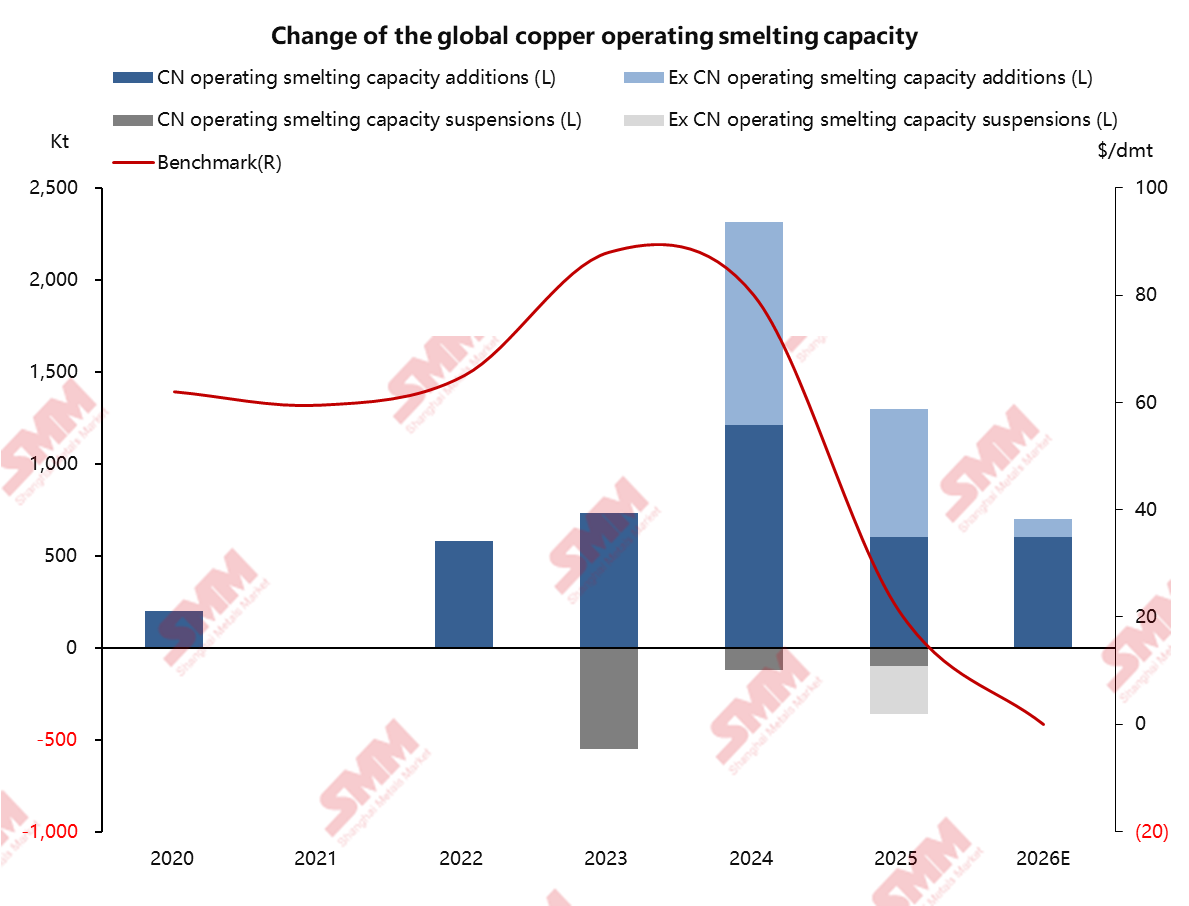

Since 2022, multiple copper smelting projects have been launched across Asian countries, notably China and Indonesia. This has directly led to a rapid increase in smelters' demand for cu cons, an imbalance in the global cu cons supply and demand balance, and a sharp decline in spot and long-term TC/RCs for cu cons.

