SMM January 26 News:

At the beginning of 2026, precious and non-ferrous metals experienced a significant rally, with gold, silver, copper, aluminum, and other metals repeatedly reaching new highs. Zinc prices also broke through to their highest level in nearly a year, after which the overall non-ferrous sector hit a "pause." So, what exactly is the market trading, and what points need attention recently?

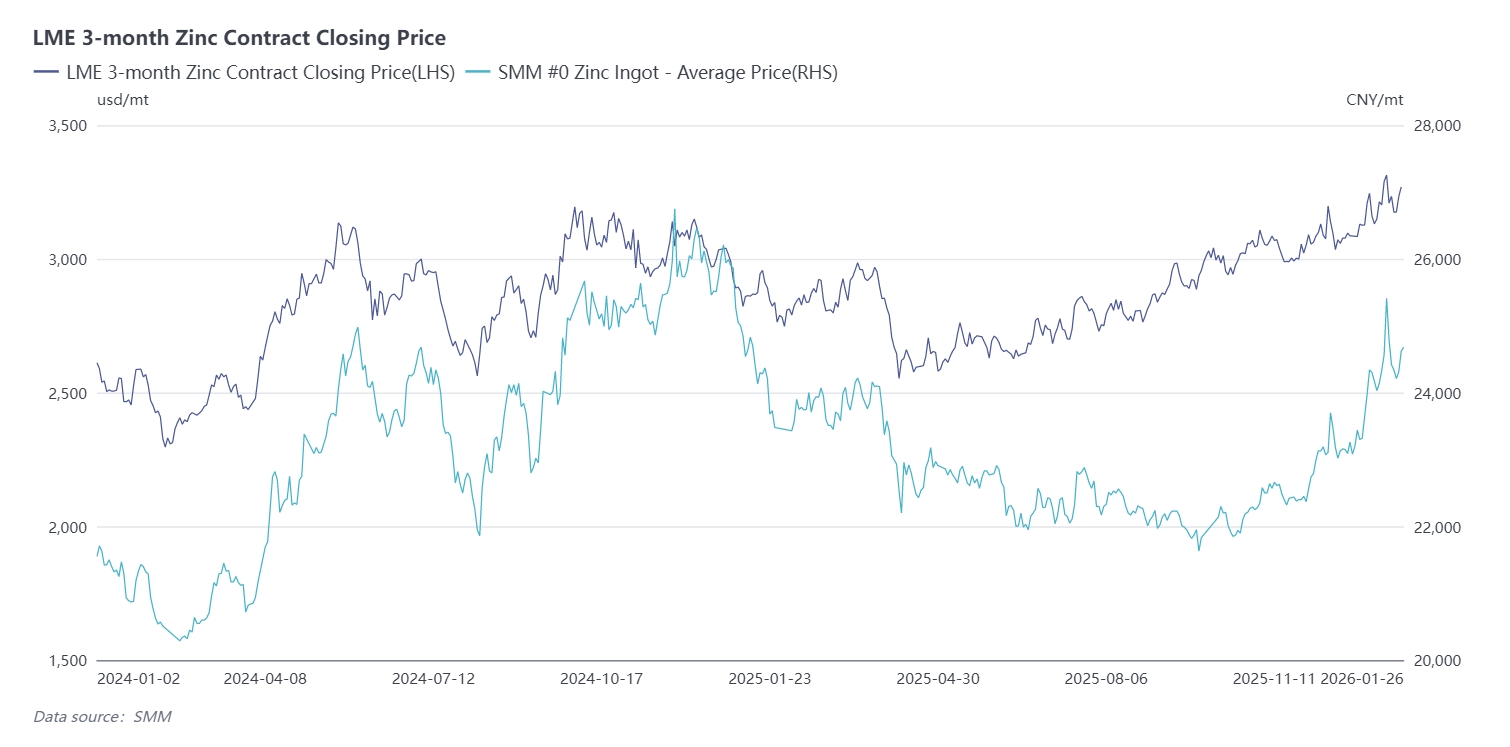

First, let's review last year's trend: Although zinc was positioned as a short play in 2025, it still managed to hold above 23,000 yuan/mt. This period can be divided into several stages:

