2025 has concluded, with the copper cathode rod industry experiencing continuous fluctuations throughout the year in line with copper price trends, and the industry's operating pace repeatedly oscillating. Looking back on the year, what characteristics did the operating performance of copper cathode rod enterprises exhibit? What are the market's expectations for the industry in 2026?

(I) Copper Prices Hit Record Highs in H2, Copper Cathode Rod Industry Faces Triple Challenges of Cost, Demand, and Inventory

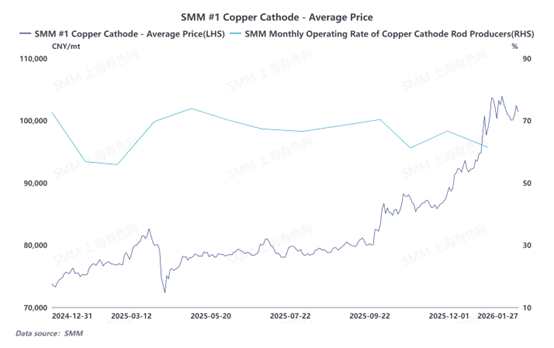

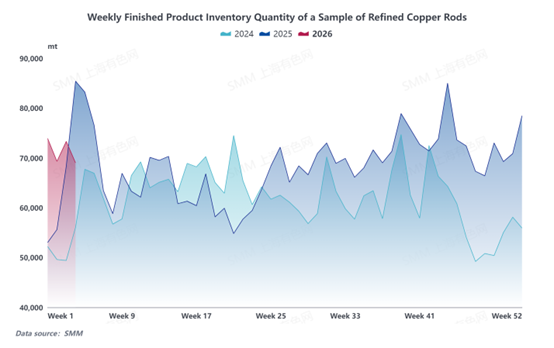

In 2025, the core contradiction of severe overcapacity and an imbalanced supply-demand relationship in the copper cathode rod industry persisted throughout the year, coupled with sharp fluctuations in copper prices, resulting in a clear divergence in industry performance between H1 and H2. In H1, driven by a temporary demand boost from copper price limit-downs and the PV installation rush, the industry's operating rate remained high. In H2, copper prices began a steep rise, with the SMM #1 copper cathode average price breaking through the 100,000 yuan/mt mark and hitting a record high. The impact from raw materials was quickly transmitted downstream, leading to weak demand in the wire and cable and enamelled wire markets, sluggish new orders, sustained pressure on processing fees, and narrowing profit margins for enterprises. The industry's overall operating rate remained below normal levels for an extended period. Copper cathode rod operating rates showed a significant negative correlation with copper price trends, gradually pulling back as copper prices rose, fully reflecting the dual constraints of high copper prices and weak demand on production activity. Notably, in the early stages of the copper price increase, enterprises maintained regular operations to preserve market share, but downstream procurement demand continued to shrink, and finished product inventories entered a buildup cycle ahead of other indicators. In H2, inventories generally exhibited a fluctuating upward trend, further intensifying operational pressures in the industry and ultimately leading to a phase of "weak demand—high inventories—profit pressure."

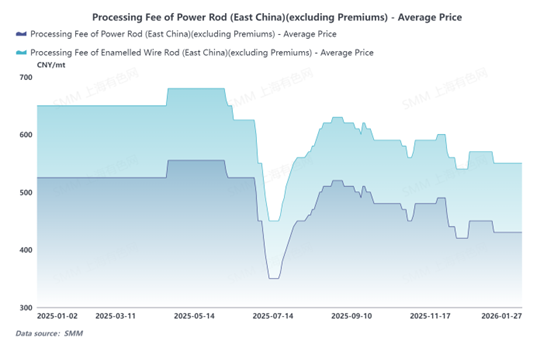

From the perspective of processing fees, the copper cathode rod processing fees in the power and enamelled wire industries experienced significant fluctuations in 2025. In June, coinciding with the mid-year period, enterprises rushed to meet production targets amid fierce competition among traders, pushing processing fees downward under pressure, with instances of zero processing fees occurring within the month. After the mid-year period, processing fees gradually recovered to normal levels. Subsequently, influenced by continuously rising copper prices, processing fees pulled back again. Looking ahead to 2026, the core issue of severe capacity surplus and supply-demand imbalance in the copper cathode rod industry is expected to persist. Enterprises within the industry will compete for limited orders, further intensifying market competition, and the state of involution is unlikely to ease quickly, continuing to exert pressure on processing fee levels. Therefore, SMM expects that copper cathode rod processing fees will remain under pressure overall in 2026, continuing a weak downward trend.

