SMM January 27, 2026 News:

In 2025, SMM expects global secondary refined lead production to exceed 8.3 million mt, accounting for 66% of the total global refined lead supply. Globally, secondary lead has surpassed primary lead as the main supply source, which is the most significant structural feature of the global lead industry.

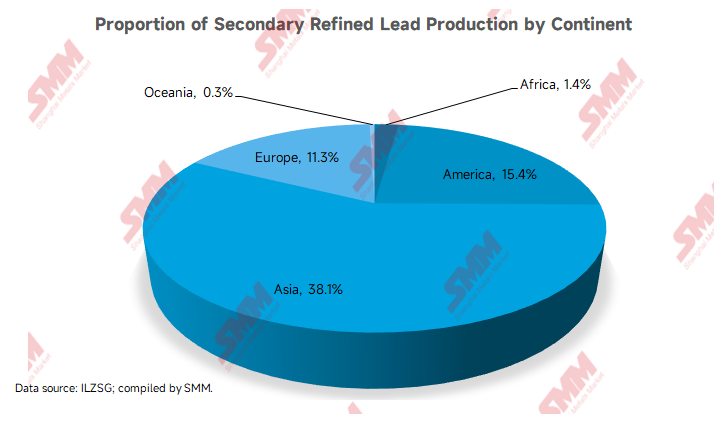

According to ILZSG data, global secondary refined lead production is mainly distributed in Asia, the Americas, and Europe.

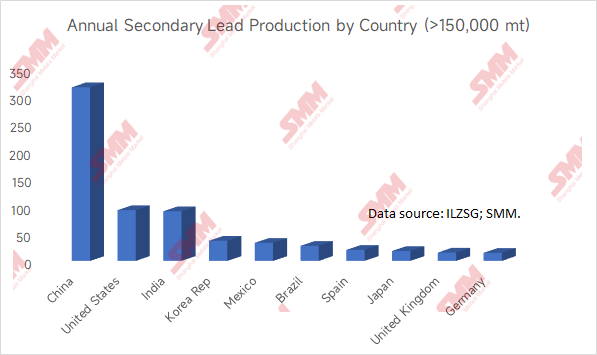

Ten countries have annual secondary refined lead production exceeding 150,000 mt, with China, the US, and India ranking as the top three.

Globally, about 21 countries have both primary and secondary lead production capacity, among which 17 have higher secondary lead production than primary lead. Notably, China has exited the group of countries where secondary lead production exceeds primary lead production. This is due to severe overcapacity in China's secondary lead sector, leading to significant industry losses and dampening smelters' production enthusiasm.

Against this backdrop, in recent years, Chinese secondary lead smelters have gradually shifted to Southeast Asia, with countries such as Malaysia, Thailand, Pakistan, and the Philippines being more popular due to low labour and raw material costs. According to SMM, as Chinese secondary lead enterprises continuously enter the Southeast Asian market, local companies' operating profits have gradually come under pressure. Local governments have implemented regulations in areas such as environmental protection and taxes, making the operating environment for Chinese secondary lead enterprises less favorable than initially. Additionally, some countries in West Asia possess advantages in raw materials due to high automobile ownership, strong demand for backup power supplies for telecom base stations, and rapid growth in solar-plus-ESS projects. These regions have also established well-developed waste battery recycling networks. While opportunities exist, challenges such as "unstable security situations and financial isolation" remain. In the short term, however, Asia will maintain its absolute dominance in global secondary lead production.

From a global perspective, SMM expects Africa to become the main region attracting investment in lead smelting in the future. In September 2024, the Beijing Summit of the Forum on China-Africa Cooperation (FOCAC) and the Ninth Ministerial Conference were held in Beijing. The meeting highlighted China’s unilateral support for key initiatives in Africa over the next three years. These include granting zero-tariff treatment to 100% of product categories for the least developed countries that have diplomatic relations with China, supporting the development of local value chains, manufacturing, and deep processing of critical minerals in Africa, establishing five regional China-Africa industrial cooperation growth circles, and building supporting facilities for 10 industrial parks. These measures are favorable for lead smelting and trade. Africa is highly likely to become the fastest-growing emerging market, with significant potential for increasing its share of secondary lead production.

Both Europe and the Americas have undergone an evolution in secondary lead smelting, from early simple recycling to modern industrial processing, spanning approximately 470 to 500 years. They have formed highly integrated systems from recycling to remanufacturing. Factors such as oligopoly, high labour costs, and stringent environmental protection standards make these regions less suitable for new entrants.

The development of secondary lead in Oceania spans about 50 years. Due to sparse population and urban distribution, its market size is relatively limited. Additionally, high logistics costs hinder the collection of waste lead-acid batteries. High labour and environmental protection costs in Oceania are also unfavorable for the development of secondary lead smelting enterprises.

In summary, global secondary lead capacity is currently concentrated in Asia. In the future, Africa has significant potential for growth in the secondary lead industry. The shares of Europe and the Americas in the secondary lead industry are expected to decline steadily, while Oceania’s share will remain relatively stable in the short term, with limited potential for future development.

![Tug-of-War Between Sellers and Buyers Continues, Short-Term Lead Price Fluctuation Trend Difficult to Break [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)