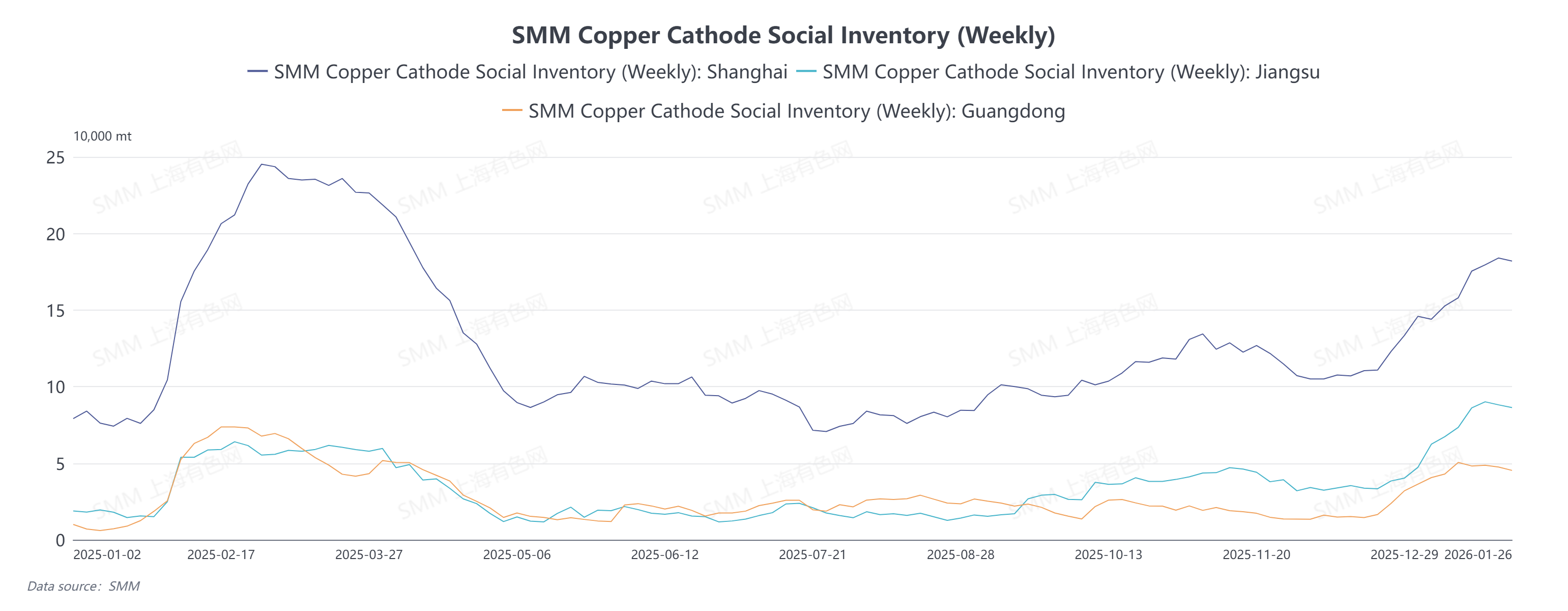

SMM social inventory of copper cathode continued to climb since the end of 2025, reaching a phase high of 330,200 mt on January 22. This week (January 26) data showed the first decline, down 5,700 mt MoM from January 22, with inventories in Shanghai, Jiangsu, and Guangdong all dropping back slightly. Meanwhile, copper prices retreated from highs since mid-January, with the SMM #1 copper cathode average price falling from 104,000 yuan/mt on January 14 to around 101,400 yuan/mt on January 27. On the surface, the pattern of "falling prices and declining inventory" aligns with the traditional logic of demand improvement. However, considering spot market performance, the destocking driver did not stem from robust end-use consumption.

