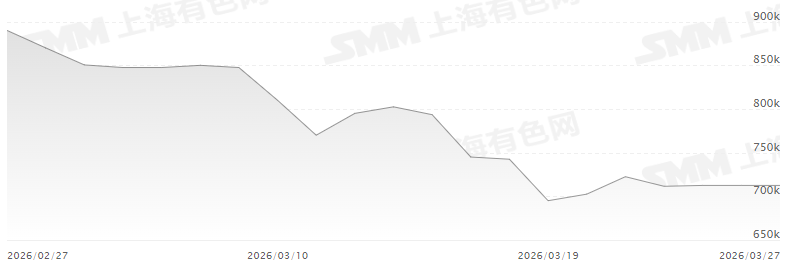

This week, the domestic praseodymium-neodymium oxide market experienced narrow fluctuations, with prices remaining relatively stable overall while market sentiment saw minor shifts. Early in the week, firm pricing intentions from upstream separation plants and just-in-time procurement from large enterprises helped improve trading sentiment temporarily, prompting sellers to test higher offers and pushing prices slightly upward. However, persistent weakness in end-user demand and limited new orders from downstream magnetic material companies led to a generally pessimistic outlook on near-term consumption. As a result, downstream metal producers showed little enthusiasm for procurement, with price acceptance clearly constrained. When offers exceeded 720,000 RMB/ton, buying interest dropped significantly, and actual transactions faced resistance. Without sufficient momentum, prices eventually retreated to around 710,000 RMB/ton, forming a pattern of initial gains followed by a pullback.

From a supply-demand perspective, some upstream separation plants are currently undergoing temporary suspensions or production cuts due to environmental inspections or maintenance, leading to a certain degree of supply contraction that provides underlying support for prices. Meanwhile, downstream demand remains weak, with no notable improvement in end-user consumption, leaving the market without strong positive catalysts. Overall, the market is characterized by weakness on both the supply and demand sides, with intense game-playing between upstream and downstream participants. Sellers show limited willingness to concede on prices, while buyers maintain a cautious wait-and-see approach, with actual transactions primarily driven by essential needs. In the short term, the praseodymium-neodymium oxide market is expected to continue in this stalemate, with ongoing tussling between the two sides and prices likely to move within a narrow range, with limited room for significant upward or downward movement.

![Energy Fuels' Acquisition of VAC and US International Mature Rare Earth Asset Acquisition Landscape [SMM Analysis]](https://imgqn.smm.cn/usercenter/ecUwF20251217171745.jpg)

![This week, rare earth prices outside China remained stable, while the US continued to acquire mature rare earth enterprises outside China [SMM Rare Earth Ex-China Weekly Review].](https://imgqn.smm.cn/usercenter/OJvHl20251217171744.jpeg)