Under a no-policy-impact scenario, SMM estimates Zimbabwe's total lithium production to reach 200,000 tonnes LCE in 2026, accounting for 9% of global primary lithium supply.

Following the export ban, as official implementing rules have not yet been released by the authorities, SMM has developed three scenarios to assess the impact on global lithium supply:

1. If only lithium sulfate can be exported: Zimbabwe could supply 17,000–35,000 tonnes LCE in 2026, representing 8%–16% of the country's original supply capacity, a reduction of 170,000–190,000 tonnes LCE.

2. If companies with processing capacity can export both lithium concentrate and lithium sulfate: Zimbabwe could supply 90,000–140,000 tonnes LCE in 2026, representing 45%–70% of the country's original supply capacity, a reduction of 60,000–110,000 tonnes LCE.

3 . With beneficiation capacity, enterprises can export spodumene concentrate + lithium sulfate. In 2026, Zimbabwe's lithium resource supply is expected to reach nearly 150,000-170,000 tons, accounting for 75%-85% of the previously projected supply, representing a decrease of 30,000-50,000 tons compared to the earlier forecast.

Assuming the ban on raw ore and lithium concentrate exports remains in effect throughout 2026, while lithium sulfate exports are permitted, SMM's assessment of the impact magnitude is as follows:

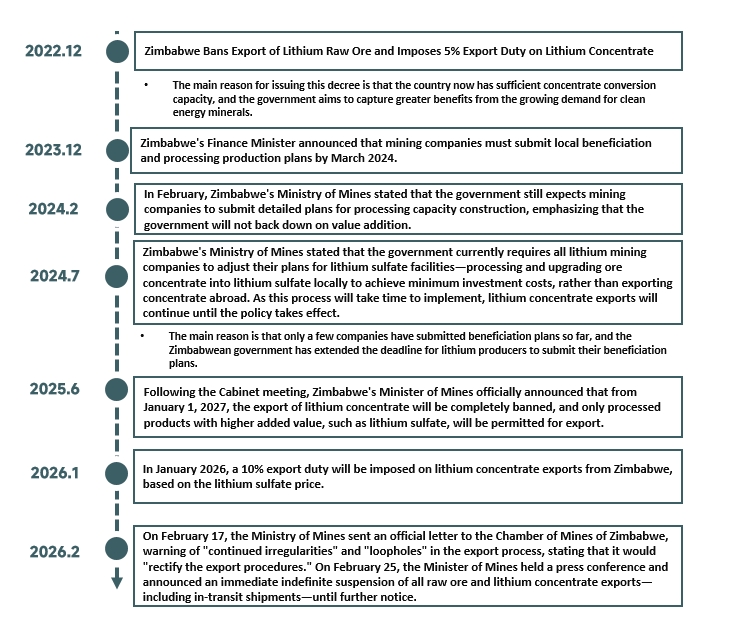

1. Timeline of Public Information on Zimbabwe's Lithium Export Restrictions

Source: SMM compilation based on public information

2. 2026 No-Policy-Impact Scenario

SMM estimates Zimbabwe's lithium supply would reach 200,000 tonnes LCE in 2026, representing:

- Over 15% year-on-year growth from 2025

- 10% of global primary lithium supply in 2026

- 17% of global spodumene supply in 2026

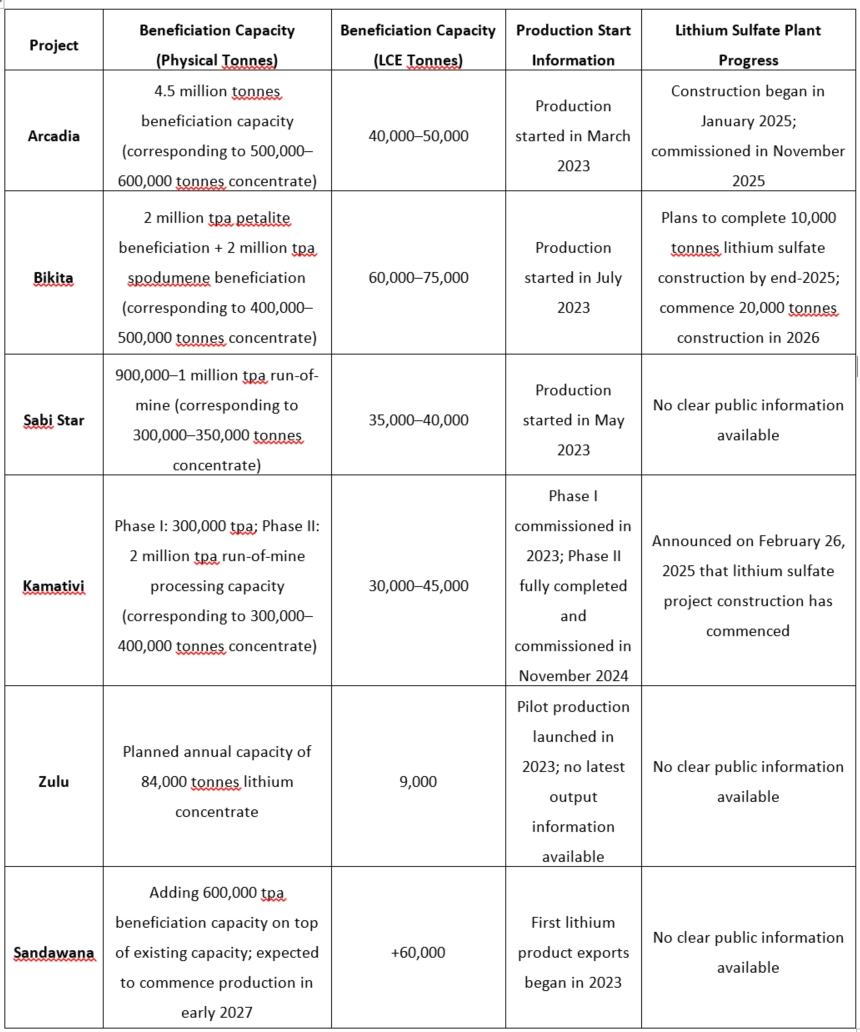

3. Major Operating Mines in Zimbabwe

Major Lithium Mining Projects in Zimbabwe

Source: SMM compilation based on public information

Notes: Based on public information:

- Zimbabwe's average spodumene grade ranges from 1.06–1.98%, with concentrate grades of 4.0–5.5%. Conversion ratio: 9.5:1 (concentrate to LCE)

- Petalite grades range from 0.8–1.8%, with concentrate grades of 3.0–4.2%. Conversion ratio: 16:1 (concentrate to LCE)

- References also made to individual companies' public disclosures

Project Updates:

- Arcadia and Bikita submitted beneficiation plans to Zimbabwe's Ministry of Mines in 2024

- Arcadia: Lithium sulfate project construction began in January 2025, with initial design capacity of 50,000 tonnes. Commissioning began in October 2025, currently in ramp-up stage. Lithium sulfate exports experienced some delays in mid-to-late February 2025

- Bikita: Announced in its May 2025 investor relations presentation that it plans to complete 10,000 tonnes lithium sulfate construction by end-2025, and commence 20,000 tonnes construction in 2026

- Kamativi: Announced on February 26, 2026, that its Zimbabwe lithium sulfate project has commenced construction