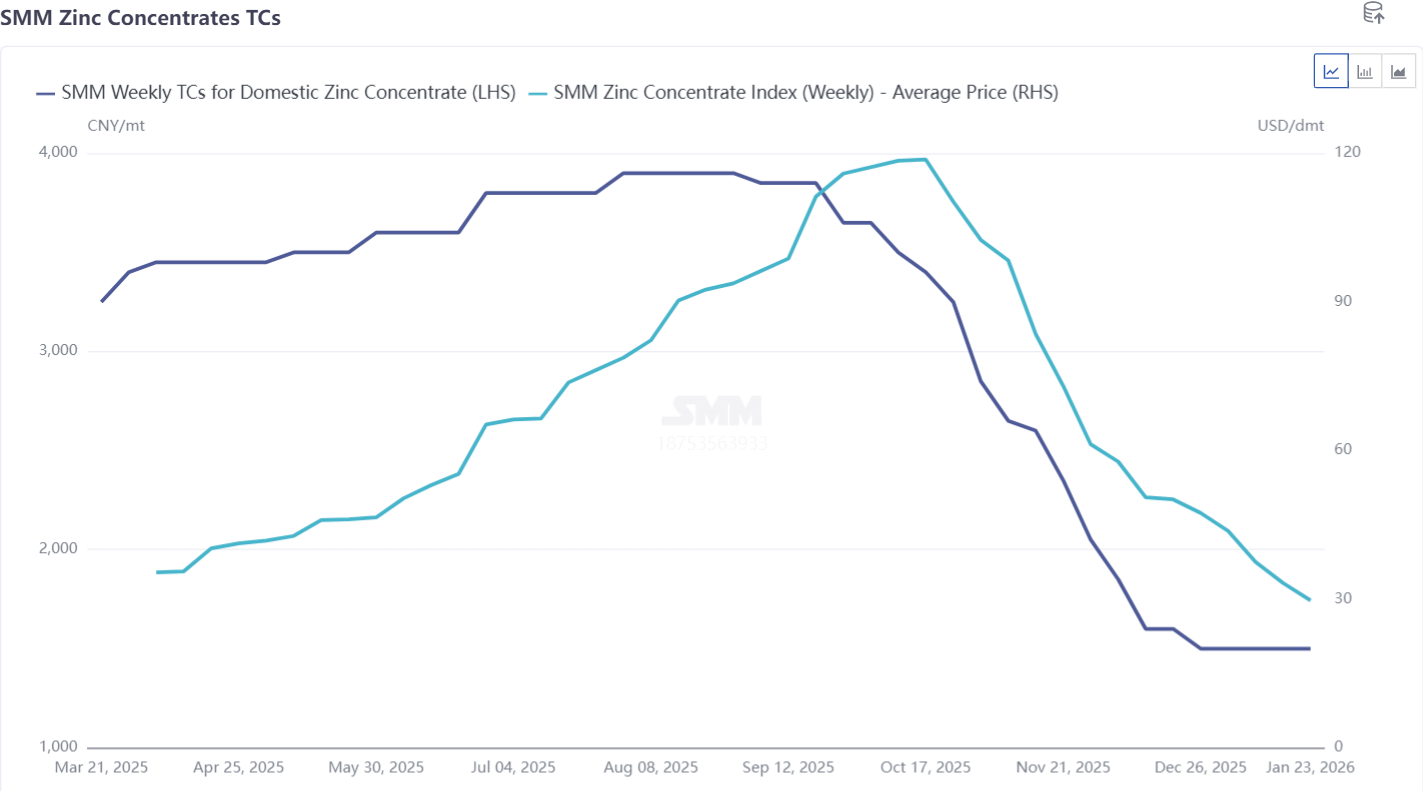

In H1, the market traded on expectations of a zinc concentrate surplus. Domestic processing fees rebounded from 1,600 yuan/mt in metal content to over 3,500 yuan/mt in metal content, and import processing fees rose from -40 $/dmt to above 60 $/dmt. Zinc prices fell steadily from nearly 25,000 yuan/mt at the start of the year, exacerbated by the US increasing tariffs, leading to an accelerated decline to around 21,000 yuan/mt. The overall market sentiment was consistent, with bears dominating and pessimistic price outlooks.

