On January 28, 2026, driven by multiple factors, domestic aluminum prices experienced a new round of surge. On that day, the weighted open interest of SHFE aluminum surged by 93,000 lots in a single day, with trading activity exploding. The core reasons for the price increase were the U.S.-Iran geopolitical conflict disrupting trade, capital diversion from precious metals position limits, and rising expectations for alumina production cuts. This represents a typical event-driven and capital-driven rally, sharply contrasting with the current weak fundamentals in downstream sectors. The SHFE aluminum main continuous contract surged 5.75% in a single day, closing at 25,640 yuan/mt, setting another historical high. Simultaneously, the SHFE introduced two major measures—adding two new aluminum ingot delivery brands and raising risk control parameters for multiple varieties—implementing a policy package of "expanding supply and strengthening risk control" to precisely address market anomalies and potential risks, balancing the industrial supply-demand and financial speculation landscape.

Delivery Brand Expansion: Easing Deliverable Supply Pressure and Optimizing Market Supply Structure

On the day, the SHFE announced the addition of Xinjiang Qiya Aluminum & Power's "QY" brand and Geely Baimao Group's "Geely Baimao" brand aluminum ingots as delivery brands, involving a combined capacity of 1.3 million mt across three aluminum plants, marking a significant expansion in the aluminum futures delivery market for the year. According to SMM data estimates, in the absence of new primary aluminum processing enterprises commencing operations, China's actual new deliverable aluminum ingot volume in 2026 is expected to exceed 1 million mt.

Simultaneously with the delivery expansion, the SHFE announced that, starting from the close of trading on January 30, it will raise the price fluctuation limits and margin ratios for products such as alumina, lead, and zinc. Among these, the price fluctuation limit for alumina futures will be adjusted to 9%, and the margin ratios for hedging and general open interest will be raised to 10% and 11%, respectively. Although this adjustment does not specifically target the main aluminum futures contract, alumina, as a core upstream raw material for aluminum, will see its tightened risk control parameters indirectly transmitted to the aluminum industry chain, curbing cross-product speculative linkages.

This move precisely aligns with the current supply-demand imbalance in China's aluminum ingot market. Demand side, the market is currently facing multiple demand constraints: the traditional off-season combined with high aluminum prices significantly suppresses end-user purchase willingness, downstream profile enterprises have already entered their holiday pace ahead of schedule, and aluminum billet processing fees continue to operate at low levels, even reaching "zero processing fees" or "negative processing fees." Against this backdrop, profile plants mostly maintain a wait-and-see attitude with high inventory levels, and stockpiling sentiment is becoming increasingly cautious. Affected by this, more billet plants initiated annual maintenance and implemented production cuts or suspensions in the second half of January, further evidencing the weakness in downstream demand.

