Recently, the sharp deterioration of the geopolitical situation in the Middle East has profoundly disrupted global commodity trade flows, driving a dramatic structural shift in the region's internal steel supply and demand. On one hand, Iran, a core steel-producing nation, is choked by the "dual stranglehold" of domestic energy shortages and blockaded logistics channels, directly resulting in a steel billet supply vacuum of over 2.3 million tons in the Southeast Asian market. On the other hand, the Red Sea shipping crisis has severely throttled China's steel export arteries. China's flat and tubular steel products, which previously maintained robust outward flows to Gulf nations based on bilateral trade advantages, are now facing severe shipping gridlocks.

Data indicates that amidst this dual mismatch of "supply breakpoints" and "export blockades" triggered by geopolitical risks, China and India are leveraging their capacity and product advantages to rapidly absorb the diverted billet orders originally belonging to Iran. The Asian steel trade map is reshaping at an unprecedented pace amid these growing pains.

The Persian Gulf Halt: From "Peak Output" to Severed Arteries

The complex geopolitical landscape in the Middle East is transmitting shockwaves across global commodity markets. As a crucial global hub for steel production and consumption, the internal supply-demand balance in the Middle East is being fundamentally shattered by the escalation of the US-Iran conflict. Iran is plunging into a profound "supply-demand mismatch," with its traditional export arteries severely blocked. Constrained by chronic energy bottlenecks—gas shortages in winter and power rationing in summer—coupled with relatively sluggish apparent domestic demand, Iran's massive semi-finished steel capacity heavily relies on seaborne exports.

Looking back before the conflict escalated, data released by the Iranian Steel Producers Association (ISPA) confirmed that 2025 was undoubtedly the "peak moment" for Iranian steel exports. Its export structure demonstrated aggressive market penetration, establishing absolute dominance particularly in the semi-finished sector: From March to December 2025, Iran's billet exports reached 4.58 million tons (+37.7% YoY), and slab exports hit 1.54 million tons (+44.6% YoY).

However, as the conflict intensified, this smooth "outward artery" for semi-finished products was severely choked. Massive volumes of steel billets, originally destined for overseas markets, were forced to pile up at ports. Essentially, Iran transformed overnight from a super-exporter of semi-finished goods to a massive "breakpoint" in the global steel supply chain.

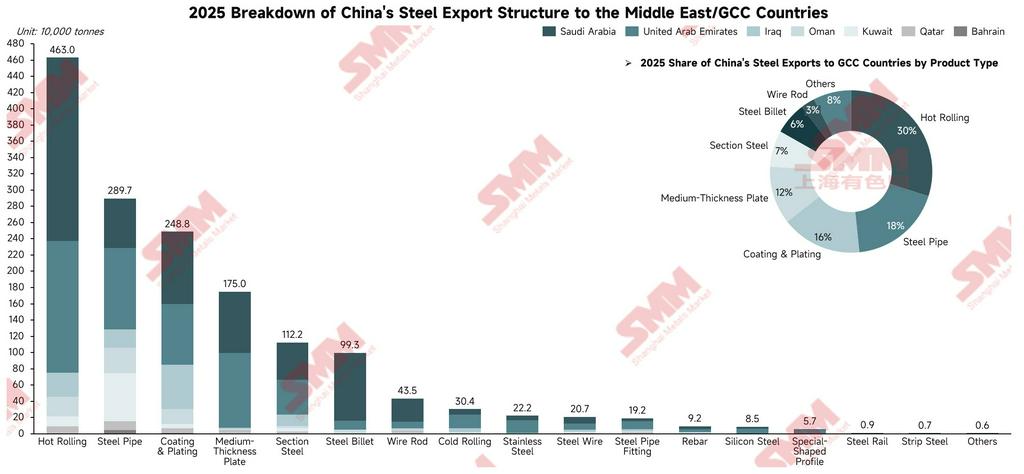

Structural Output: China Maintains Dominance in Three Core Categories to the Middle East

Beyond Iran's logistical mismatch, the broader Middle East region exhibits highly structural characteristics in product supply and demand. Observing the categories of China's steel exports to the Middle East provides the most direct insight into the region's true demand profile.

As the data shows, China's steel shipments to core Middle Eastern countries (such as the UAE, Saudi Arabia, and Iraq) in 2025 displayed high product concentration, with steel pipes, hot-rolled coils (HRC), and coated products maintaining absolute dominance. Notably, Saudi Arabia also demonstrated a massive appetite for steel billets, accounting for approximately 84% of the total billet imports to Gulf countries from China.

The underlying logic for the sustained high import volumes across the Middle East lies not only in local infrastructure booms but also in favorable bilateral trade environments. Taking Saudi Arabia and the UAE as examples, the significant growth in their imports of Chinese steel is fundamentally driven by tightening economic cooperation, favorable currency settlement conditions, and an increasingly optimized business environment for Chinese enterprises.

