Panoramic Analysis of China's Magnesium Foreign Trade: Market Games and Coexisting Risks

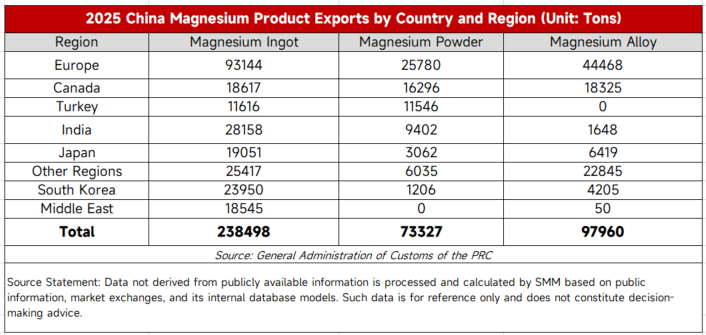

In the magnesium industry, China possesses 100% full industrial chain capabilities ranging from primary magnesium to magnesium alloys and magnesium powder production. According to statistics from SMM and Customs data, China's primary magnesium production accounts for over 90% of the global total. In 2025, China's annual export volume of magnesium ingots reached 251,300 tons, magnesium powder 73,600 tons, and magnesium alloys 99,600 tons. The foreign trade market accounts for 40%-45% of the overall magnesium trade, serving as a vital demand support for the domestic magnesium industry.

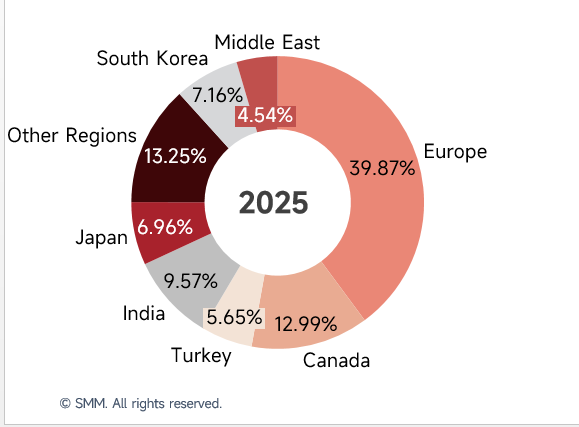

From the perspective of the 2025 export market structure, the European region—with the Port of Rotterdam in the Netherlands as the main landing point—accounted for 40% of China's magnesium export demand. Canadian demand accounted for 13%, with European and American markets maintaining high import scales across the three major categories of magnesium ingots, powder, and alloys. In the magnesium ingot segment, annual export volumes to India, South Korea, Japan, Turkey, and the Middle East (including the UAE, Saudi Arabia, and Qatar) also performed prominently, primarily flowing to local traders and terminal industries such as aluminum processing and automobile manufacturing.

In 2025, SMM data showed that the average annual price of magnesium ingot 9990 FOB was $2,323/ton, a 12% decrease compared to 2024. The downward trend in export prices was influenced on one hand by the callback of magnesium prices in main production areas, but the deeper reason lies in the fact that China's export market remains a buyer's market: competition among traders is fierce, large overseas enterprises generally adopt a bidding model, and small to medium enterprises also compare prices across multiple parties, leading to the continuous compression of export profits. Regarding order modes, although FOB Tianjin Port is used as the quotation benchmark, customers in Europe, the Middle East, India, Japan, and South Korea prefer signing at CIF or CFR destination port prices. This forces foreign trade merchants to not only bear the risk of domestic price fluctuations but also handle multiple variables such as payment cycles, exchange rates, and ocean freight, resulting in profit margins being squeezed layer by layer. The current industry "involution" (internal competition) persists, and risks in the foreign trade market have further intensified recently due to geopolitical conflicts and policy changes.