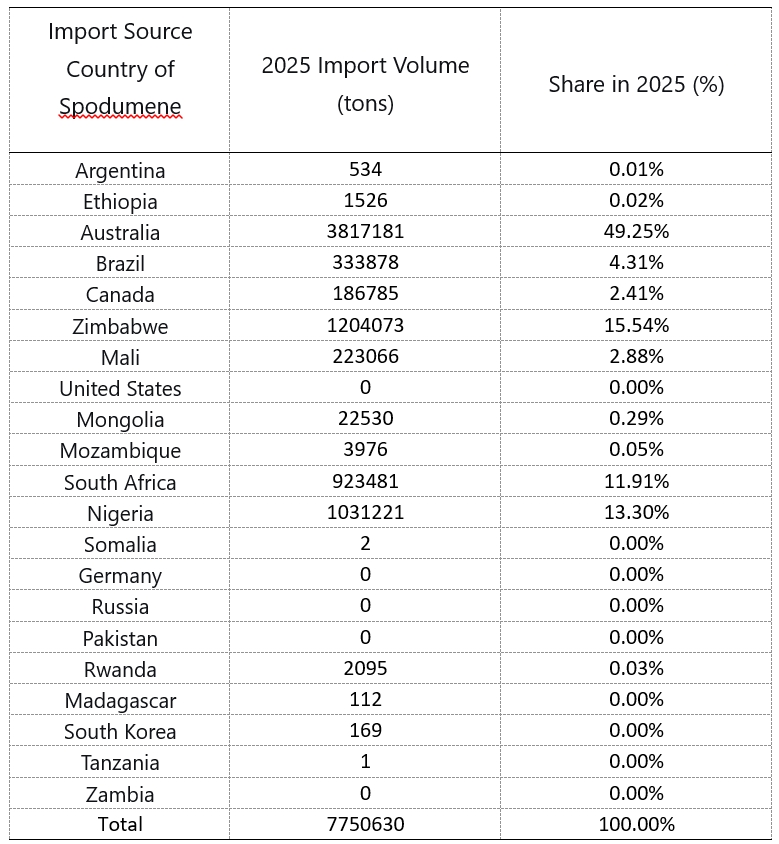

4. China's Lithium Spodumene Imports (2025)

Zimbabwe supplied over 1.2 million tonnes of spodumene to China in 2025, accounting for approximately 15% of China's total imports.

Lithium Spodumene Imports by Source Country (2025)

Source: China Customs, SMM compilation

5. Project Comparison: Arcadia Lithium Sulfate Plant Construction and Ramp-Up Timeline

Construction to commissioning takes approximately one year. If the export ban remains in effect throughout 2026:

- Arcadia and Bikita are confirmed to be able to export lithium sulfate

- Based on Kamativi's February 26, 2026 public announcement, it may also be able to export lithium sulfate. As Kamativi's capacity plans have not yet been disclosed, certain assumptions have been made regarding its output.

No-Policy-Impact Baseline: Zimbabwe's Expected Total Output Approaching 200,000 Tonnes LCE in 2026. Scenario Analysis: Impact of Export Ban on Supply

(1) Only lithium sulfate can be exported:

a. No export procedure required (Arcadia + Bikita + Kamativi): Zimbabwe will have an exportable lithium resource volume of 30,000–35,000 tons LCE in 2026, accounting for 16% of the country's total annual lithium supply, with an affected volume of nearly 170,000 tons LCE;

b. Export permit application process required for lithium sulfate (policy pending clarification, assuming a two-month processing period) (Arcadia + Bikita + Kamativi): Zimbabwe will have an exportable lithium resource volume of 17,000 tons LCE in 2026, accounting for 8% of the country's total annual lithium supply, with an affected volume of nearly 190,000 tons LCE.

(2) Companies with smelting capacity can export both lithium concentrate and lithium sulfate:

a. No export procedure required (Arcadia + Bikita + Kamativi): Zimbabwe will have an exportable lithium resource volume of 140,000 tons LCE in 2026, accounting for 70% of the country's total annual lithium supply, with an affected volume of nearly 60,000 tons LCE;

b. Export permit application process required for lithium concentrate+ lithium sulfate (policy pending clarification, assuming a two-month processing period) (Arcadia + Bikita + Kamativi): Zimbabwe will have an exportable lithium resource volume of nearly 90,000 tons LCE in 2026, accounting for 45% of the country's total annual lithium supply, with an affected volume of nearly 110,000 tons LCE.

(3) Enterprises with beneficiation capacity may apply to export spodumene concentrate + lithium sulfate:

a. If the export procedure takes one month to complete (policy not yet clarified; this is an estimate only): Zimbabwe is expected to be able to export approximately 170,000 tons LCE of lithium resources in 2026, accounting for 85% of the country's originally projected annual supply, with a reduction of nearly 30,000 tons LCE.

b. If the export procedure takes two months to complete (policy not yet clarified; this is an estimate only): Zimbabwe is expected to be able to export approximately 150,000 tons LCE of lithium resources in 2026, accounting for 75% of the country's originally projected annual supply, with a reduction of nearly 50,000 tons LCE.

![[Lithium Battery: Yongtai Technology And CATL Sign Electrolyte Cooperation Agreement]](https://imgqn.smm.cn/usercenter/GVVKq20251217171728.jpg)

![[SMM Analysis] The Real Barriers to Upgrading Africa’s Battery Metals Value Chain](https://imgqn.smm.cn/usercenter/WyqWW20251217171729.jpg)