SMMJanuary 30 Report:

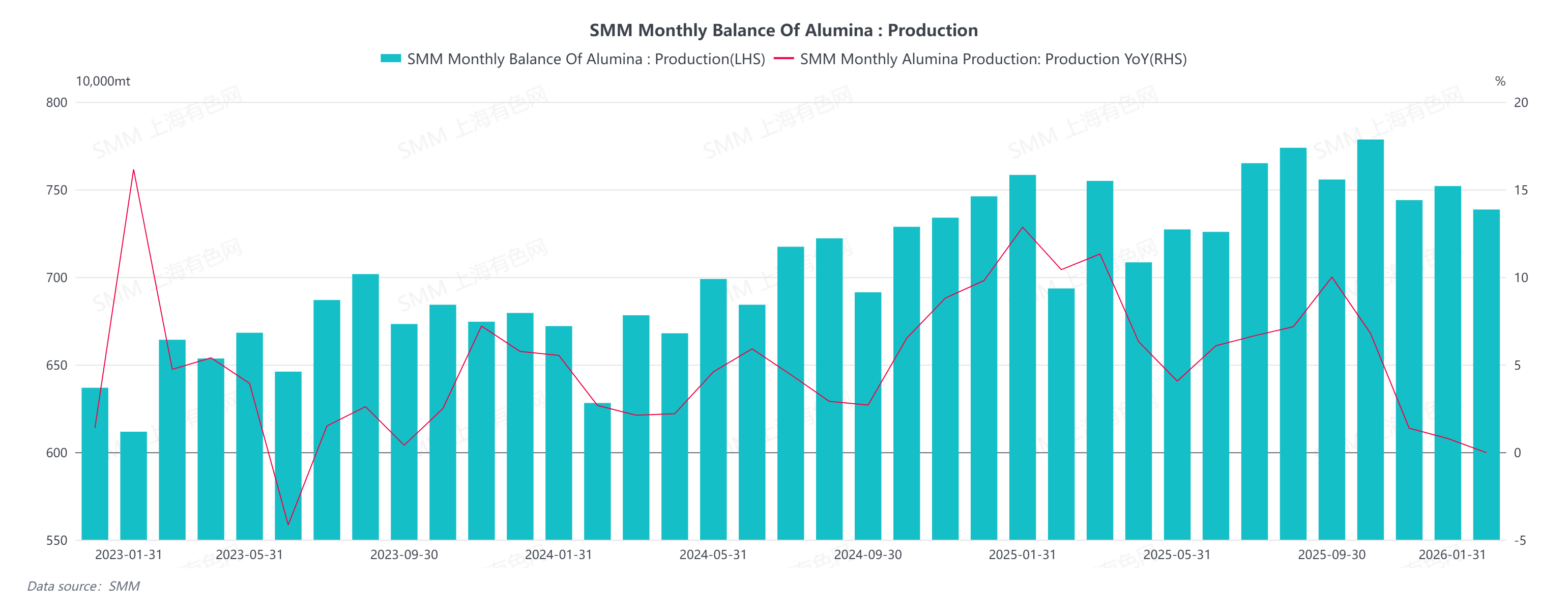

China's metallurgical-grade alumina production in January 2026 decreased by 1.78% month-on-month and 2.6% year-on-year. As of the end of January, the national built capacity was approximately 110.32 million tons, with operating capacity down 1.78% month-on-month and 3.56% year-on-year, indicating a slight contraction in overall industry production.

The decline in output this month was primarily driven by phased maintenance and environmental controls. Early in the month, some northern enterprises underwent routine annual maintenance, affecting a portion of production. In mid-month, an alumina plant in Henan province commenced a full maintenance shutdown due to environmental policy requirements, further impacting output. Additionally, enterprises in regions such as Guizhou and Guangxi initiated annual maintenance around mid-month, with capacity affected close to half for some plants. Although maintenance capacities in Henan and other areas gradually resumed by month-end, full-month production remained somewhat constrained.

Looking ahead to February, the alumina market is expected to maintain a supply surplus situation. Continuously declining prices are increasing operational pressure on producers, likely prompting more enterprises to adjust supply through production line upgrades and maintenance. Regarding imports, December recorded a net import of approximately 20,000 tons, adding some pressure to the market. However, as domestic prices fall rapidly—with prices in northern China already below overseas levels—import volumes are expected to gradually decrease starting in January. Coupled with weakening downstream restocking sentiment ahead of the Spring Festival, demand support remains limited. Overall, operating capacity in February is projected to be around 86.248 million tons, with the market continuing in a state of oversupply.