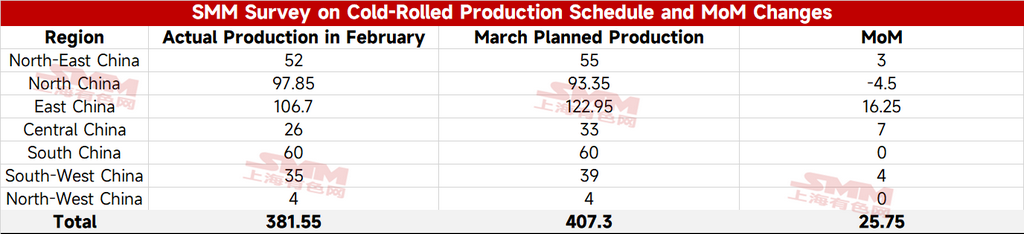

- SMM Cold-Rolled Production Schedule: Steel Mills’ Daily Average Cold-Rolled Production Schedule Fell 3.6% in March

According to SMM’s latest tracking, the total planned volume of cold-rolled commercial products for this month among 31 mainstream cold-rolled sheet and coil steel mills was 4.073 million mt, up 257,500 mt (6.7%) from last month’s actual production of cold-rolled commercial products.

On a daily average basis, March had three more days than February. The daily average scheduled production of cold-rolled commercial products in March was 131,400 mt, down 3.6% MoM from last month’s actual daily average production of cold-rolled commercial products.

Table 1: MoM Changes in SMM Steel Mills’ Planned Output of Cold-Rolled Commercial Steel Products

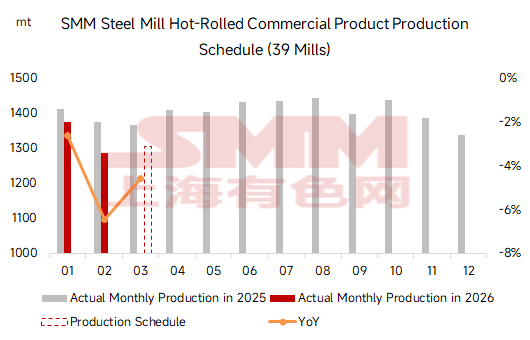

- SMM HRC Production Schedule: March HRC Production Schedule Rose 1% MoM, Daily Average Fell 8%

According to SMM’s latest tracking, the total planned HRC commercial output for 39 mainstream HRC steel mills this month was 13.04 million mt, up 181,800 mt, or 1.4%, from last month’s actual HRC commercial production.

On a daily average basis, March had three more days than February. The daily average scheduled HRC commercial output in March was 420,700 mt, down 8.4% MoM from last month’s actual daily average production.

In March, multiple steel mills in Northeast China, North China, east China, and Central China released maintenance plans, compounded by voluntary production cuts and reduced operating rates at some steel mills in North China during the Two Sessions; in addition, SMM learned that a small number of steel mills adjusted production to cold-rolled products. Under the combined impact, total steel mill production schedules this month fluctuated rangebound compared with February, while the daily average production schedule saw a notable decline from February.

Summary: Total hot-rolled commercial steel production scheduled by steel mills in March rose MoM, but because March had three more days than February, the daily average production schedule fell sharply MoM.

Demand side, according to SMM data, apparent demand for hot-rolled coil in the second week after the holiday was at a relatively low level for the same period over the past four years, only about 1.2% higher than the same period in 2025, and demand in the “Golden March, Silver April” period faced significant challenges; meanwhile, the Middle East conflict disrupted China’s steel export orders to the Middle East, triggering market concerns that weaker exports could lead to production flowing back into the domestic market and further increase the difficulty of inventory drawdown.

Macro perspective, recently bullish and bearish factors at home and abroad were intertwined: overseas geopolitical conflicts continued to escalate, while during the domestic Two Sessions, policy “tailwinds” kept emerging, intensifying disruptions to capital flows and market sentiment.

Overall, uncertainty from macro perspective news was relatively high. Fundamentally, attention should be paid to domestic and overseas hot-rolled coil demand performance and inventory drawdown in mid-to-late March. If demand remains weaker than the same period in recent years, hot-rolled coil prices in March may face room to pull back under pressure.

![Strong Cost Support Remained; Ferrous Metals May Hold Up Well in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/gaBsW20251217171749.jpg)

![[SMM Daily HRC Trading Volume] Futures Hovered at Highs, Spot Trading Changed Relatively Little](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)