[SMM Steel Import and Export Special Topic] Outward Leap Under Domestic Demand Restructuring: A Panoramic Analysis of the Deep-Seated Logic Behind China's Steel Export Surge in 2025(Prat1)

- Breaking Outward, Restructuring Inward: The Five-Year Advancement of China's Steel Trade Global Layout

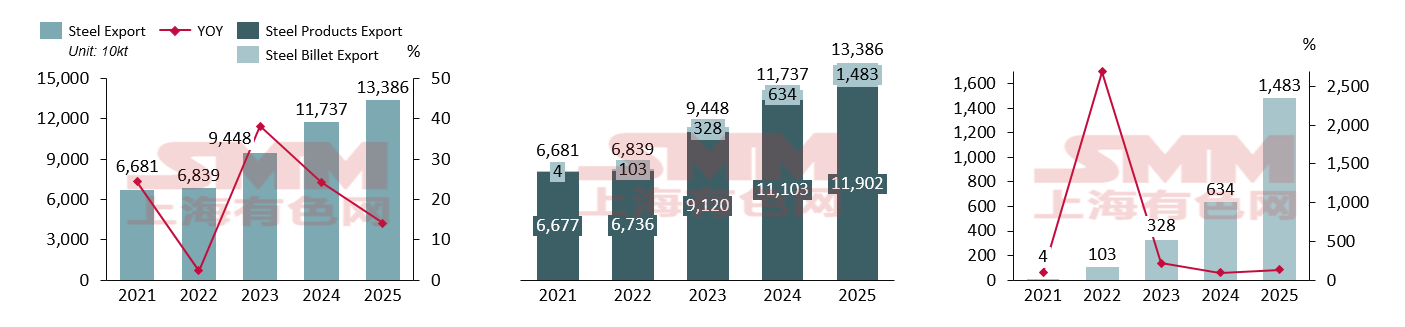

Over the past five years, China's steel exports have undergone a qualitative transformation from "volatile recovery" to "structural surge." From 2021 to 2022, exports remained within the traditional range of 60-70 million mt. However, starting in 2023, the export growth curve steepened sharply. In 2025, the total broad exports, including steel billet, reached a new high of 134 million mt, with a YoY growth rate of 14%. The underlying driver of this explosive growth is the long-term mismatch between domestic supply and demand. As the real estate sector entered a period of deep adjustment, domestic apparent consumption continued to shrink. However, due to the inertia and economies of scale in steel production processes, China's crude steel production did not decline proportionally. This "supply-demand scissors gap" forced Chinese resources to flow overseas, seeking markets with higher prices, greater profits, and more robust demand.

The most notable product in China's steel exports in 2025 was undoubtedly steel billet. Steel billet exports exploded from an almost negligible 40,000 mt in 2021 to 14.83 million mt in 2025, increasing hundreds of times over five years. The high growth in 2022 was primarily due to the outbreak of the Russia-Ukraine conflict, which created significant gaps in markets previously supplied by Russian and Ukrainian billets, providing substitution opportunities for China to expand its billet exports. The growth in 2025 largely stemmed from finished steel products facing increasingly severe anti-dumping and anti-circumvention investigations overseas. As a semi-finished product, steel billet enjoys low or even zero tariffs in most countries, and with China's low prices, many enterprises chose to export billets, entering overseas markets in semi-finished form for further processing, effectively circumventing trade protections on finished products.

Data Source: General Administration of Customs、SMM

Data Source: General Administration of Customs、SMM

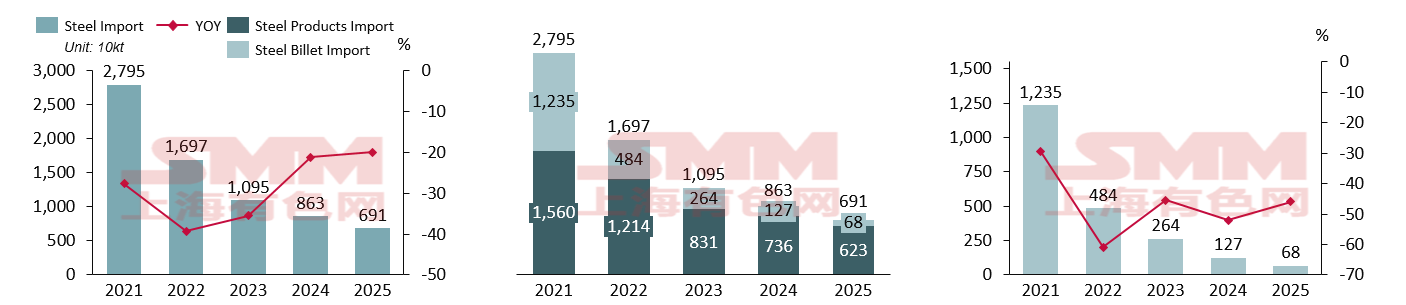

In contrast, the import market showed a completely opposite trend compared to exports. Total imports declined year after year from 27.95 million mt in 2021, shrinking to 6.91 million mt by 2025, a drop of over 75% over the five-year period. The YoY growth rate consistently remained in the negative range of -20% to -40%. The core reasons are: ① Accelerated domestic substitution: With the release of domestic special steel and high-end sheets & plates capacity, high-end varieties previously reliant on imports achieved self-sufficiency. ② Weakening cost-driven advantages: Global supply chain cost fluctuations and domestic overcapacity diminished the cost-effectiveness advantages of imported steel. ③ Transformation in domestic demand: Slowing growth in domestic downstream manufacturing combined with industrial upgrading further pressured demand for traditional imported resources.