(II) Increased Copper Price Volatility in 2025 Led Copper Cathode Rod Enterprises to Adjust Long-Term Contract Strategies

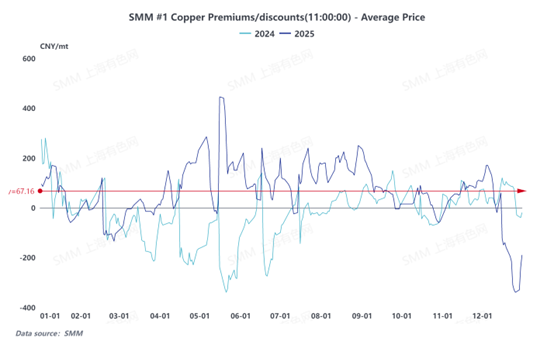

In 2025, copper prices experienced wild swings, with a limit-down trend occurring in April during H1. Starting from September, driven by multiple factors such as the re-emergence of arbitrage opportunities in LC price spreads, tight supply in non-U.S. regions due to tariffs, disruptions in the mine sector, and high market expectations for copper demand in emerging sectors, copper prices continued to rise and repeatedly hit record highs. The significant volatility in copper prices, combined with severe overcapacity and persistent supply-demand imbalances in the domestic copper rod industry, led to a shift in the pricing logic for spot and long-term contracts in the copper cathode rod sector. Looking back at 2024, spot premiums/discounts were substantially lower than long-term contract prices for most of the period, and copper cathode rod enterprises suffered deep losses in their long-term contract businesses with downstream customers. This operational challenge persisted into 2025. Although the average annual spot premium/discount for SMM standard-quality copper reached 39.22 yuan/mt in 2025, a price difference still existed compared to the offers under long-term contracts signed with smelters. As a result, during the 2026 long-term contract negotiation phase, copper cathode rod enterprises showed a greater preference for signing contracts with floating premiums/discounts or proactively reducing the proportion of fixed long-term contracts to minimize losses.

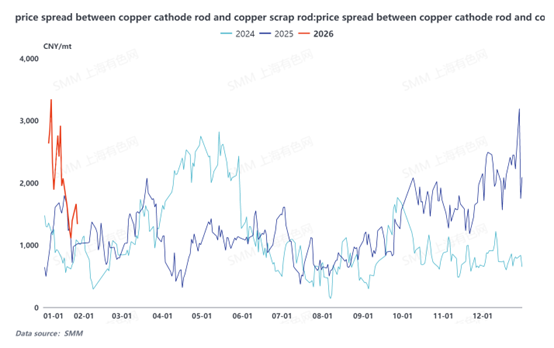

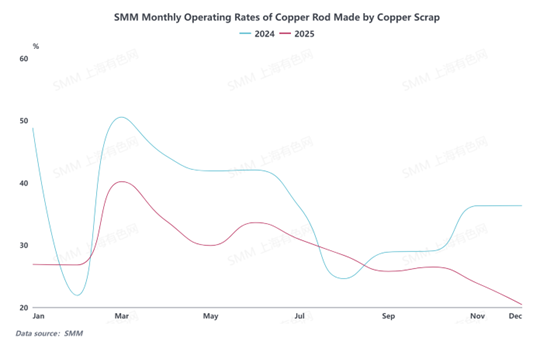

(III) Copper Prices Surge, Price Difference Between Primary Metal and Scrap Widens, Impact of Secondary Copper Rod on Copper Cathode Rod Falls Short of Expectations

The price of the most-traded SHFE copper contract continues to surge, theoretically opening up significant substitution potential for the price difference between primary metal and scrap. The widening price spread has also prompted wire and cable enterprises to consider purchasing secondary copper rods to reduce costs, leading many copper cathode rod enterprises to worry that secondary rods may squeeze their market share. However, due to distortions in the implementation of reverse invoicing policies, uncertainties arising from the cleanup of local tax havens, coupled with tight invoice quotas for enterprises and strained capital chains, production and sales willingness among secondary rod enterprises remain weak. The phenomenon of halting production to wait and see is prominent, and the industry's operating rate continues to be low. Therefore, despite rising copper prices driving an expansion in the price difference between primary metal and scrap, the actual impact of secondary copper rods on the copper cathode rod market has not reached the level previously expected by the market.

