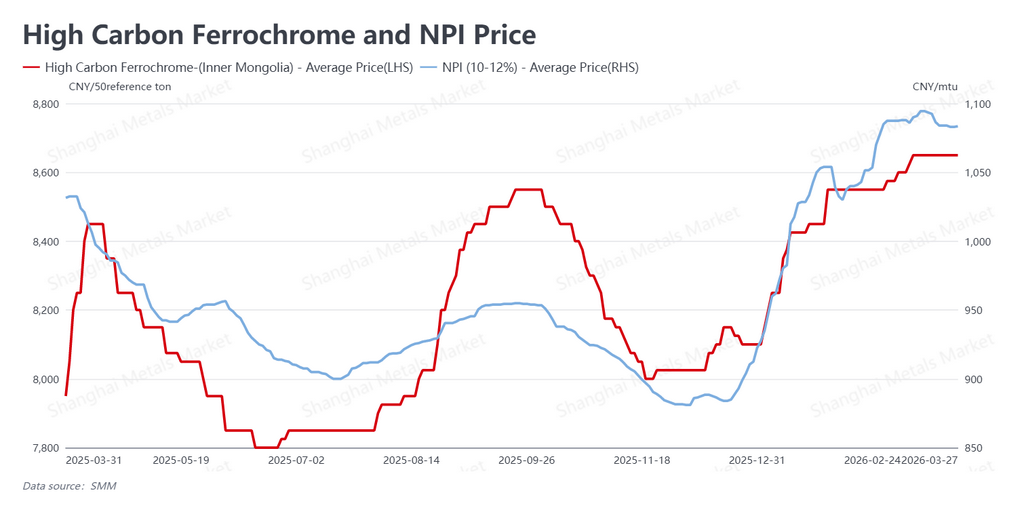

Cost support stays firm as Indonesia policy rumors stir the market

The cost side remained notably resilient, with fresh policy speculation adding another layer of support. As of March 27, high-grade NPI was quoted at RMB 1,083.5 per nickel unit (about USD 156.71 per nickel unit), while high-carbon ferrochrome held firm at RMB 8,650 per 50-basis mt (about USD 1,251.07 per 50-basis mt).

Although weak spot fundamentals still left mills inclined to push back against expensive raw materials, the market was unsettled this week by reports and rumors surrounding possible Indonesian export taxes and windfall taxes on nickel products. That policy uncertainty quickly revived bullish sentiment and helped upstream prices stabilize even as the market faced correction pressure. With raw material costs remaining elevated, downside room in stainless steel futures continued to look limited.

Outlook: macro support sets the floor, weak demand caps the upside

Overall, this week’s market was a clear example of macro support defining the downside floor while weak fundamentals capped the upside. “Golden March” ended without delivering the demand strength many had hoped for, and the return to inventory accumulation undermined the bullish case from a fundamental perspective. Even so, the combined effect of China’s RMB 500 billion MLF injection, easing Middle East tensions, and Indonesian tax-related speculation helped prevent a breakdown and instead allowed prices to rebound.

Looking ahead, the market is now moving into the “Silver April” period. With inventories still high and mill output still elevated, there is little in the current fundamentals to support a strong one-way rally. At the same time, cost support remains firm enough to make a deep decline difficult. In the near term, the most-active stainless steel futures contract is expected to remain in a broad trading range. Market participants should pay close attention to whether Indonesian policy measures are formally implemented and how quickly spot inventories are absorbed after the holiday period. For now, chasing prices higher aggressively still looks risky.

Written by: Bruce Chew | bruce.chew@smm.cn +601167087088

![[SMM Nickel Market Flash] Indonesia Nickel Industry Seeks Clarity on Whether NPI Falls Under Mandatory DSI Export Rule](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)

![[SMM Nickel Market Flash] Harita Nickel Reports Q1 2026 Revenue of Rp6.81T (~$418M), Full-Year 2025 at Rp29.63T](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Nickel Market Flash] First Atlantic Gets Newfoundland Permit to Advance Awaruite Ni-Co Project and Geologic H2 Test](https://imgqn.smm.cn/usercenter/sKmGT20251217171733.jpg)