SMM Feb 23 News:

Holiday Performance Review:

During the Chinese New Year break, LME zinc prices first declined then rose. Throughout the holiday, the 40-day moving average provided consistent support on the daily candlestick chart. After the market opened, LME zinc prices pulled back, hitting a weekly low of $3,253/mt, before rebounding steadily and closing at $3,378/mt on Friday—up $35.5/mt WoW, a gain of 1.06%. LME zinc inventory stood at 101,575 mt, down 650 mt from pre-holiday levels, with the decrease mainly from Singapore warehouses.

Trading was subdued during the break. Early in the week, a stronger US dollar weighed on nonferrous metals, but bargain hunting emerged later. Toward the weekend, PMI data from various countries were released: February manufacturing PMI readings for Germany, the UK, and the Eurozone exceeded expectations, while the US S&P Global Manufacturing PMI fell short. The US dollar index retreated from highs, and a US Supreme Court ruling against large-scale tariffs imposed by former President Trump provided macro tailwinds, boosting market sentiment. In addition, the LME zinc 0-3 spread remained in a slight contango, and zinc ingot inventories stayed low. These factors combined led LME zinc to decline first and then rise over the holiday period.

Post-Holiday Outlook:

From a macro perspective, the US Supreme Court’s tariff ruling initially softened the US dollar index, offering some support to nonferrous metals. However, Trump later announced a 15% tariff on all imported goods, raising market uncertainty and concern. Ongoing overseas geopolitical tensions also contribute to macro-level risks, warranting continued attention to subsequent macro guidance.

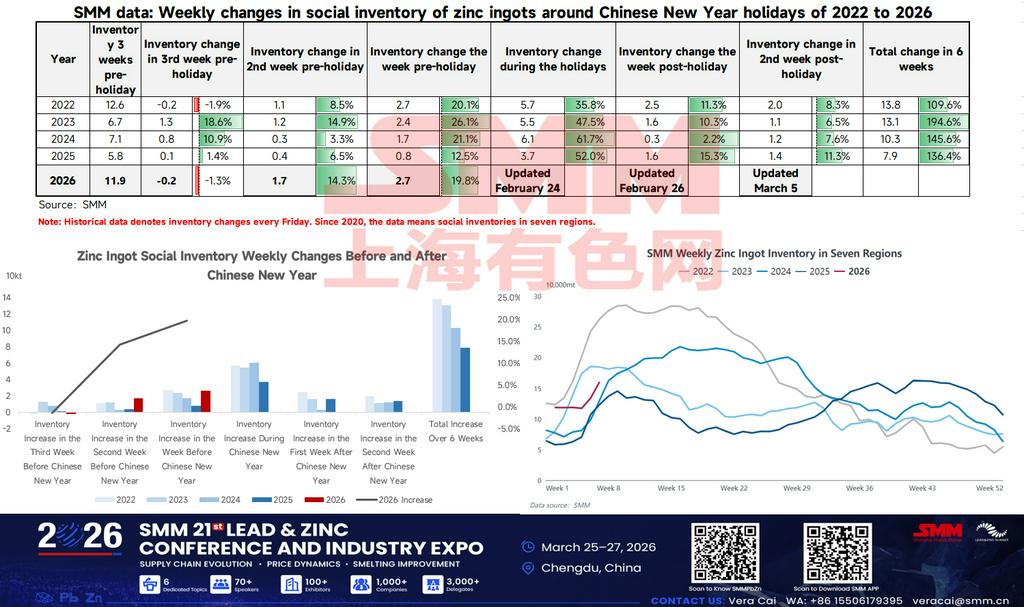

On the fundamentals side, February coincided with the Chinese New Year break, during which some domestic smelters underwent maintenance or halted production. SMM estimates domestic refined zinc output fell by approximately 50,000 mt MoM, indicating a supply-side slowdown. Demand was also weak, as most downstream zinc processors suspended operations around the holiday. According to SMM, holiday durations ranged from several days to several weeks, with large-scale production resumptions not expected until after the Lantern Festival. Overall downstream demand in February dropped to a yearly low, and social inventory of zinc ingots is expected to see a significant buildup during the break. As a result, fundamentals may provide weaker support for zinc prices. However, if the inventory increase is less than expected, zinc prices could still find some momentum as downstream consumption recovers after the holiday. Continued monitoring of the pace of downstream production resumptions and zinc ingot inventory accumulation is advised.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![July Refined Zinc Production Continues to Decline, Watch Actual Maintenance at Major Smelters [SMM Analysis]](https://imgqn.smm.cn/usercenter/cirme20251217171754.jpg)