On the domestic capacity front, while Middle Eastern nations aggressively develop Direct Reduced Iron (DRI) and Electric Arc Furnace (EAF) technologies to achieve self-sufficiency in long products (in practical smelting, charging hot metal into EAFs is a rational, economically driven operational choice, often utilized more by integrated steelmakers than standalone EAF mills), these optimized processes still cannot bridge the capacity gap in flat products and premium tubular goods. Thus, the region remains highly dependent on the "hardcore" supply from mature supply chains like China.

The Great Mismatch: China's Flat Steel Hits an Export Winter in the ME, Yet Billet Orders Show Resilience

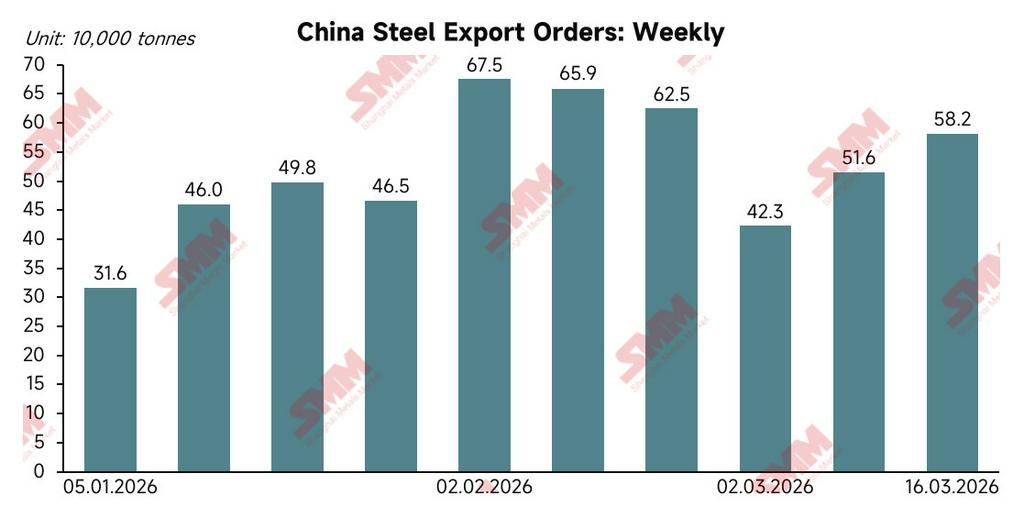

The sudden shift in the Red Sea has ruptured this established bilateral trade consensus. We must re-evaluate the comprehensive impact of the geopolitical crisis on China's steel exports. This is not a simple "ebb and flow" scenario, but a profound industrial mismatch. On one hand, China's flat and pipe orders destined for the Gulf face an "export winter," stalling almost completely due to transportation blockades. On the other hand, China's overall export orders have demonstrated astonishing resilience.

SMM's Chinese export order data directly corroborates this trend. As illustrated, after early-year fluctuations, China's weekly steel export orders in Q1 2026 have shown a significant upward trajectory. Crucially, "diverted risk-off orders" from buyers dodging the Iranian supply halt contributed essential growth.

Fundamentally, China is utilizing its colossal capacity base and mature export supply chain to effortlessly "absorb" the urgent overseas demand for semi-finished products triggered by the Iran halt. In 2025, China exported roughly 35 million tons of steel to Southeast Asia, with the top three categories—coated steel, HRC, and billets—totaling 19 million tons, providing the structural backbone for China to swiftly fill the gap.

However, we must confront the structural truth behind the data. A generalized view obscures the reality that China has simultaneously lost substantial flat and pipe orders from Gulf states due to the Red Sea turmoil.

Additionally, India's "precision filling" warrants attention. In 2025, India exported about 460,000 tons to Southeast Asia. While the absolute volume is modest, the product mix is highly concentrated in billets (~200,000 tons) and HRC (~110,000 tons). This structure perfectly overlaps with Iran's disrupted supplies. Leveraging its geographical proximity, India is actively seizing this short-term, high-premium market deficit.

