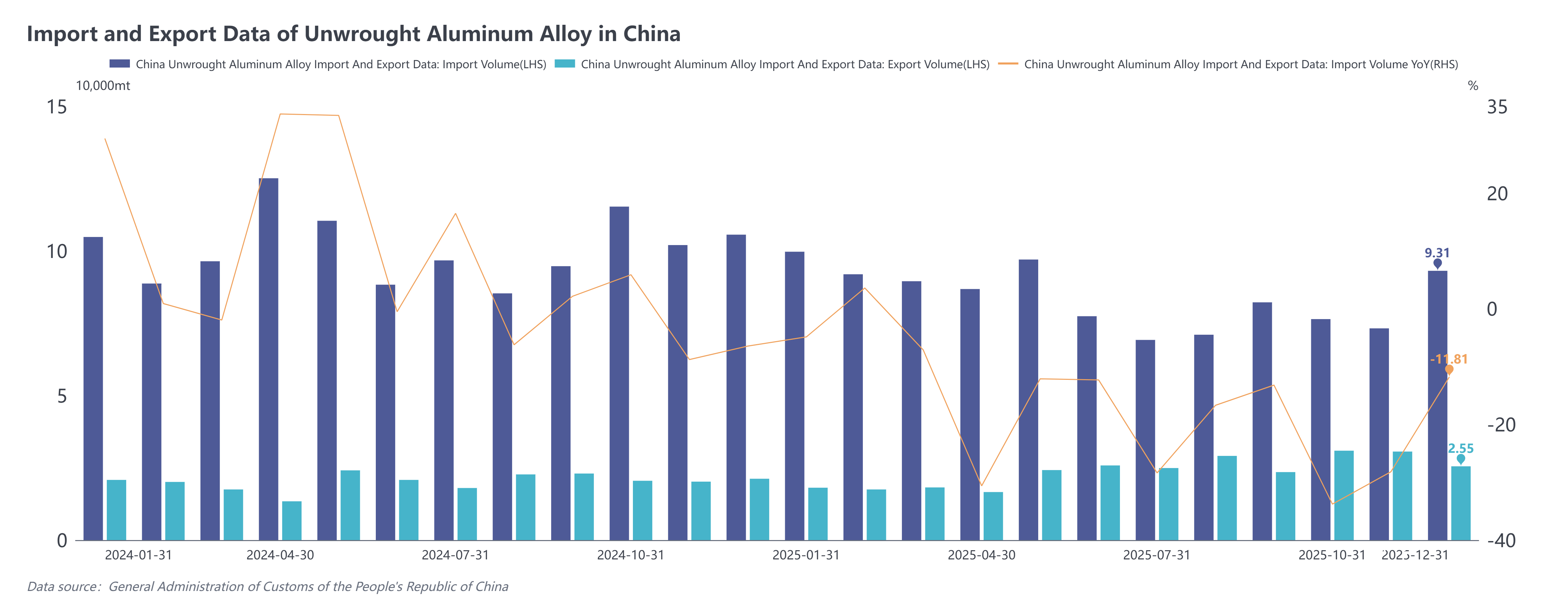

The General Administration of Customs recently released import and export data for December 2025. Customs data showed that:

In December 2025, unwrought aluminum alloy imports were 93,100 mt, down 11.8% YoY, but up 27.2% MoM. Cumulative imports for the full year of 2025 reached 1.0084 million mt, down 16.9% YoY.

In December 2025, unwrought aluminum alloy exports were 25,500 mt, up 20.0% YoY, but down 16.8% MoM. Cumulative exports for the full year of 2025 totaled 284,700 mt, up 17.5% YoY.

Total imports for the full year of 2025 decreased by 203,900 mt YoY. Imports from major suppliers generally declined: although imports from Malaysia fell by 164,600 mt to 356,700 mt, it remained the top supplier; Thailand, Vietnam, South Korea, and Pakistan also saw reductions ranging from 14,100 to 46,100 mt. In contrast, imports from Russia surged, increasing by 131,600 mt to 225,400 mt YoY, moving up from fourth place in 2024 to second. In terms of trade characteristics, imports from Russia were mainly through Processing Trade with Imported Materials (accounting for 39%), focusing on aluminum alloy slabs such as 3003 and 5052; in terms of flow, about 79% of the goods entered Henan, effectively supplementing the production needs of local sheet and strip enterprises.