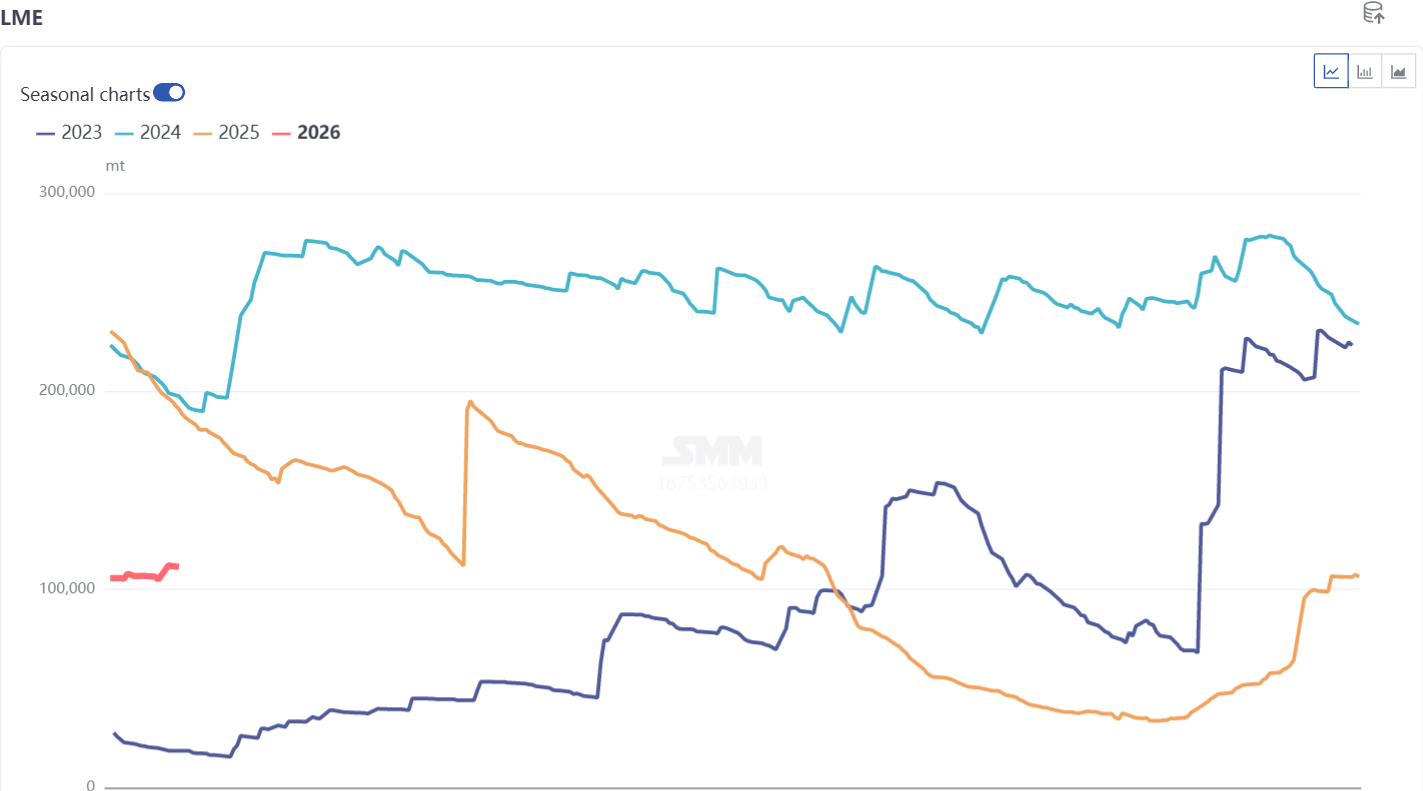

In Q3, as processing fees stopped falling and began to rebound, new capacities at domestic smelters were gradually released, and social inventory increased. However, against the backdrop of overseas interest rate cuts, LME inventory declined rapidly, and the center of zinc prices slightly shifted upward to around 22,000 yuan/mt.