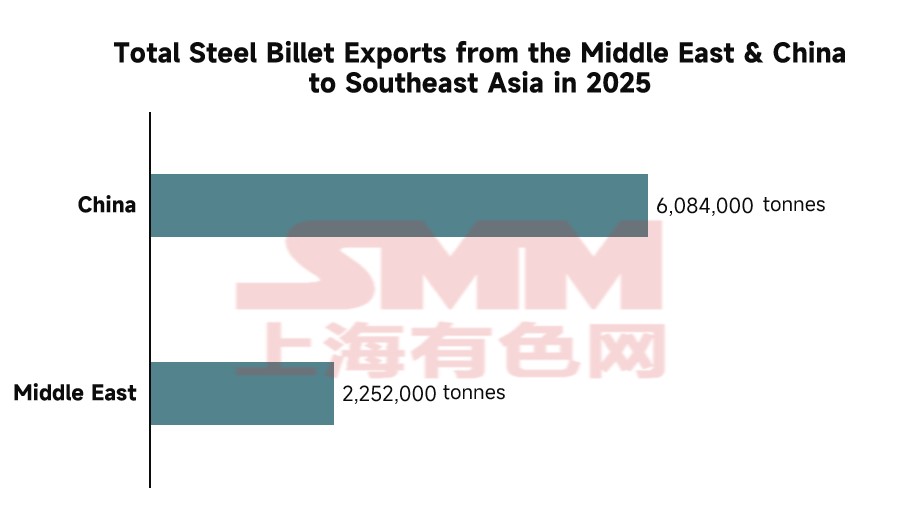

The Southeast Asian Vacuum: The Reality Behind the 2.3 Million-Ton Supply Breakpoint

The core driver behind the counter-cyclical surge in recent orders for China and India is the chain reaction sparked by the Middle East (Iran) supply halt, which is manifesting most violently in the Southeast Asian market.

Currently, multiple ASEAN nations are in a phase of rapid development, with relatively low per-capita steel consumption and vast room for growth. These emerging economies possess a massive appetite for basic construction materials and semi-finished raw materials.

SMM research data lays bare this heavy reliance: In 2025, Southeast Asia imported approximately 2.31 million tons of steel from the Middle East, with a staggering 97% consisting of semi-finished steel billets. The Middle East effectively served as the long-term raw material "bank" for numerous rolling mills across Southeast Asia. Consequently, when transit through the Strait of Hormuz was restricted, the Southeast Asian market instantly exposed a hard deficit of over 2 million tons. To avert a "raw material drought" and sustain production lines, buyers were forced to pivot massive volumes of emergency orders toward China and India.

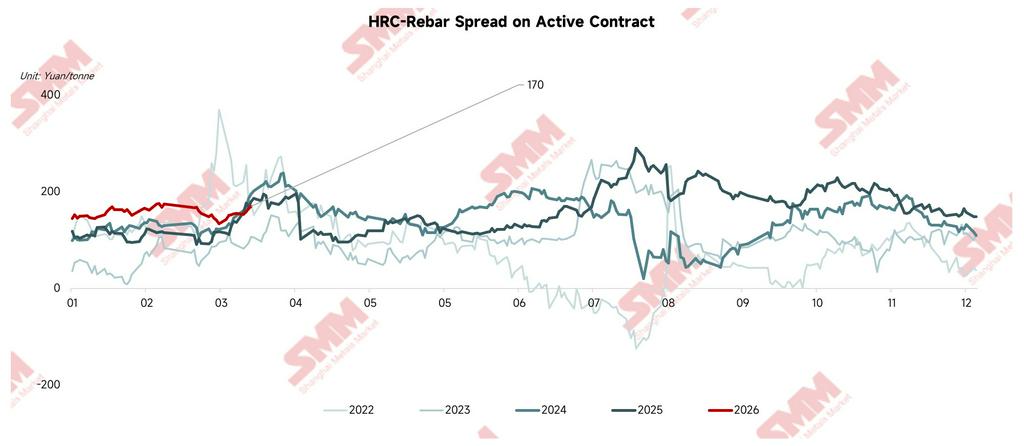

Market Outlook: Mismatch to Drive Narrowing HRC-Rebar Spreads

Looking ahead, driven by long-term "de-risking" strategies within their supply chains, countries traditionally reliant on Iranian exports (like those in Southeast Asia) will substantively shift their procurement focus toward China and India. This long-term reshaping of trade flows is more than a temporary logistical bottleneck; it will generate profound implications for China's domestic steel market.

As China's export structure increasingly exhibits a "billet stronger than HRC" dynamic, the mismatch induced by geopolitical crises will inevitably transmit to the domestic spot pricing system. The blockade on Chinese flat steel exports will force flat-rolled supply pressure back into the domestic market, whereas robust Southeast Asian demand for billets will accelerate the consumption of upstream resources.

Based on these dynamics, SMM makes a bold projection: This export torrent, triggered by the great mismatch, will likely accelerate the narrowing of the domestic HRC-rebar spread through market labor pains. The reshaping of the global steel trade map is, in an entirely unexpected manner, kicking off a new industry cycle.

![In the short term, ferrous metals will remain under pressure [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/YxksS20251217171748.jpg)

![Silicon Metal Futures Fluctuate within a Narrow Range, Spot Market Largely Stable [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/bkAyC20251217171720.jpg)