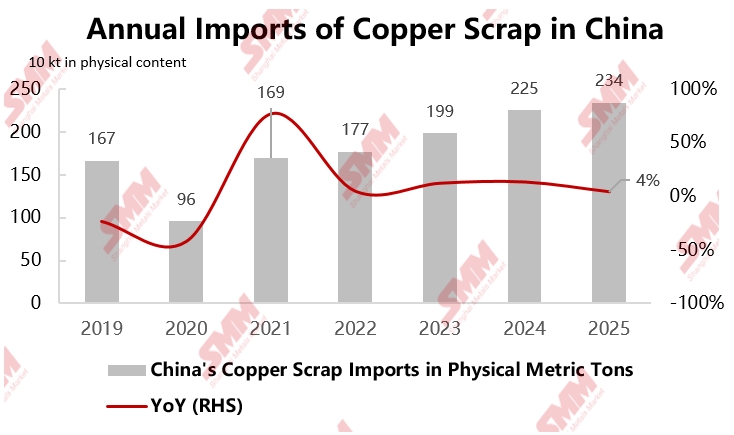

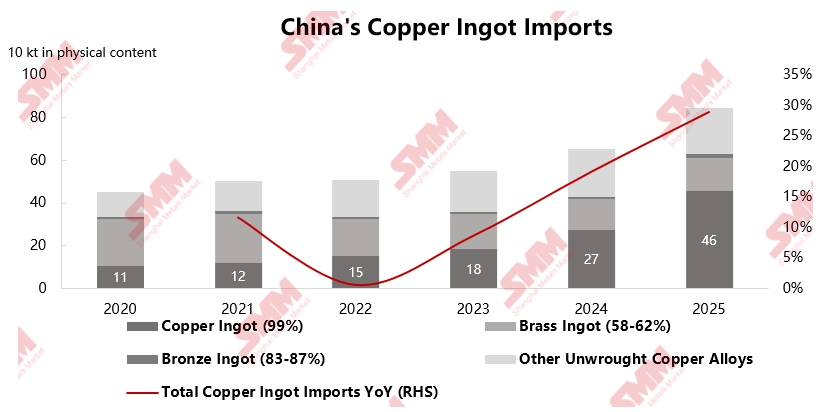

According to SMM statistics, China's copper scrap imports reached 2.3427 million mt in physical content in 2025, up 4.1% YoY. Among copper ingot imports, copper ingot imports stood out significantly, reaching 459,000 mt in physical content, up 67.6% YoY. Against the backdrop of domestic copper cathode capacity expansion and persistent copper concentrate supply tightness, copper scrap has become an indispensable raw material supplement for the smelting sector. Due to limited growth in domestic supply, both the copper processing and smelting sectors have rigid demand for overseas raw materials.

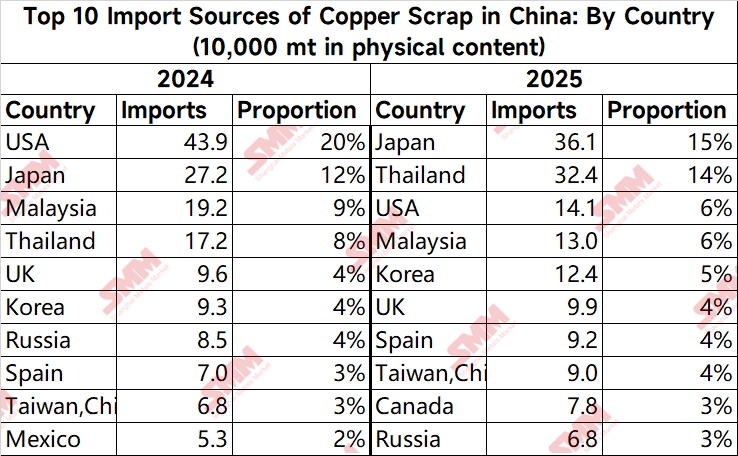

From the perspective of copper scrap import sources, the landscape changed significantly in 2025 compared to 2024. Japan surpassed the US to become China's largest source of copper scrap imports, with imports reaching 361,300 mt in physical content. Thailand's import volume also exceeded that of Malaysia, reaching 324,300 mt in physical content. In contrast, Malaysia saw its domestic dismantling and smelting operations shrink due to unprecedentedly strict new regulations on copper scrap imports implemented by its customs authorities starting in 2025, which particularly intensified the crackdown on solid waste and sheathed wire and cable. This led to a substantial shift of industrial activities to Thailand, causing China's imports from Malaysia to drop 32% YoY to 129,600 mt in physical content. Regarding the US, affected by the escalation of Sino-US trade friction after May 2025, China imposed an additional 10% import tariff on US goods, forcing many traders to abandon direct procurement from the US market and instead develop sources in Southeast Asia, Japan, and South Korea.

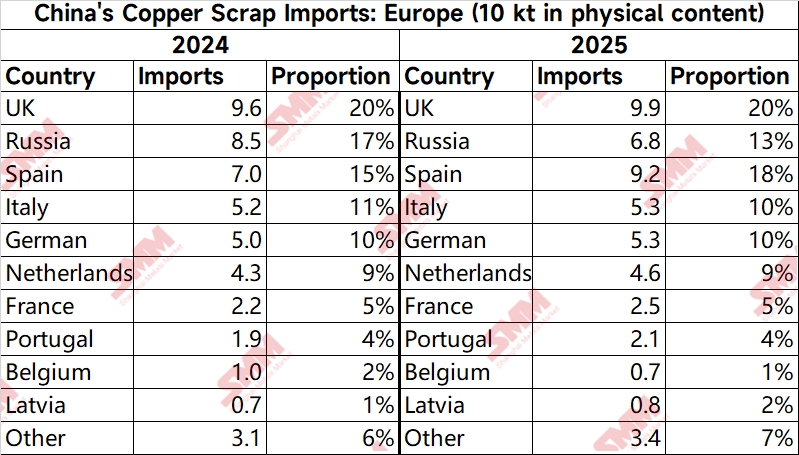

The European market, however, harbors uncertainties. The European Union proposes to establish thresholds for exports of "critical recycled raw materials" (such as copper scrap and aluminum scrap) to non-OECD countries starting in 2027, prioritizing domestic recycling needs and potentially implementing export quotas. As a result, Europe's exports of copper scrap are expected to contract in the future.