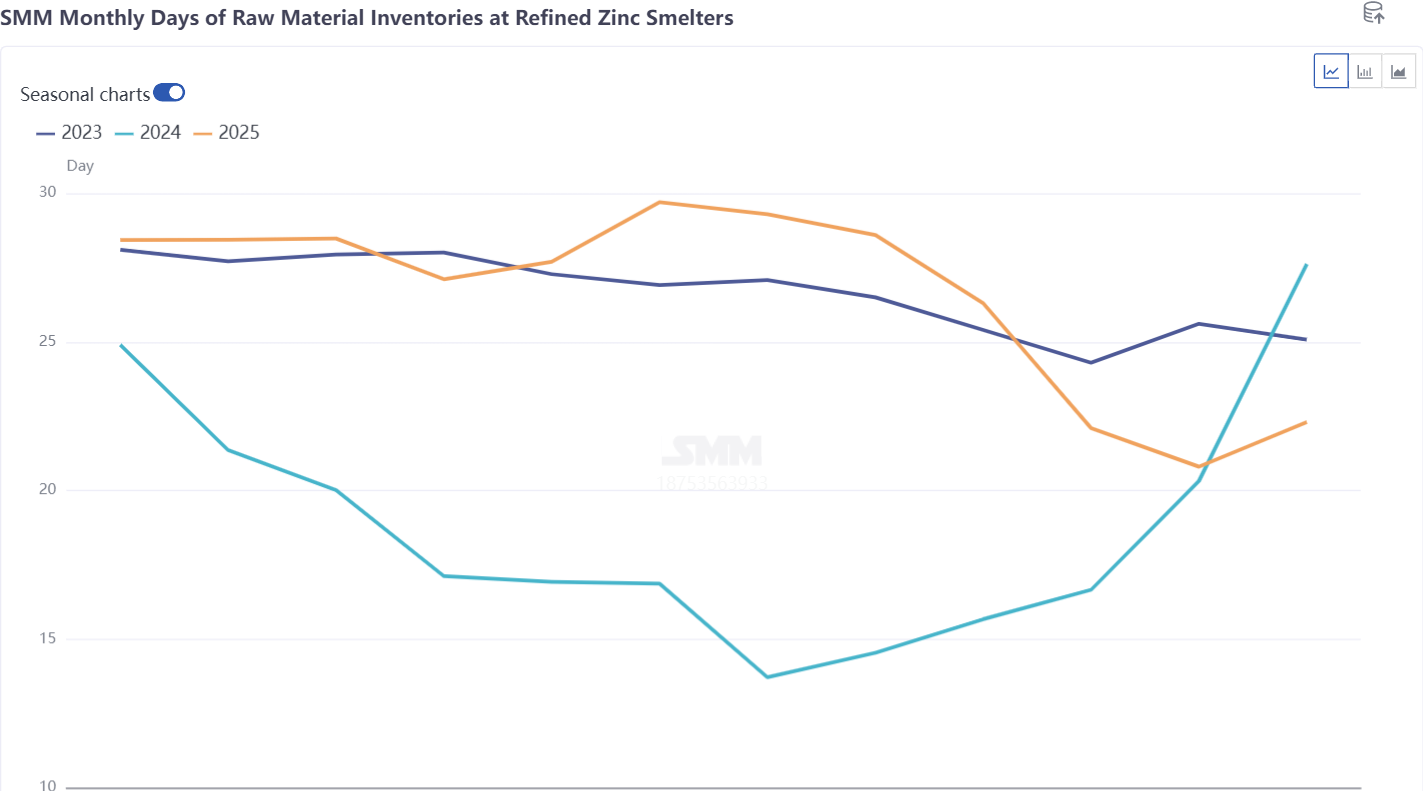

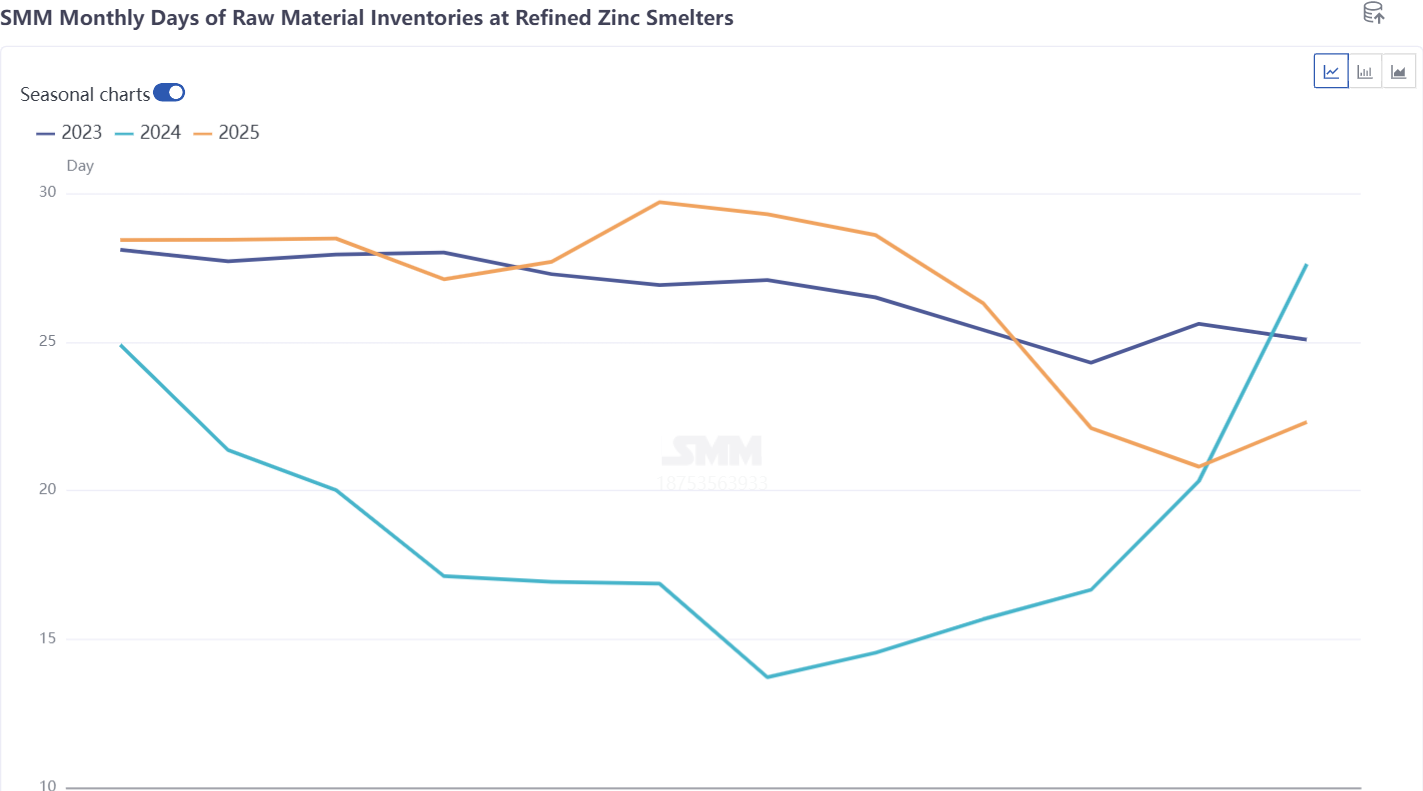

Entering Q4, LME inventory dropped to about 10kt, and LME Cash-3M backwardation surged to over $300/mt. Overseas structural risks escalated, pulling LME prices strongly back above $3,000/mt. For the first time since 2022, the export window for domestic zinc ingots reopened, leading to a phased transfer of domestic zinc ingots overseas. Simultaneously, the import window for zinc concentrates closed, and both domestic and import processing fees plummeted. The logic of ore surplus collapsed, and smelter raw material inventories decreased to around 20 days, pushing zinc prices above 23,000 yuan/mt.

Entering 2026, zinc prices followed the macro sentiment and the high spirits of surrounding metals, rising to over 25,500 yuan/mt at their peak, significantly exceeding market expectations. Besides macro factors, what fundamental aspects of zinc should be watched?

1. With low smelter raw material inventories and continued downward pressure on import processing fees, will production cuts expand?2. The game between smelter production cuts and low TC levels, the timing of a rebound in TC, and the situation regarding BM negotiations.

3. The surge in overseas natural gas prices and its impact on European smelter production.

4. Disruptions to mine production due to floods in Australia, internal conflicts in the DRC, extreme weather overseas, and geopolitical factors.

5. The buildup in social inventory during the Chinese New Year period, as well as the recovery in smelter production and downstream consumption after the holiday.