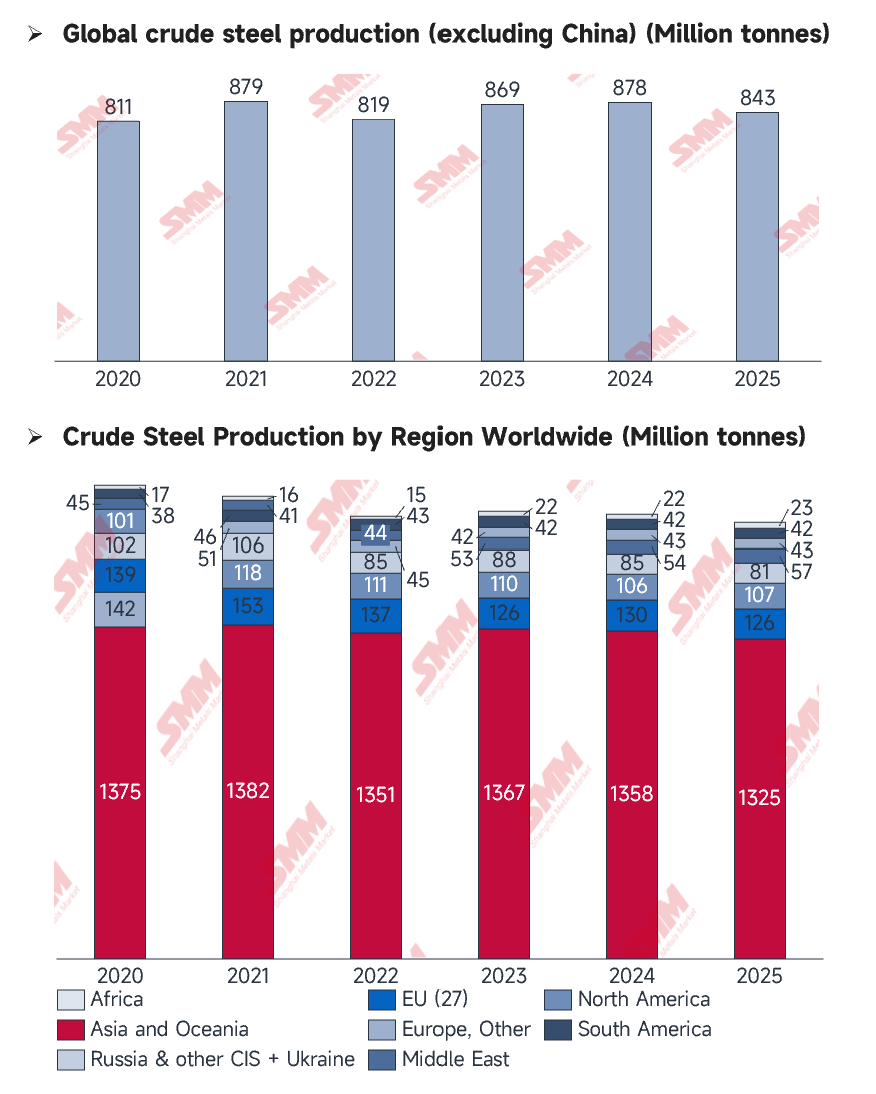

In 2025, the global steel industry experienced a profound geographic and structural pivot. While total production tracked by the World Steel Association (worldsteel) reached 1.8494 billion tonnes, the overseas market (excluding China) demonstrated notable resilience, growing by approximately 1% year-on-year to reach 888.6 million tonnes. This performance marks the beginning of a new cycle driven by overseas domestic demand, where the industry's center of gravity is accelerating its migration toward emerging markets in India, the Middle East, and Southeast Asia.

Source: WorldSteel

Source: WorldSteel

Macro Outlook: Who Is Rising and Who Is Retracting?

The global steel landscape underwent a quiet yet significant reconfiguration in 2025. While demand in parts of Asia remained robust, buoyed by market heating, traditional markets in Europe and North America generally faced stagnant growth. Simultaneously, emerging economies exhibited high activity levels, significantly outpacing the steady but slow-moving mature markets.

