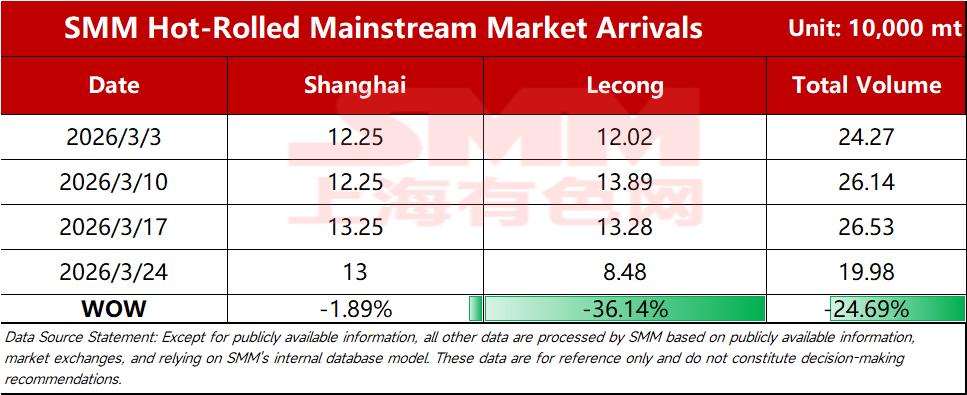

SMM Steel March 24: According to SMM statistics, the estimated total shipments to mainstream markets this week reached 214,800 mt, down 19.04% WoW. Breakdown by market:

Chart-1: Mainstream Market Arrivals Comparison

Data source: SMM Steel

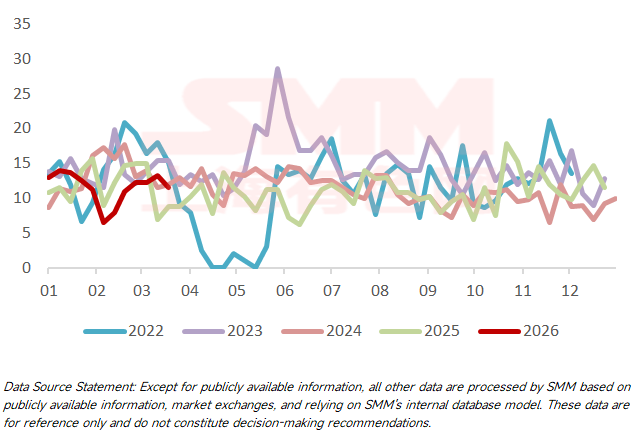

Shanghai market: Hot-rolled coil shipments to Shanghai declined slightly this week. Specifically, shipments from mainstream steel mills in South China decreased modestly, while those from other regions remained basically flat. Short-term, east China's price advantage remained limited, prompting steel mills to maintain stable shipment volumes. Next week's shipments to Shanghai are expected to fluctuate rangebound.

Chart-1: Shanghai Market Arrivals

Data source: SMM Steel

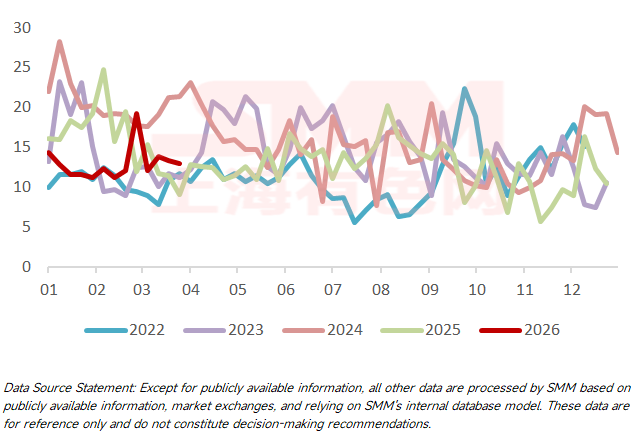

Lecong market: Shipments to Lecong dropped notably WoW. The decline was primarily driven by reduced shipments of local mainstream resources, as WG shifted production to specialty steels mid-month, leading to a significant WoW decrease in shipments. Looking ahead, in-transit mainstream resources remain scarce, suggesting arrivals in Lecong may stay low next week, creating opportunities for local inventory drawdown.

Chart-2: Lecong Market Arrivals

Data source: SMM Steel

SMM releases weekly hot-rolled shipment data for mainstream markets every Tuesday. Scan the QR code below to subscribe or access more data.

![[SMM Steel] Indonesian Billet Edges Down as Chinese Offers Weigh](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)

![[SMM Steel] Alang Scrap Stable, Mandi Market Rises](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)