[SMM Analysis] Persian Gulf Shutdown? The Impact of the U.S.-Iran Conflict on Global Steel Trade

- On February 28, 2026, the conflict between the United States and Iran escalated into a full-scale outbreak, causing a sudden spike in Middle Eastern geopolitical tensions. As a global chokepoint for energy and bulk commodity maritime transport, the Strait of Hormuz has seen shipping disrupted and routes tightened, directly impacting the nerves of the global supply chain. This "Golden Waterway" is not only a lifeline for oil but also a critical strategic corridor for the global steel import and export trade. Once passage is restricted, it will deliver a comprehensive shock to the international steel trade landscape. Amidst the turmoil of war, what disruptions and restructuring will the global steel trade face? SMM's latest research provides an in-depth analysis.

In the short term, the U.S.-Iran conflict poses a risk of stalling steel imports and exports in the Persian Gulf region, putting pressure on China's steel exports.

-

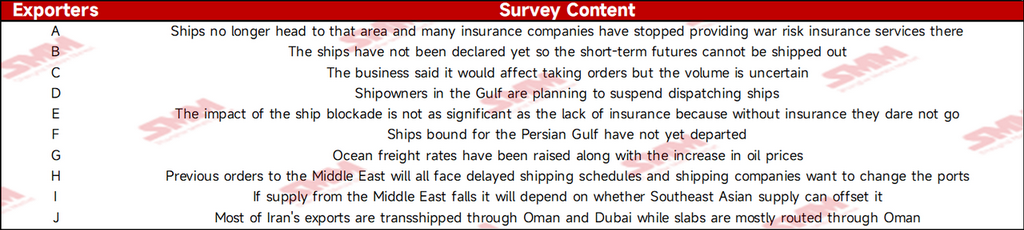

Multiple disruptions along Gulf shipping routes have caused significant delays in exporters' orders.

According to SMM research, the current Middle East situation has disrupted multiple ports in the Gulf region. Bahrain has suspended port activities, including pilotage services. Jebel Ali Port has halted all operations due to a fire caused by intercepting airstrike debris. Qatar's Ras Laffan and Messaid ports remain operational but with reduced traffic, GPS signal interference, and the government closure of its airspace. Similarly, new orders and shipments for Chinese exporters have also been significantly hindered.

Data Source:SMM

-

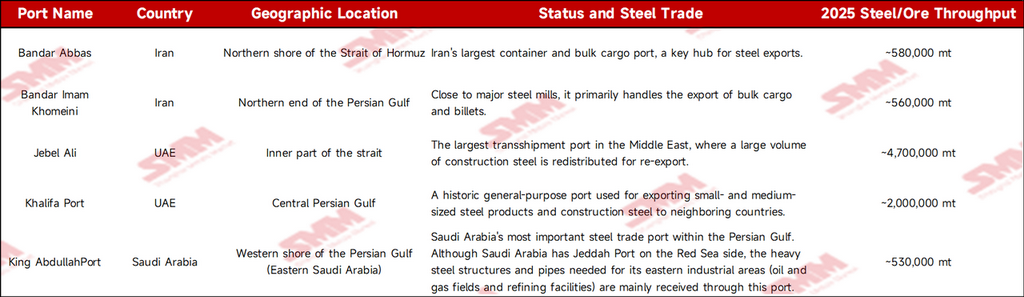

Impact Assessment of Core Ports within the Strait of Hormuz

Should a physical blockade occur at this strategic chokepoint, the five most directly affected key inner-bay ports experiencing “instant logistics paralysis” would be: Port of Bandar Abbas, Port of Khomeini, Port of Jebel Ali, Port of Khalifa, and King Abdullah Port. Simultaneously, a Strait blockade would threaten to disrupt approximately 10% of global seaborne steel trade (primarily semi-finished products and specialty ores). Iran's production of direct reduced iron (DRI) also holds significant weight in global supply; any disruption could drive up costs for electric arc furnace steelmaking in the Middle East.

Data Source: SMM Ferrous Metal Shipping

-

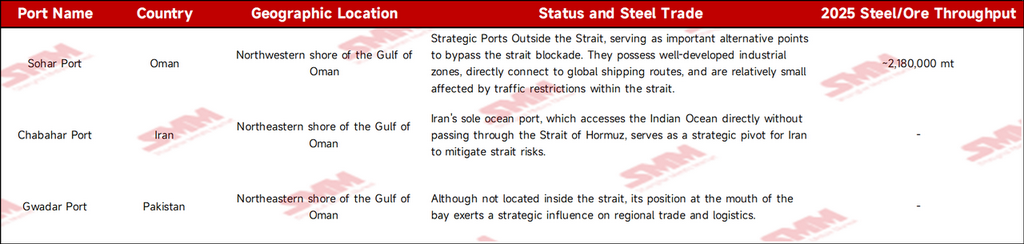

After the blockade, will goods become completely impossible to transport?

While maritime routes will indeed come to a near standstill, the flow of goods won't cease entirely. It will simply become extremely costly, slow, and require complex overland transshipment. For instance, strategic alternative ports outside the strait include Sohar Port, Chabahar Port, and Gwadar Port.