In 2025, the top five provinces for China's unwrought aluminum alloy imports were Zhejiang (415,800 mt, 41%), Shandong (129,200 mt, 13%), Henan (100,200 mt, 10%), Jiangsu (95,400 mt, 9%), and Guangdong (82,200 mt, 8%). Compared to 2024, the import landscape became more diversified: imports in Zhejiang, Guangdong, and Jiangsu decreased by 171,700, 91,800, and 21,500 mt respectively; while Shandong and Henan saw significant increases, adding 63,700 and 59,300 mt respectively, rising to the second and third positions in the industry.

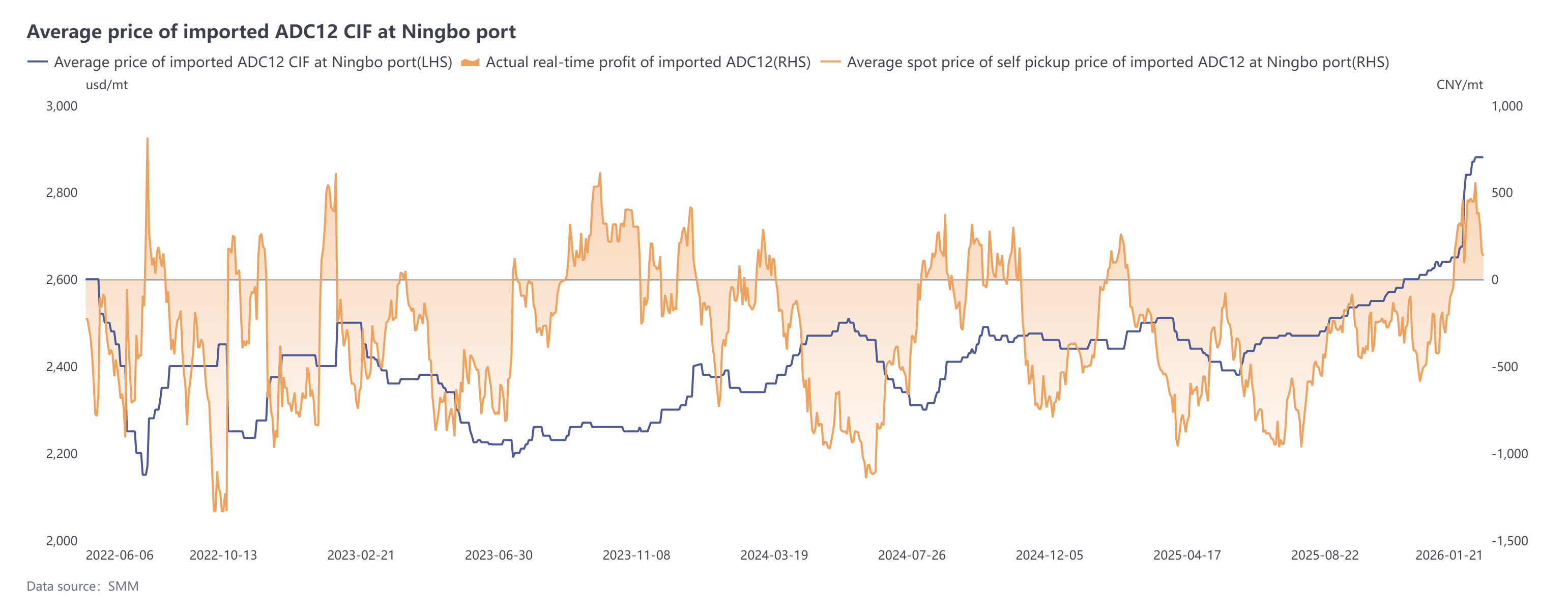

Overall, in 2025, China's unwrought aluminum alloys showed a trend of shrinking imports and growing exports. Annual imports decreased by 16.9% YoY to 1.0084 million mt; exports increased by 17.5%, reaching 284,700 mt. The weak import performance was mainly due to two factors: first, the persistent inversion of the price spread between domestic and overseas aluminum alloys throughout the year, weakening the import advantage and closing the profit window; second, the tight supply of aluminum scrap or recovering demand in Japan, South Korea, and India, which pushed up regional alloy ingot prices, leading to a significant reduction in resources flowing into China. From late December 2025 to January 2026, domestic ADC12 prices rose sharply in line with aluminum prices, reaching their highest level since October 2021. Although overseas prices also climbed rapidly to above $2,850/mt, the increase was smaller than that in the domestic market. The immediate import profit/loss shifted from a deficit to above the break-even point, theoretically reopening the import window. Imports in January 2026 were projected to range between 80,000–100,000 mt.