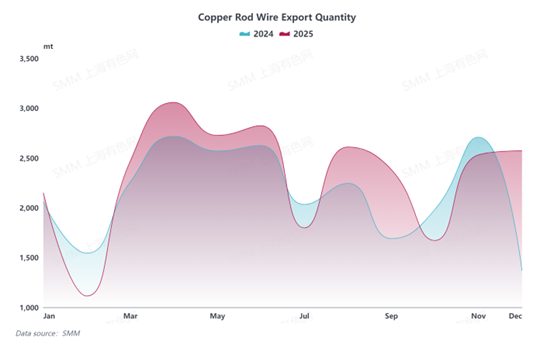

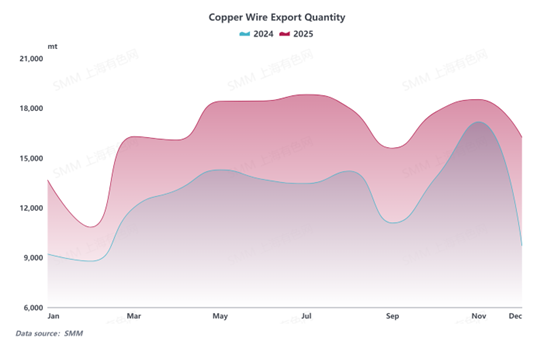

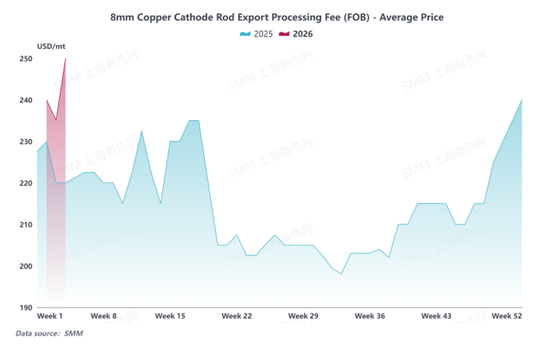

(IV) Transformation of Trade Models Facilitates Recovery of Copper Rod Exports, with Significant Growth in 2025 and Promising Prospects for the Future

Although affected by policy adjustments in the earlier stage, the export volume of mainstream copper rod export enterprises in China experienced a phased decline. However, as the industry's trade model gradually shifted from Ordinary Trade to processing trade, multiple enterprises actively expanded their export business and proactively applied for processing trade manuals. Subsequently, export volumes gradually returned to normal levels and achieved a slight increase. In 2025, China's overall copper rod exports increased by approximately 50,000 mt compared to 2024. Looking ahead to 2026, the domestic copper rod industry remains in a landscape characterized by weak domestic demand and intensified competition in processing fees. With expanding export profit margins, more enterprises are accelerating their expansion into overseas markets to seek new growth opportunities. It is expected that China's overall copper rod exports will maintain a slight upward trend in 2026. Notably, due to rising costs of imported copper raw materials, although the long-term contract processing fees for domestic 8mm copper rod exports have been raised, the increase falls short of market expectations.

In summary, the copper cathode rod industry in 2025 was dominated by sharp fluctuations in copper prices, with the operating pace oscillating repeatedly throughout the year. The sharp surge in copper prices, coupled with weak downstream demand, led to fluctuations in processing fees, limited profitability, and high inventory levels, putting overall production and operation under pressure. Looking ahead to 2026, the trend of copper prices, the recovery process of downstream demand, and the effectiveness of overseas market expansion will remain key factors influencing the industry's development. Enterprises are also expected to continue adopting more flexible business strategies to actively respond to the complex and ever-changing market landscape.