First, a review of the February price trend for secondary aluminum alloy: Futures market: In February, the most-traded cast aluminum alloy contract generally showed a pattern of falling first and then stabilizing, followed by a post-holiday rebound. Early in the month, it extended the pullback trend seen in late January, with futures prices largely giving back earlier gains and fluctuations widening markedly; later, as Chinese New Year approached, trading turned sluggish and prices were mainly rangebound and consolidative. After the holiday, futures prices rebounded quickly. Entering March, amid disruptions from external factors such as the escalation of the US-Iran conflict, bullish sentiment heated up again and prices strengthened noticeably.

Spot market: In early February, dragged down by a sharp plunge in futures, spot quotes pulled back quickly and then stopped falling and stabilized; after the holiday, alongside a rebound in primary aluminum and the progress of production resumption, prices recovered somewhat. Price spread: In February, the center of aluminum prices moved lower, while supported by costs and affected by supply contraction, ADC12 prices were relatively resilient, maintaining a premium against A00 prices; in March, as primary aluminum rose sharply again, the premium narrowed significantly. As of March 6, SMM ADC12 was assessed at 24,600 yuan/mt, up a cumulative 750 yuan/mt from early February.

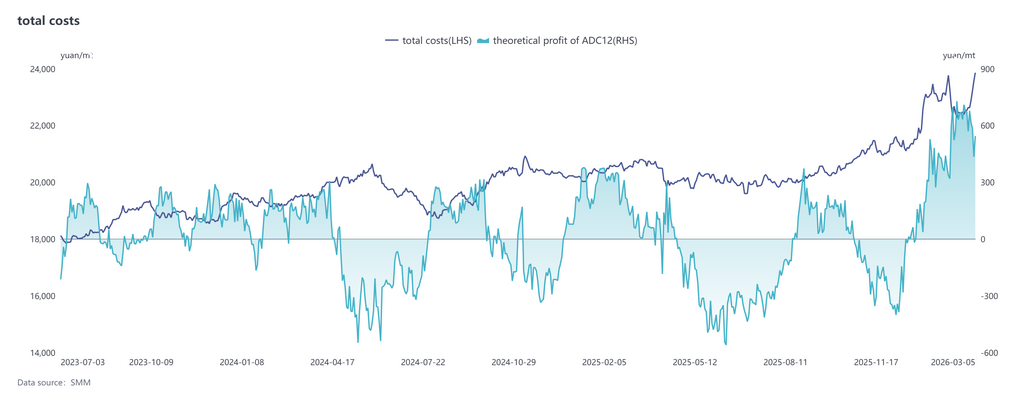

Cost side, according to the latest SMM data, the theoretical total cost of the ADC12 industry in February fell to 22,492 yuan/mt, down 2.6 percentage points MoM from January. From the cost structure perspective, aluminum scrap cost per mt pulled back to 20,245 yuan, with its share narrowing slightly to 90.0%, remaining the primary cost source; copper cost per mt was basically stable at 850 yuan, with its share edging up to 3.8%; silicon cost per mt inched up to 491 yuan, with its share rebounding to 2.2%. Overall, changes in the cost structure were relatively small, and aluminum scrap still held an absolute dominant position in the cost system. Over the same period, the industry’s theoretical ADC12 profit was about 643 yuan/mt, still in profitable territory overall. Entering March, against the backdrop of continued gains in primary aluminum prices and a gradual release of raw material procurement demand driven by enterprises resuming operations, aluminum scrap prices are expected to hold up well, and the short-term cost center is likely to move further higher, becoming the core driver supporting stronger secondary aluminum prices.

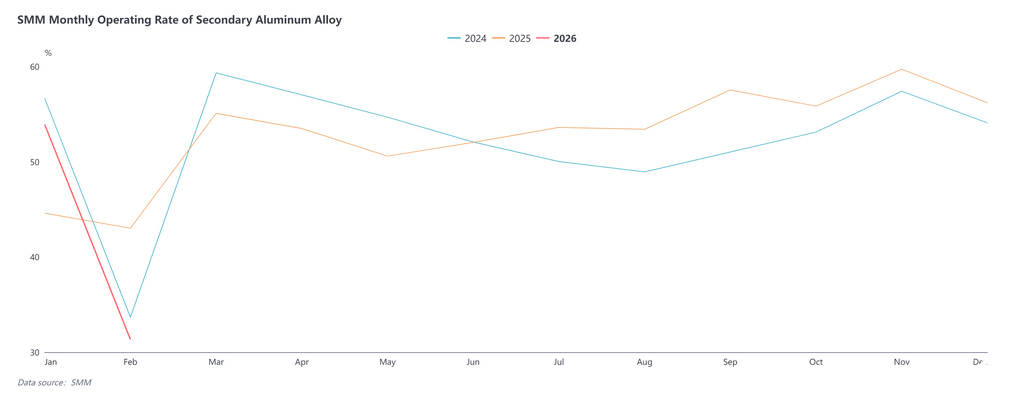

In terms of supply, the operating rate of the secondary aluminum alloy industry came in at 31.3% in February, down sharply by 22.6 percentage points MoM and down by 11.7 percentage points YoY. Affected by the concentrated production shutdowns during the Chinese New Year, enterprises saw a marked reduction in effective production days, with production declines of 30%–50% for most enterprises, leading to a significant contraction on the supply side of the industry. In addition, environmental protection-related controls tightened in some regions ahead of the holiday, and with detailed fiscal and tax policy rules such as “reverse invoicing” yet to be clarified, enterprises became more cautious in production; some took holidays early or delayed resuming operations, and a few even approached a near full-month shutdown.

Demand also remained weak. Beyond seasonal holiday factors, multiple factors—including pre-holiday destocking by manufacturers, adjustments to the purchase tax policy for new energy vehicles, and end-use consumers waiting to see discounts at spring auto shows—dampened auto production and sales in February, putting secondary aluminum producers’ orders clearly under pressure. Entering March, as the industry chain fully resumed operations and automakers’ production schedules gradually recovered, supply and demand are expected to recover in tandem, with the industry operating rate likely to rebound week by week and move back toward normal pre-holiday levels. However, the pace of recovery will still depend on the actual realization of end-user orders.

The English translation of the above text is:

Overall, ADC12 prices in March are expected to fluctuate while holding up well. On the macro front, escalating tensions in the Middle East have heightened market concerns over the stability of aluminum supply, driving aluminum prices at home and abroad to fluctuate upward. Against the backdrop of primary aluminum prices remaining at highs and aluminum scrap circulation staying persistently tight, secondary aluminum production costs are unlikely to ease downward, reinforcing producers’ willingness to hold prices firm and making prices more likely to rise than fall. In the short term, cost support and a mild release of supply will jointly underpin ADC12 prices, and the market is expected to continue to hold up well. The medium-term trend will depend more on the actual recovery in end-use consumption. If orders in the die-casting sector increase significantly, the price center is expected to continue to move higher; if demand recovery falls short of expectations, together with a continued rise in the operating rate on the supply side, prices will enter a pattern of fluctuating at highs. Overall, the operating center of ADC12 prices in March is expected to move higher gradually, with the upside extent and pace mainly influenced by the strength of downstream consumption release and raw material supply conditions.

![Domestic and International Aluminum Prices Weakened in Tandem, Weak Macro Dragged Down Pre-Holiday Market [SMM Aluminum Price Weekly Review]](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)

![Downstream Basically Completed Early Stockpiling, Market Transactions Returned to Sluggish [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/JnyfJ20251217171654.jpg)