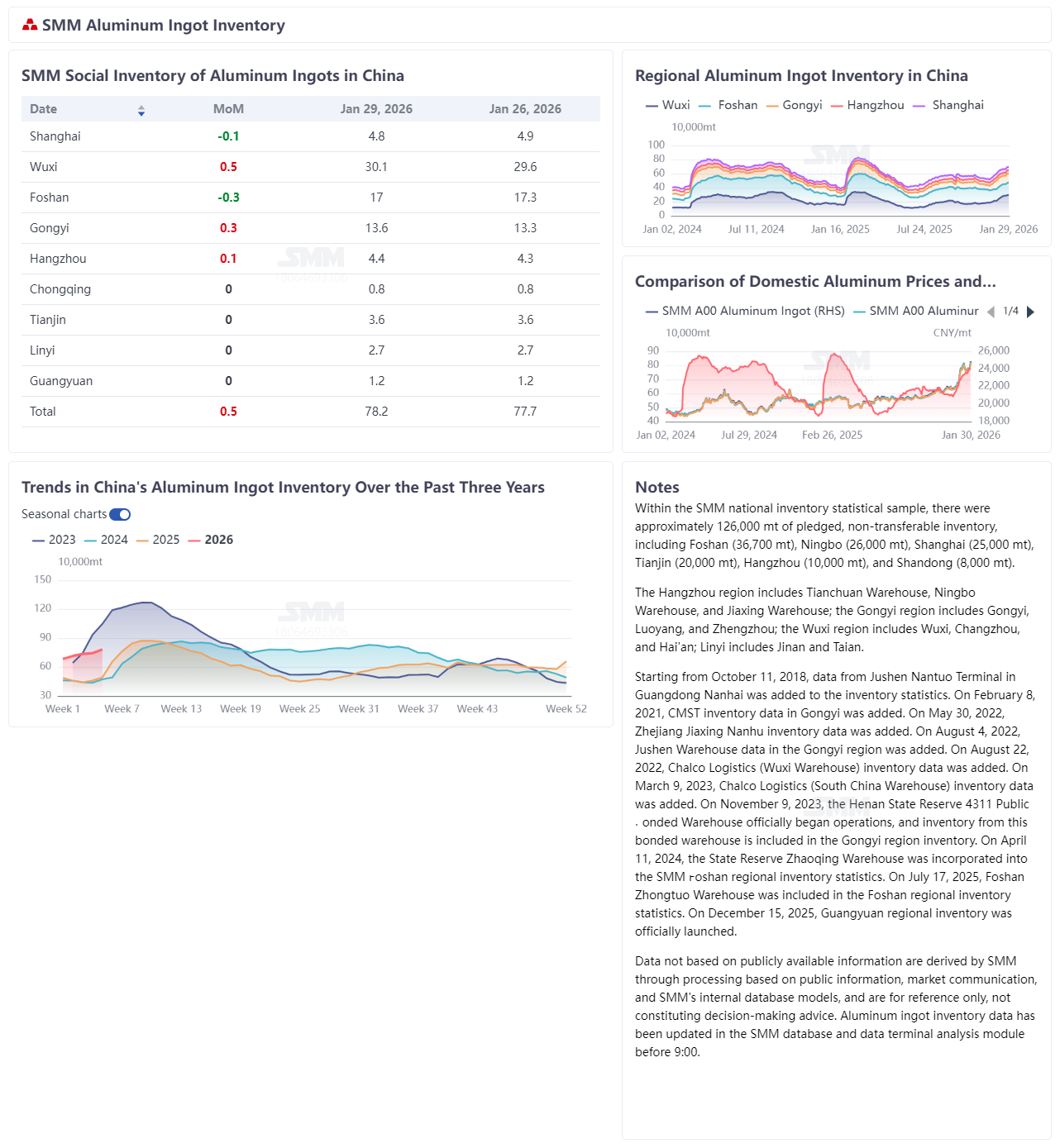

Under the transmission of weakening demand at the beginning of the year, supply and inventory side, the latest SMM data shows that on January 26, aluminum ingot inventory in mainstream consumption areas in China reached 777,000 mt, an increase of 117,000 mt from month-end December, up 18% MoM, reaching a high for the same period in recent three years. SMM temporarily predicts that the inventory peak in 2026 may approach or even exceed the historical peak of 1.269 million mt recorded in 2023. Meanwhile, the decline in the proportion of liquid aluminum has further amplified the supply pressure on aluminum ingots—the proportion of liquid aluminum in domestic aluminum enterprises fell 2.25 percentage points MoM to 72.64% in late January, down 3 percentage points YoY from month-end December. This translates to a theoretical weekly increase in casting ingot volume of 25,000 mt, with a full-month estimated increase of around 100,000 mt, up over 10% MoM from the previous month.

The expansion of delivery brands will effectively absorb the new casting ingot supply, alleviating inventory accumulation pressure in the spot market. SMM believes that the supplementation of delivery resources from Xinjiang and Guangxi production areas not only optimizes the regional layout of SHFE aluminum ingot deliveries, reducing cross-regional delivery logistics costs, but also enhances the price discovery efficiency of the futures market by increasing deliverable targets, reducing the risk of futures-spot divergence against the backdrop of high inventory. For industrial clients, the new delivery brands provide more target options for hedging, helping to strengthen risk management capabilities. Against the backdrop of weak demand and high inventory, price surges driven by capital conceal the risk of corrections. Simultaneously, the SHFE's increase in risk control parameters essentially aims to prevent excessive market speculation and guide market conditions to return to some extent to supply and demand fundamentals by raising trading costs and limiting price fluctuation ranges.

Outlook: Strong Macroeconomic Conditions but Weak Fundamentals; Aluminum Prices Seek New Equilibrium Under Policy Guidance

Overall, the two major measures by the SHFE form a policy mix of "loosening and tightening": the expansion of delivery brands increases supply and improves efficiency in the market, alleviating the tension between high inventory and scarce delivery resources; the upgrade of risk control parameters cools down the overheated market, curbs the spread of speculative sentiment, and precisely counteracts the current divergence in the aluminum market of "strong performance but weak fundamentals."

In the short term, geopolitical conflicts on the macroeconomic front and sector rotation in capital flows will continue to dominate aluminum price fluctuations. However, with the implementation of risk control measures, speculative behavior will be partially constrained, limiting the upside room for prices. Looking ahead, the core contradiction in aluminum fundamentals remains focused on inventory destocking and demand recovery. If post-Chinese New Year downstream resumption falls short of expectations and inventory continues to accumulate, surpassing historical highs, it will exert strong pressure on aluminum prices. Meanwhile, the gradual implementation of new delivery brands will further enhance the anchoring effect of the futures market on spot aluminum, driving prices to partially return to supply-demand fundamentals and seek a new equilibrium.

SMM cautions that the recent sharp rally in SHFE aluminum prices has been driven by event-driven factors and capital inflows, with market sentiment reaching a phase of euphoria. In the subsequent period, vigilance is warranted against sentiment cooling and price corrections triggered by multiple factors. Market participants should rationally use futures tools to hedge against price volatility, manage positions prudently, and avoid chasing rallies. SMM will continue to monitor macroeconomic liquidity performance, U.S.-Iran conflict developments, the implementation of alumina production cuts, and the pace of downstream stockpiling before the Chinese New Year and post-holiday resumption. These factors will collectively determine the future direction of the aluminum market.

![Buying Sentiment Recovered Slightly from the Previous Day but Remained Weak [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/wStpx20251217171650.jpg)