The long-term benchmark pricing system for cu cons is facing significant pressure. Except for Antofagasta, long-term contract negotiations with other major suppliers are becoming increasingly fragmented. Currently, the annual benchmark is still based on the agreement reached between Antofagasta and Chinese smelters, but its market influence is gradually weakening. This stems from two factors: the tightening supply of cu cons, prompting more suppliers to pursue higher profits by departing from the benchmark system and adopting individualized pricing; and Antofagasta's annual direct sales of cu cons to China amounting to only about 500,000 dmt, diminishing its representativeness and bargaining power accordingly. According to SMM research, current supplier offers to domestic smelters take various forms: first, fixed TC/RC long-term contracts, mostly within the range of -50 to -60 USD/dmt; second, contracts referencing a third-party index average price with a deduction of 10-15 USD/dmt; third, a gradual shift towards spot sales, with some suppliers explicitly stating they will not sign new long-term contracts starting in 2026; fourth, contracts directly discounting the benchmark by 15%-20% or deducting 10-20 USD/dmt. Notably, the proportion of long-term contracts settled using indexed pricing and spot transactions has risen significantly, a trend actively promoted by major suppliers for their own benefit. Furthermore, recent reports from foreign media indicate that Japan's PPC has agreed on a long-term price of $25 per ton with raw material suppliers for 2026. However, according to SMM, this price actually represents the rollover of the long-term offtake position for 2025 between Japan's PPC and its affiliate—Caserones Minera Canada Limited, which holds a 49% stake in the Caserones copper mine under Lundin Mining. Its market reference value is limited and cannot be compared to the benchmark results achieved by Chinese smelters through centralized negotiations. Furthermore, PPC did not sign any new long-term contracts for 2026.

China is breaking through the dilemma of homogeneous competition with a high-quality development strategy, leading to tightening constraints on new capacity. Against this backdrop, domestic potential copper smelting projects face significantly greater approval and implementation difficulties, and the scale of new capacity shows a contracting trend. In active response to policy direction, several planned projects have adjusted their construction timelines. For example, new projects by Hubei Qiangxing, Hunan Yueneng, expansion projects by Xinjiang Wuxin and Yuguang Jinqian, and the third-phase project of Guangxi Nanguo have all been postponed. As the growth rate of domestic smelting capacity slows, the global cu cons supply-demand structure is expected to continuously optimize, driving a gradual recovery in cu cons TC/RC.

Major copper-producing countries overseas are accelerating supply chain localization through new smelting capacity. This is both a strategic move to enhance economic autonomy and industrial added value, and a reflection of the intensifying global strategic competition for critical mineral resources like copper. Since 2024, a new wave of global copper smelting capacity expansion has surged. Major projects such as Indonesia's Manyar smelter, PT Amman smelter, the Democratic Republic of the Congo's Kamoa-Kakula smelter, and India's Adani smelter have successively commenced or begun operation, signaling that major overseas copper producers are accelerating the localization and integration of their supply chains. This trend reflects countries' multifaceted considerations—enhancing economic autonomy, extending industrial value chains, and stabilizing domestic employment and livelihoods—actively transforming resource endowments into sustainable industrial competitiveness. On a deeper level, this represents not just physical capacity growth but also mirrors the intensifying global competition for strategic control over critical mineral resources. Countries are strengthening the smelting segment to gain greater autonomy over the copper supply chain, preparing for the long-term demand outlook for copper in the energy transition, and thereby securing a more favorable position in the global green economy competition.

![Diverging African Supply: June China Copper Anode Imports Recover, Q3 Maintenance May Weigh on Imports [SMM Analysis]](https://imgqn.smm.cn/usercenter/Bwtty20251217171714.jpeg)

![Copper Prices Continue to Rise, Copper Scrap Suppliers Actively Selling [SMM Secondary Copper Daily Review]](https://imgqn.smm.cn/usercenter/EFLYr20251217171714.jpeg)