Core Event 1: US-Israeli Joint Military Strike on Iran; Middle East Tensions Escalate Abruptly

According to foreign media reports, the United States and Israel launched a large-scale joint military strike against Iran on Saturday, February 28, local time. The Pentagon named the operation "OPERATION EPIC FURY." This marks the second military strike by the U.S. against Iran since Trump returned to the White House in January last year, with the first occurring last June targeting Iranian nuclear facilities.

-

Direct Impact: Middle East Magnesium Export Channels Blocked; Ocean Freight Suspended The recent escalation of military conflict has dealt a substantial blow to the magnesium export market in the Middle East. Regions such as Bahrain and Dubai are major demanders of magnesium ingots. According to Customs data, China's export volume of magnesium ingots to the Middle East (excluding Turkey) was 18,500 tons in 2025. According to SMM research, shipping companies for the Middle East route have currently stopped quoting and suspended shipments for March, as the situation remains unclear. Traders reported that some orders placed in the Middle East in February were originally scheduled for March delivery but can no longer be shipped as planned.

-

Indirect Impact: Oil Price and Capacity Fluctuations Propagate; India and Europe Also Affected Tensions have triggered rising oil prices and shipping capacity fluctuations, further affecting the broader export market. Today, ocean freight quotes for the India region have doubled, with the possibility of further increases. 2025 data shows that India's demand for magnesium ingots was 28,000 tons and magnesium powder was 12,000 tons. Although the European market is mainly transported via the Cape of Good Hope route, quotes and shipment statuses have also become unclear due to capacity reallocation and market sentiment. Overall, this conflict has caused significant disruption to nearly half of China's magnesium export market.

Core Event 2: Upgrade of China's Export Controls to Japan; Magnesium Products Included in Dual-Use Item Review

On January 6, 2026, the Ministry of Commerce issued the "Announcement on Strengthening Export Controls of Dual-Use Items to Japan," explicitly prohibiting the export of dual-use items to Japanese military users, for military purposes, and related end-users. As a typical dual-use metal, magnesium has been officially included in the scope of control. This means that magnesium exports to Japan will face stricter compliance review processes, and related trade activities are expected to become more cautious.

-

Market Impact: Restricted Exports to Japan; Traders Turning Cautious Customs data shows that in 2025, China's export volume of magnesium ingots to Japan was 19,000 tons, with magnesium powder and alloys also maintaining a certain scale. According to SMM research, since the announcement, traders have become significantly more cautious regarding exports to Japan. Some traders who previously accepted Japanese orders currently have goods undergoing compliance review at ports or are in a wait-and-see state. Overall, since January 2026, the trade activity of magnesium products to Japan has declined, compliance review cycles have lengthened, and market operations have become more prudent.

Future Outlook: Magnesium Ingot Foreign Trade Market Faces Dual Pressure in 2026; Challenges Intensify

In the short term, ocean freight market fluctuations triggered by geopolitical conflicts are bringing greater uncertainty and risk to foreign trade merchants. Soaring freight rates, shipping delays, and the suspension of bookings on some routes directly push up fulfillment costs. Some terminal orders may be lost due to poor price transmission, and some cases of "shipping at a loss" may even occur. In this context, the overall export scale of the foreign trade market may face phased compression pressure.

In the long term, although China remains the world's primary supplier of magnesium ingots, the buyer-led structure of the export market has not fundamentally reversed. If overseas buyers continue to suppress prices and the bidding model persists while domestic demand growth gradually pushes up ex-factory magnesium prices, the game between internal and external price differences will further intensify, and foreign trade profit margins will likely continue to face pressure. Under this dual squeeze, the future export scale of magnesium products may face risks of further contraction. In fact, the "involution" model of cutthroat competition and low-price bidding is no longer sustainable. Only by returning to rational quoting and ensuring reasonable profit margins can the sustainable development of magnesium foreign trade be supported and China's global dominance in the magnesium industry be solidified.

SMM will continue to monitor geopolitical situations, shipping changes, and policy trends to track the subsequent evolution of the magnesium foreign trade market.