The Powerhouse Engines: India, Türkiye, and the Middle East

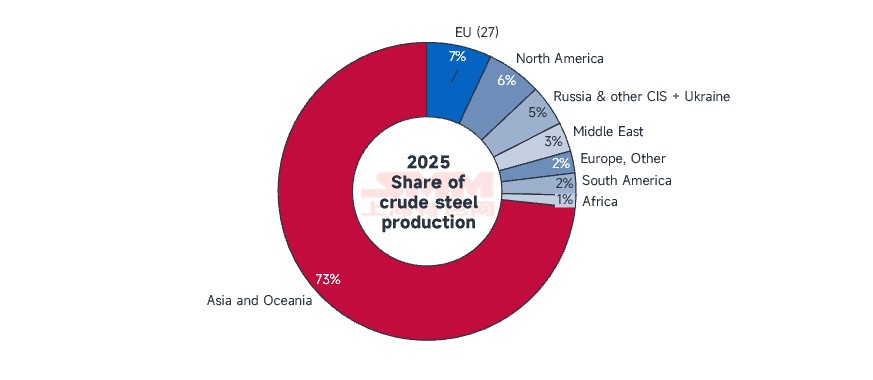

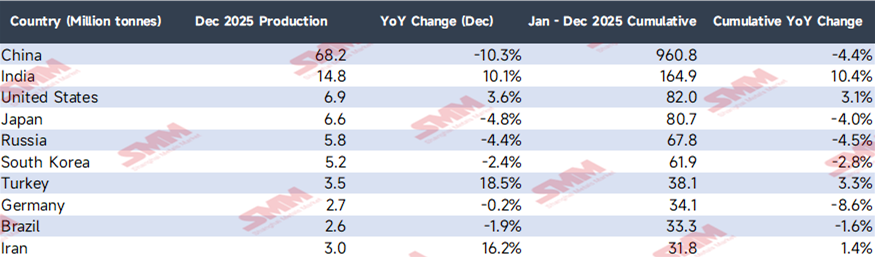

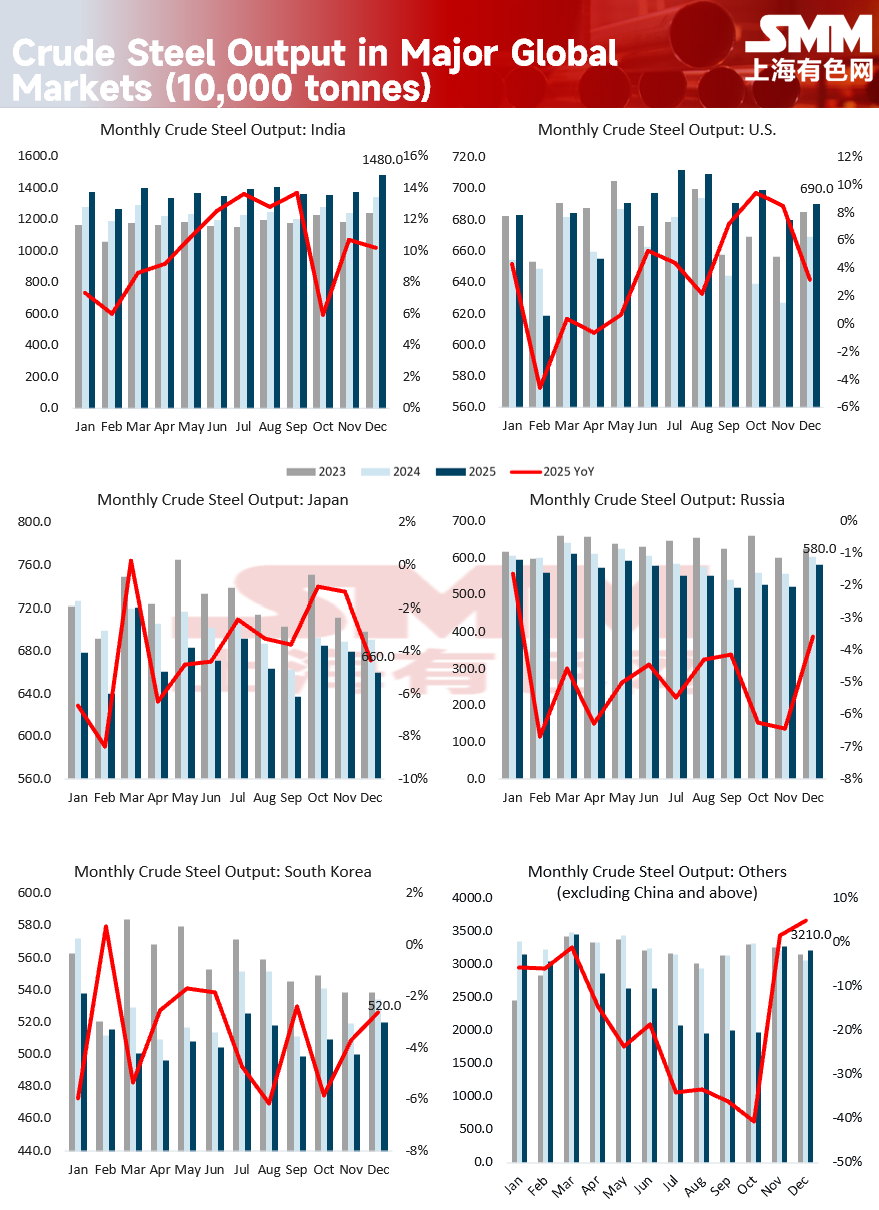

- India: In 2025, India's crude steel production reached 164.9 million tonnes, a dramatic surge of 10.4%, firmly securing its position as the world's second-largest steel producer . This growth was primarily fueled by the government’s $1.4 trillion National Infrastructure Pipeline and the "PMAY" affordable housing scheme.

