Overseas Tungsten Raw Material Market Tightens at a Faster Pace, Prices Continue to Surge Under a Seller-Dominated Pattern

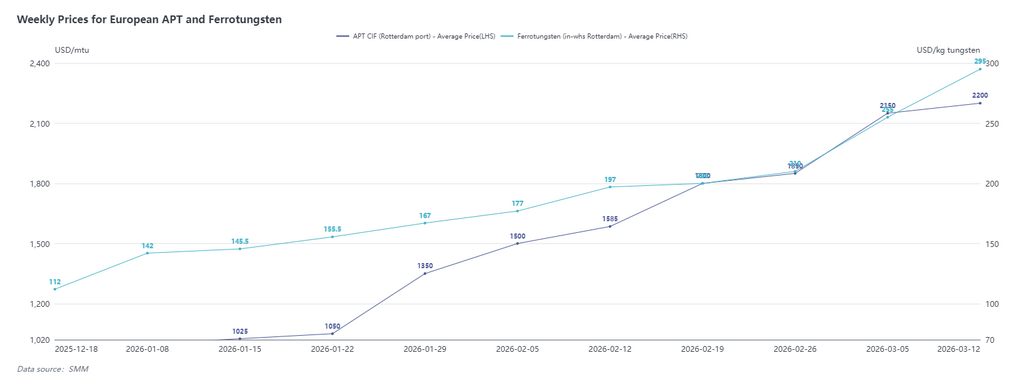

As of March 13, SMM data showed that the price of ammonium paratungstate (APT) CIF Rotterdam was $2,150-2,250/mtu, with an average price of $2,200/mtu, up $50 from March 6; ferrotungsten (Rotterdam warehouse) was priced at $280-310/kg tungsten, with an average of $295/kg tungsten, up $40 from March 6.

In addition, the latest SMM survey on March 16 showed that Indian FOB quotes for scrap tungsten alloy inserts had reached $142-158/kg, while European quotes for scrap tungsten alloy inserts rose to 130-140 euros/kg. Prices in both markets were up more than 25% WoW, and the overseas scrap tungsten market maintained a sustained upward trend.

At present, the raw material inventory gap in the European and US markets is extremely significant. According to the SMM survey, raw material inventories at most producers were nearly depleted, and procurement demand was urgent. Against this backdrop, end-user buyers remained increasingly active in making inquiries, and nearly every transaction pushed APT quotes further upward. Last week, some extreme transaction prices in the market reached $2,700-3,000/mtu. Although the trading volume was extremely limited and not enough to represent the overall market average price, it reflected that prices still had momentum for continued increases amid the intensifying supply-demand imbalance. The tungsten raw material market has now clearly shifted to a seller-dominated pattern, with suppliers' bargaining power significantly strengthened.

Supply side, the scrap market in India continued to face dual pressure. On the one hand, scrap prices kept soaring, compounded by a shrinking volume of circulating scrap resources, making procurement increasingly difficult; on the other hand, natural gas prices continued to rise, pushing up production costs.

According to feedback from a sodium tungstate producer, its production raw materials mainly consisted of hard alloy scrap and catalyst scrap, and both types of raw materials were currently difficult to obtain in the Indian market. Meanwhile, the roasting process was highly dependent on energy, and the enterprise was under substantial cost pressure and had fallen into production stagnation. It is worth noting that sodium tungstate is an important raw material source for APT production in India and Vietnam. Recently, supply in this segment was nearly cut off, further exacerbating tight raw material supply in the region.

According to an SMM survey, Vietnam Masan's APT resources are currently also sold out. The enterprise is in the process of shifting its mining area from the old mine to the new mine, with overall output extremely limited, making it difficult to form effective supply in the short term.

From the perspective of exports from China, exports of tungsten raw materials such as APT still face multiple constraints in procedures and transportation. At present, the overall lead time from application approval to cargo arrival at the Port of Rotterdam still requires 3-4 months. Coupled with the impact of geopolitical conflicts, the stability of European shipping routes has declined, further exacerbating uncertainty in the supply chain. As demand from end-user orders outside China remains urgent, the APT CIF Rotterdam transaction price has continued to hit new highs.

China Tungsten Market Pulled Back From High Levels, Rational Wait-and-See Prevails; Tight Supply and Demand Outside China May Further Widen the Domestic-Overseas Price Spread

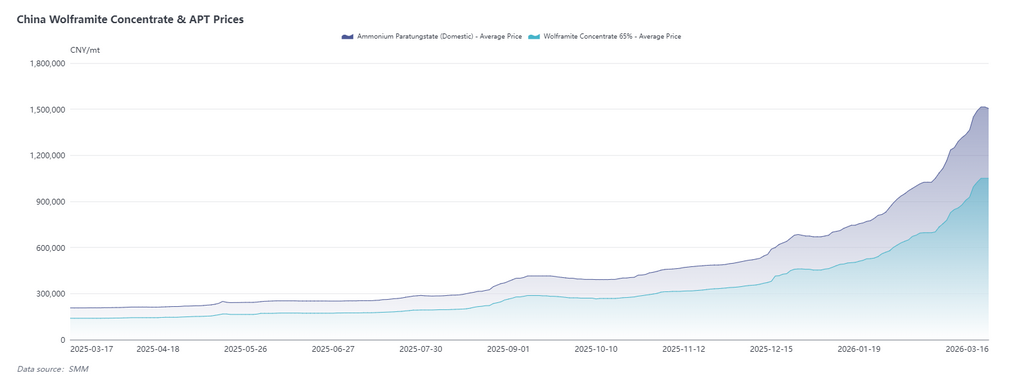

As of March 16, domestic APT was quoted at 1.5 million-1.51 million yuan/mt, with an average price of 1.505 million yuan/mt, down 10,000 yuan/mt from the previous working day; domestic scrap tungsten alloy inserts were quoted at 1,130-1,180 yuan/kg, down 35 yuan/kg from the previous working day.

This week, prices on both the raw material side and the scrap tungsten side in the Chinese tungsten market saw a slight correction, mainly because fear of high prices was gradually released. Since the start of 2026, APT prices had risen by more than 100% cumulatively, and market enthusiasm was somewhat overdrawn. Recently, some mines saw failed auctions, further cooling overheated sentiment, while localized selling put prices under pressure to consolidate around the 1.5 million yuan/mt mark.

The scrap tungsten market was likewise dominated by fear of high prices. Earlier price gains had come too fast, downstream demand moved toward saturation, support at high levels weakened, and the market gradually entered a correction channel. Overall, the tungsten market was undergoing a phase of sentiment repair and price rebalancing.

China market, the current price adjustment was an inevitable result of the release of earlier overheated sentiment, and the market was gradually shifting from irrational rush to buy amid continuous price rise to a phase of rational wait-and-see. However, it should be noted that the fundamental supply crunch situation in the tungsten market had not changed fundamentally, nor had the policy side released any new regulatory signals, leaving the market as a whole in a high-level consolidation pattern. In the short term, price trends will still be affected by multiple macro uncertainties.

By contrast, the tight supply-demand pattern in markets outside China had not seen any substantive easing. Affected by factors such as elevated energy costs and persistent transportation pressure, the overseas raw material supply side was even tighter. Against this backdrop, the current APT CIF Rotterdam port price of $2,200/mtu may only be a new starting point. In the future, as the Chinese market enters a phase of high-level adjustment, overseas market prices are expected to continue rising, and the price spread between domestic and overseas markets may widen further.