Data Source: Compiled by SMM based on publicly available information

-

Trade Chokehold Triggered by Insurance Withdrawals

Equally severe as the strait blockade is the withdrawal of war risk insurance. Marine insurers Skuld and Gard have announced they will cancel war risk coverage due to escalating tensions in the Middle East. Local feedback from the UAE indicates most insurers refuse to underwrite war risk insurance for the Red Sea. This means traders must bear multiple uncontrollable factors and assume all consequences, which will significantly impact new orders.

-

Summary: The Hormuz Crisis's “Hedging Effect” on China's Steel Market Leads to Short-Term Export Pressure

Short-Term Negative Impact (Suppression of Demand and Logistics): The sudden halt in Gulf shipping routes will cause China's total exports to Middle Eastern countries like Saudi Arabia and the UAE to plummet dramatically. Export disruptions may even force resources to flow back into the domestic market, intensifying supply pressure and exerting downward pressure on steel prices.

Data Source: SMM, GACC

Mid-term outlook: As a major steel supplier, Iran's halted exports will trigger tightening supply of steel billets in Southeast and South Asia.

-

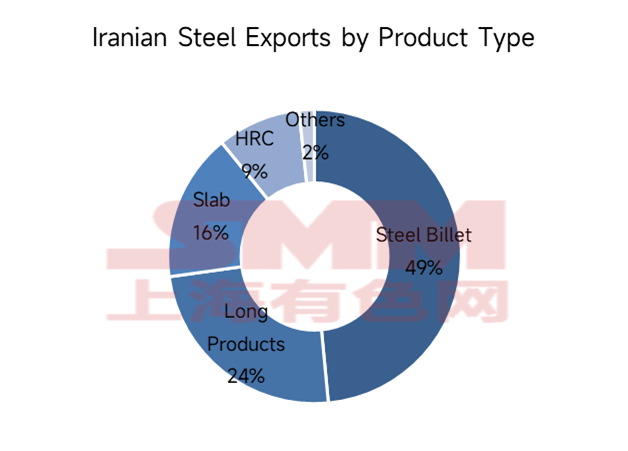

From Construction to Industry: Iran's Steel Export Structure Transformation and the Peak Era Dominated by “Billet”

According to data released by the Iranian Steel Producers Association (ISPA), 2025 marked the “peak era” for Iran's steel exports, with its export structure exhibiting an extremely aggressive trend:

① Absolute Dominance of Semi-Finished Products: From March to December 2025, Iran's billet exports reached 4.58 million tons (+37.7% YoY), while slab exports hit 1.54 million tons (+44.6% YoY). This confirms the earlier observation that the current strait blockade will trigger significant “slab panic” among downstream steel mills in Southeast Asia and the Middle East.

② Structural Leap in Flat Products: Finished flat product exports surged from 307,000 tons in the same period last year to 1.03 million tons. Notably, the significant increase in hot-rolled coil (867,000 tons) and coated steel (up 76.7% YoY) indicates Iran's gradual transition from a “construction steel supplier” to an “industrial raw material supplier.”

③ Weakness and contraction in long products: In contrast, exports of finished long products (rebar, wire rod) declined by 9.9%, while structural steel exports plummeted by 27.7%. This trend of “reducing long products while increasing flat products” has, against the backdrop of stalled infrastructure projects, actually heightened the risk of inventory buildup for finished goods.

Data Source: ISPA

-

Mid-term positive factors: Cost and substitution support

Iran's steel export shortfall of nearly 11 million tons will trigger regional supply tightness, forcing some Southeast Asian and South Asian buyers to shift procurement to China, creating “substitution-driven incremental demand.” Simultaneously, rising crude oil prices may push up costs across the entire industrial chain, providing bottom-up support for steel prices. Although logistics disruptions and project suspensions will suppress export performance in the short term, the reshuffling of the global supply landscape is expected to partially offset the negative impact. Chinese steel may play a key role in filling the global gap.

Long-term outlook: Iran's ceasefire may temporarily impact the global steel market

-

Hoarding effect under blockade: Iran's sharply rising mill and port inventory pressures

According to the latest global steel statistics report released by the World Steel Association (WSA), Iran's cumulative crude steel production reached 31.8 million tons in 2025, marking a year-on-year increase of approximately 1.4% compared to 2024 and solidifying its position as the world's tenth-largest steel producer. In December 2025, Iran's monthly crude steel output hit 3 million tons, a significant year-on-year increase of 16.2%. This indicates that Iranian steel mills were operating at peak capacity just before the conflict erupted. In January 2026, its crude steel output reached approximately 2.6 million tons, marking a 15.1% year-on-year increase. Against the backdrop of a 6.5% year-on-year decline in global crude steel production during January, Iran demonstrated an “independent trend.” According to SMM research, the high production levels from earlier periods have led to severe inventory backlogs at domestic steel mills. The logistics blockade that began in late February prevented the full shipment of steel produced during this high-output phase out of the Persian Gulf. Consequently, ports and mill warehouses are now stockpiling large quantities of slabs and billets originally intended for export. Once the situation eases, this “low-priced inventory” could flood the market at dumping prices. However, considering Iran's post-ceasefire reconstruction needs and the actual release of these supplies, SMM will continue to monitor developments closely.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[China Iron Ore Brief] Iron ore concentrates prices in west Liaoning may consolidate](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)