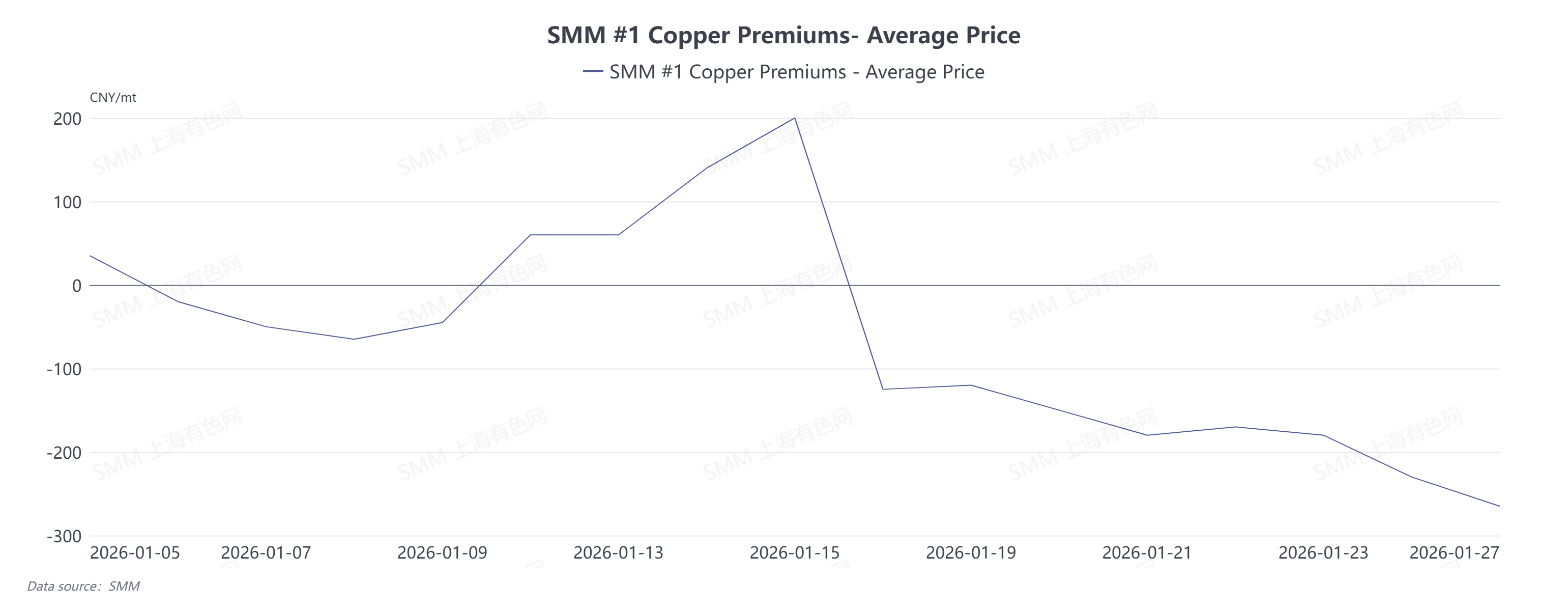

In contrast to the inventory decline, the spot market has shown a clear discount structure since early January, which can be divided into two phases: As the 2601 contract approached delivery, influenced by suppliers tightening spot availability to deliver warrants, spot discounts quickly narrowed from an average discount of 65 yuan/mt at the beginning of the month, turning into a premium structure between January 12 and 15, with the peak reaching an average premium of 200 yuan/mt. However, this premium was actually a "structural premium" driven by delivery behavior, not accompanied by a substantial recovery in downstream consumption. After the contract rollover on January 16, market logic shifted rapidly, and spot prices against the 2602 contract immediately turned to an average discount of 125 yuan/mt. Under the dual pressure of persistently high inventory and weak downstream consumption, spot selling pressure continued to increase. Although the widening Contango price spread between futures contracts provided some support for spot premiums/discounts, it still could not reverse the overall market oversupply situation, with the average discount falling to a recent low of 265 yuan/mt by January 27. Downstream purchasing only occurred occasionally when copper prices touched psychological price levels, indicating weak and non-resilient demand.

Based on spot market performance, the recent decline in social inventory is mainly due to a temporary reduction in arrivals in north China, combined with some rigid demand for cargo pick-up triggered by the earlier pullback in copper prices to key levels. However, the driving force behind this destocking is clearly insufficient. The spot market continues to experience deep discounts and sluggish trading, with no sustained improvement. Downstream consumption is limited to buying the dip rather than trend stockpiling, indicating that demand is highly sensitive to prices and lacks resilience. At the same time, supply pressure has not dissipated. Domestic smelters are maintaining high operating rates, and supply remains ample in major consumption areas such as east China. Therefore, this inventory decline should be viewed more as a result of fluctuations in the pace of arrivals and the short-term release of flexible demand, rather than a signal of substantial and sustainable recovery in end-use consumption.

According to SMM communication with enterprises:

- Trader 1: Recently, there is little intention to sell, and they plan to consider selling only when discounts exceed 200 yuan/mt. Now that the price spread between futures contracts has widened, it is enough to cover rollover costs, and they are even considering stockpiling until April for sales.

- Trader 2: Currently, both supply and demand are weak. Everyone is worried that smelters will continue shipments. If we purchase too much now, we will have limited funds left. If smelters suddenly release several thousand metric tons of goods at a discount of more than 300 yuan/mt between February 8 and 10 before the Chinese New Year, everyone will regret it, as they won’t be able to purchase at even lower prices. That’s why everyone is staying calm now.

- Downstream 1: We’ve observed that when the front-month copper contract is around 99,500 yuan/mt, end-users become more active, and orders increase slightly. However, most actual orders are placed near 99,000 yuan/mt. Customers are like that—when they see a lower price, they want an even lower one.

- Downstream 2: Recently, non-registered copper cathode supply has been relatively tight. Because the price spread is indeed large, producers tend to bid up prices, so we generally prefer to purchase earlier. We’re not holding much inventory now and are buying on a daily basis.

Looking ahead to the market around the Chinese New Year, the "triple suppression" pattern of high inventory, wide price spreads between futures contracts, and deep discounts is expected to be difficult to reverse in the short term. Before the Chinese New Year: Wide price spreads amid high inventory will strengthen suppliers’ willingness to ship to delivery warehouses, thereby suppressing spot market liquidity and buying interest. Spot premiums/discounts lack momentum for recovery and are expected to remain in a discount structure. If smelters engage in distress selling, discounts may widen further. After the Chinese New Year: The key validation point for the market will be the extent and speed of post-holiday inventory buildup. If significant inventory accumulation occurs, it will reinforce the perception of weak demand and may force spot premiums/discounts to move even lower.