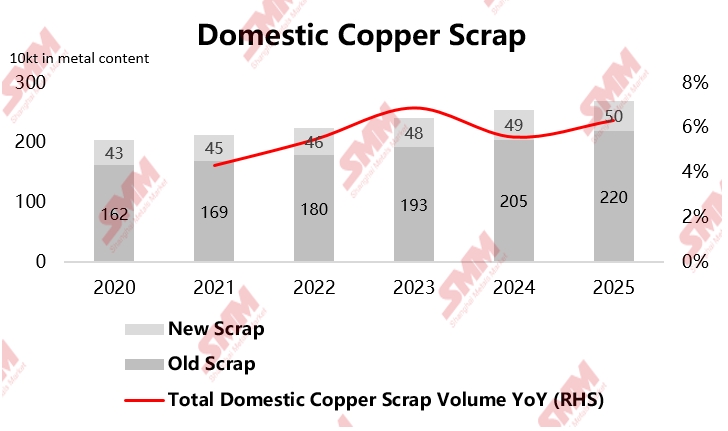

Domestically, in terms of supply, driven by policies such as home appliance subsidies and vehicle trade-in programs, as well as high copper prices, a large volume of retired products entered the recycling system at an accelerated pace. In 2025, domestic production of old scrap reached 2.202 million mt in metal content, while new scrap production stood at 500,800 mt in metal content. Domestic recycling volume achieved steady growth, with total domestic secondary copper raw materials amounting to 2.7 million mt in metal content, up 6% YoY.

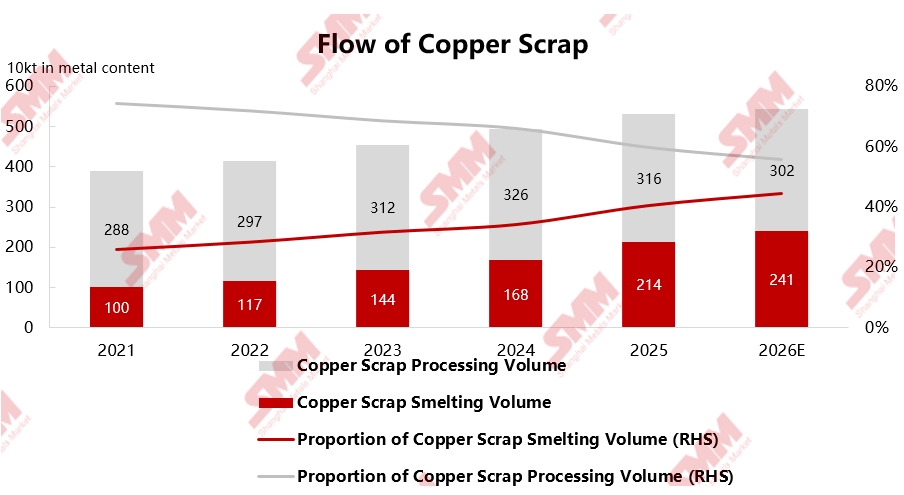

The consumption structure is also undergoing profound transformation, with the proportion of copper scrap flowing to the smelting end continuously increasing. According to SMM statistics, China's secondary copper smelting volume reached 2.14 million mt in metal content in 2025, accounting for 40.3% of total consumption; while processing volume decreased to 3.164 million mt in metal content, representing 59.7%. This change primarily stems from two major drivers: first, copper concentrate TCs have remained low or even negative for an extended period, compelling smelters to increase the use of scrap-generated anode plates to alleviate cost pressure; second, the implementation of the "reverse invoicing" policy and the introduction of "Notice No. 770," while beneficial for industry invoice standardization in the long term, have significantly increased the tax costs for small and medium-sized secondary copper processing enterprises in the short term, causing many enterprises to suspend production and adopt a wait-and-see approach towards the policies. Consequently, more raw materials have flowed to enterprises with long-term agreements and stable production of scrap-generated anode plates and smelting operations.

In summary, the supply-demand pattern of copper scrap in China is undergoing profound changes in 2025. Driven by both geopolitical factors and domestic industrial policies, the market is exhibiting new trends: diversification of import sources, strengthening of domestic recycling, and an increasing proportion of demand from the smelting sector. Traders are actively exploring emerging markets such as the Middle East, India, and Central Asia to reduce reliance on single sources. Meanwhile, policies like "reverse invoicing" are steering the industry away from disorderly price competition toward competition based on product quality and technology. From a macro perspective, amid expectations of long-term copper ore supply tightness, the strategic importance of copper scrap as a resource is becoming increasingly prominent. Domestic supply, incentivized by policies, is gradually building a healthier "internal circulation," while advancements in smelting technology have improved the processing efficiency of complex copper-containing scrap. Together, these developments provide strong support for ensuring the stability of China's copper cathode supply chain.

![China Copper Social Inventory Continues Destocking, Regional Trends Diverge Significantly [SMM Weekly Data]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)