As domestic electric furnace steel and high-standard blast furnace processes matured, previously imported low-cost primary resources, such as overseas low-cost steel billet, lost competitiveness in terms of freight and carbon compliance, leading to a consecutive annual decline in import share. However, we must also deeply recognize the need to closely monitor the few high-end varieties still reliant on imports, such as high-end mold steel and top-grade bearing steel. Only by achieving precise substitution as soon as possible can China's steel industry complete the ultimate transition from "dependence" to "high-end exports." In the future, enterprises should focus more on the depth of "import substitution" for high value-added products rather than solely relying on trade scale.

Data Source: General Administration of Customs、SMM

- Global Flow Analysis: Asia's Core Role and Regional Diversification

Data Source: General Administration of Customs、SMM

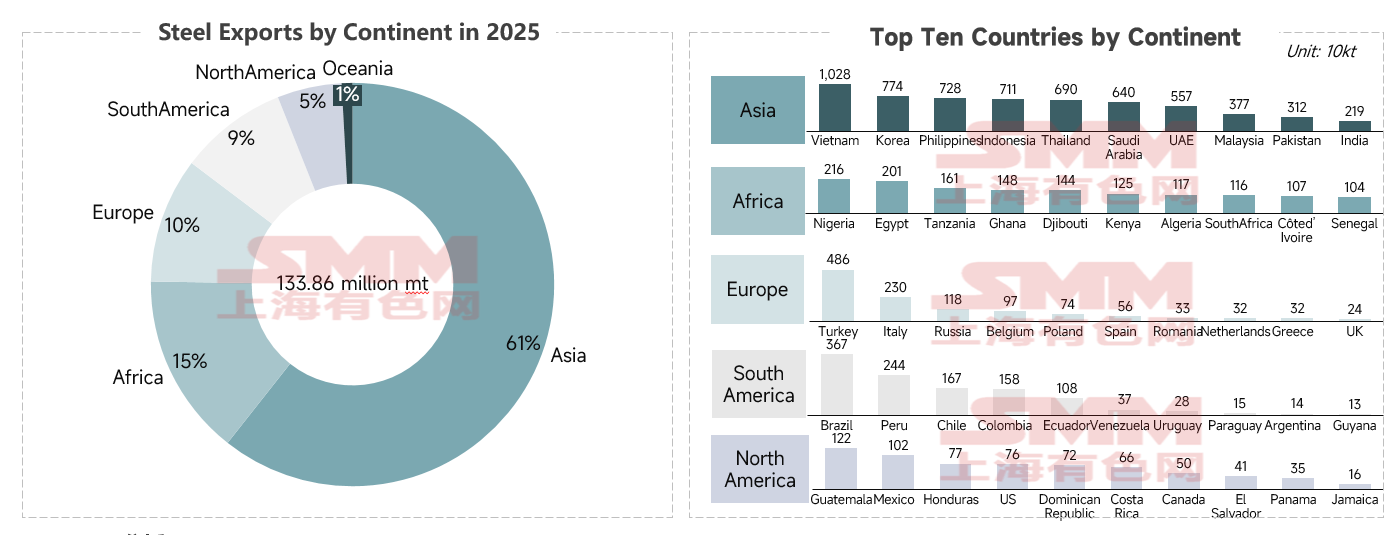

Based on 2025 steel export data by continent, China's global steel distribution is clear: ① The Asian market remains the absolute trade center (61% share), contributing over 81.5 million mt of exports. Among these, ASEAN countries, in the acceleration phase of industrialization and urbanization, have huge demand for construction steel like rebar and wire rod, as well as basic sheets & plates. Meanwhile, deep industrial chain interactions in shipbuilding and automobiles exist between China and South Korea, with China's cost-effective hot-rolled coil being a key raw material for downstream manufacturing. Additionally, cost advantages in near-field logistics make Chinese products highly competitive in the Asian market. As of January 26, 2026, China's hot-rolled coil export FOB offer was approximately $465/mt, significantly lower than India's $480/mt, Japan's $495/mt, and Turkey's $535/mt.

② Africa, Europe, and South America serve as the supporting layer with three dominant players: Africa (15%) saw Nigeria, Egypt, and Tanzania as the main growth drivers, boosted by infrastructure linkages under the Forum on China-Africa Cooperation and local livelihood projects, with the African market being highly price-sensitive, where Chinese plain steel holds dominance. In Europe (10%), Turkey, with 4.86 million mt of imports, became the largest "transshipment hub" and consumer of Chinese steel in the region. In South America (9%), Brazil, a representative country, imported 3.67 million mt of Chinese steel, showing strong demand, primarily driven by heavy industries such as mining and agricultural machinery, which boosted consumption of special steel.

③ The "long-tail" effect in the North American market: In the regional ranking, the US (760,000 mt) ranked even behind Honduras (770,000 mt). This directly reflects how increasingly fierce US-China trade tensions and high tariff barriers have marginalized trade with the US. However, risks and opportunities coexist, forcing Chinese steel to be transshipped via Southeast Asia or Latin America or redirected to emerging markets beyond high barriers. So, let’s take a closer look at which emerging countries showed outstanding growth rates and increments in 2025

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Daily Hot-Rolled Coil Trading] Spot Trading Moved Sideways](https://imgqn.smm.cn/usercenter/JAnHq20251217171716.jpg)