- Türkiye: Annual production reached 38.1 million tonnes, growing by 3.3%. Benefiting from large-scale reconstruction efforts following the 2023 earthquake and enhanced export competitiveness due to the devaluation of the Lira, Türkiye emerged as one of the standout black horses of the year .

- Middle East: Regional production grew by 4.3% year-on-year. Specifically, Saudi Arabia (+12.3%) and Iran (+1.4%) leveraged energy export dividends to accelerate domestic industrialization.

Traditional Giants in Crisis: Germany and Mature East Asian Markets

- Germany: Production plummeted by 8.6%, reflecting the severe impact of high energy costs and the painful transition of the automotive industry toward electrification.

- Japan and South Korea: Production fell by 4.0% and 2.8%, respectively. Persistent labor shortages hindered domestic construction projects, while their automotive exports faced intense global competition from Chinese electric vehicle (EV) brands.

Source: WorldSteel

Source: WorldSteel

December Focus: "Fire and Ice" in Overseas Markets

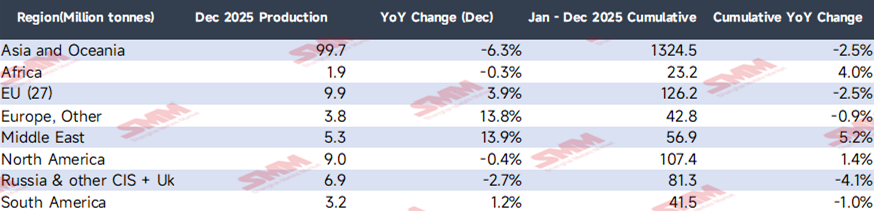

In December 2025, Rest-of-World (ROW) steel output rose by 1.7% to 71.4 million tonnes—one of the strongest monthly totals of the year. This month highlighted sharp contrasts in regional policy and market strategy:

- Türkiye's Year-End Sprint: December production skyrocketed by 18.5% year-on-year. This was driven by aggressive seasonal restocking from European buyers—who faced record-low inventories—alongside an end-of-year rush in domestic reconstruction projects.

- The EU's "CBAM Front-Running" Rebound: EU production saw an unexpected 3.9% increase in December, reaching 9.9 million tonnes. With the Carbon Border Adjustment Mechanism (CBAM) set to enter full implementation in 2026, local mills restarted blast furnaces to bolster domestic supply, anticipating that future imports might be curtailed by carbon cost uncertainties.

- The U.S. "IRA Dividend": December production grew by 3.6%. Despite the pressure of high interest rates, the Inflation Reduction Act (IRA) continued to spur investment in clean energy infrastructure and data centers, providing a stable floor for domestic steel orders.

Source: WorldSteel

Source: WorldSteel

Deep Analysis: Key Variables Affecting Production

-

Structural Demand Shift: From Property to Machinery: Global steel demand is pivoting away from traditional real estate toward manufacturing and high-end energy infrastructure. In India and Southeast Asia, urbanization and transportation networks remain the primary drivers. In the U.S. and Europe, the green energy transition (such as wind power and EV supply chains) has become the core support for high-value flat steel production.

-

Policy Games and Trade Barriers: 2025 saw a wave of protectionist measures. The U.S. reinstated 25% Section 232 tariffs, while the EU tightened safeguard quotas. These regional self-sufficiency policies forced global steelmakers to adjust production schedules based on the level of protection in their respective trade blocs.

-

Labor and Energy Constraints: Production cuts in Japan and Germany were largely driven by fundamental survival challenges. In Japan, chronic labor shortages severely delayed construction deliveries, while in Germany, exorbitant electricity prices placed Electric Arc Furnace (EAF) producers at a competitive disadvantage against emerging market rivals.

Source: WorldSteel

Source: WorldSteel

2026 Outlook: Toward a "Green Premium" Balance

![[SMM Analysis]China-Indonesia Steel Price Spread Inverted, Overseas Demand Still Shows No Improvement](https://imgqn.smm.cn/usercenter/wSpkX20251217171718.png)