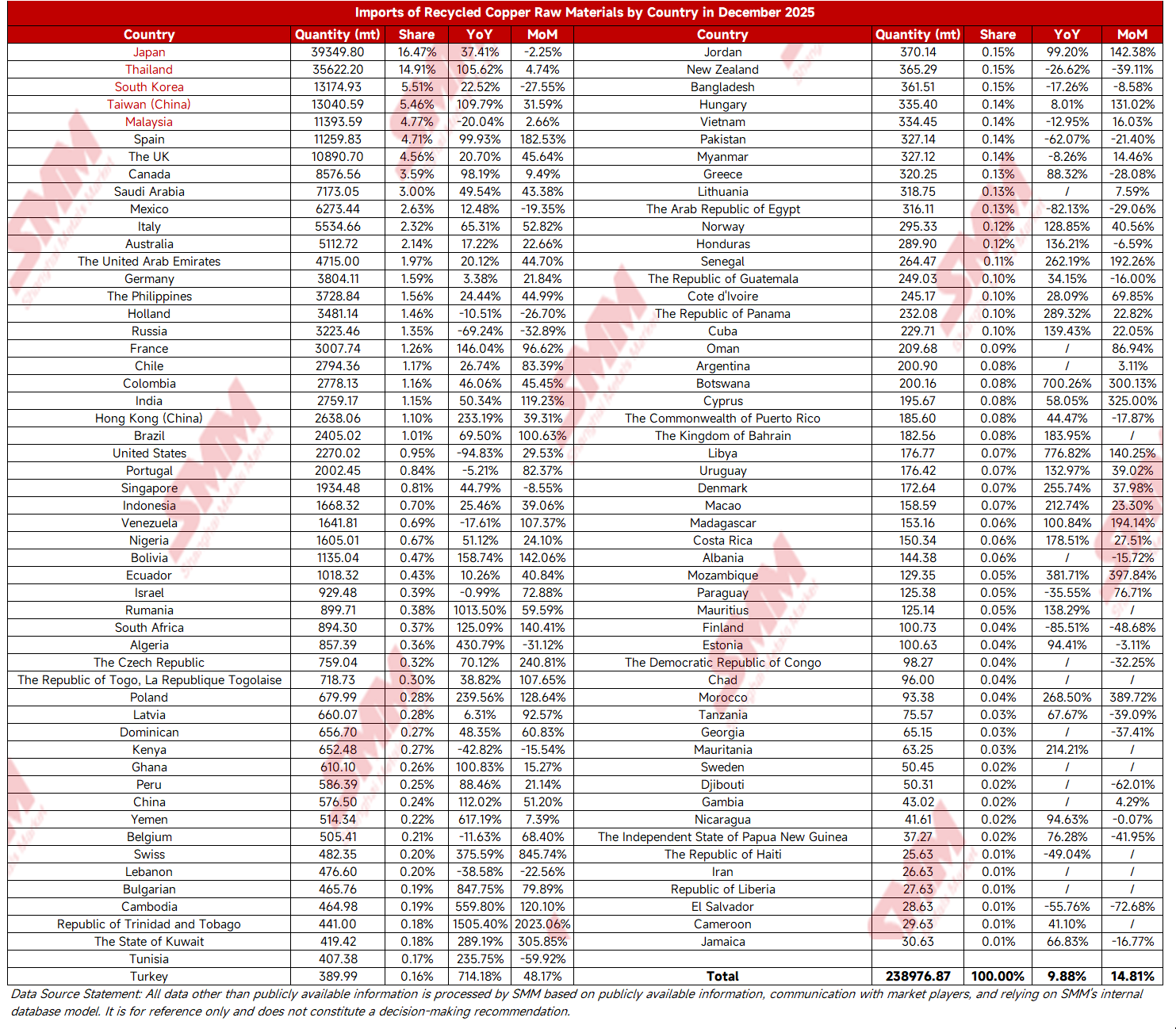

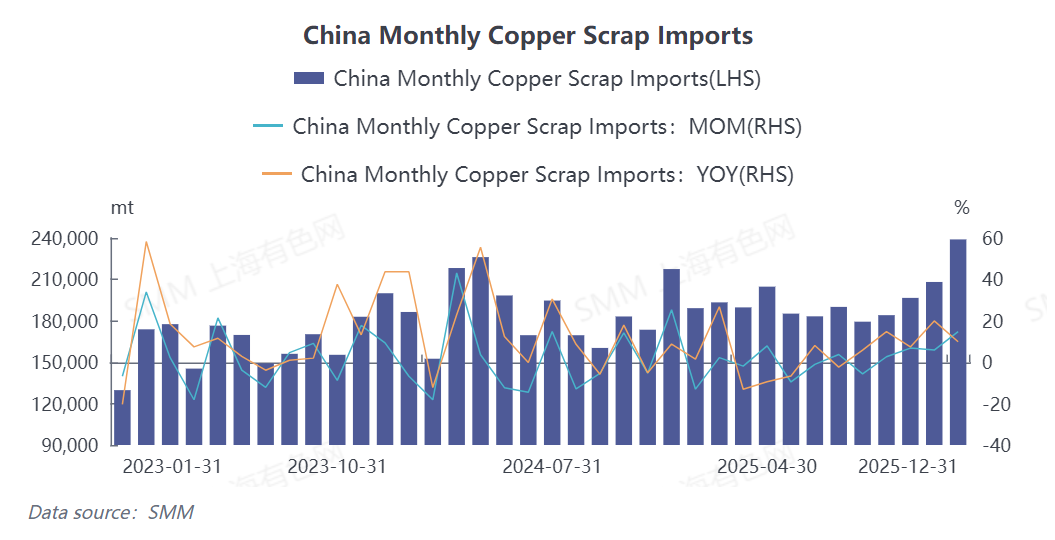

The latest data from the General Administration of Customs shows that in December 2025, China imported 239,000 mt in physical content of copper scrap and shredded copper scrap, up 14.81% MoM and 9.88% YoY. For the full year of 2025, cumulative imports reached 2.3427 million mt in physical content, up 4.12% YoY. China's secondary copper raw material imports maintained an overall stable and positive development trend amid a complex international economic and trade environment. (HS code: 74040000)

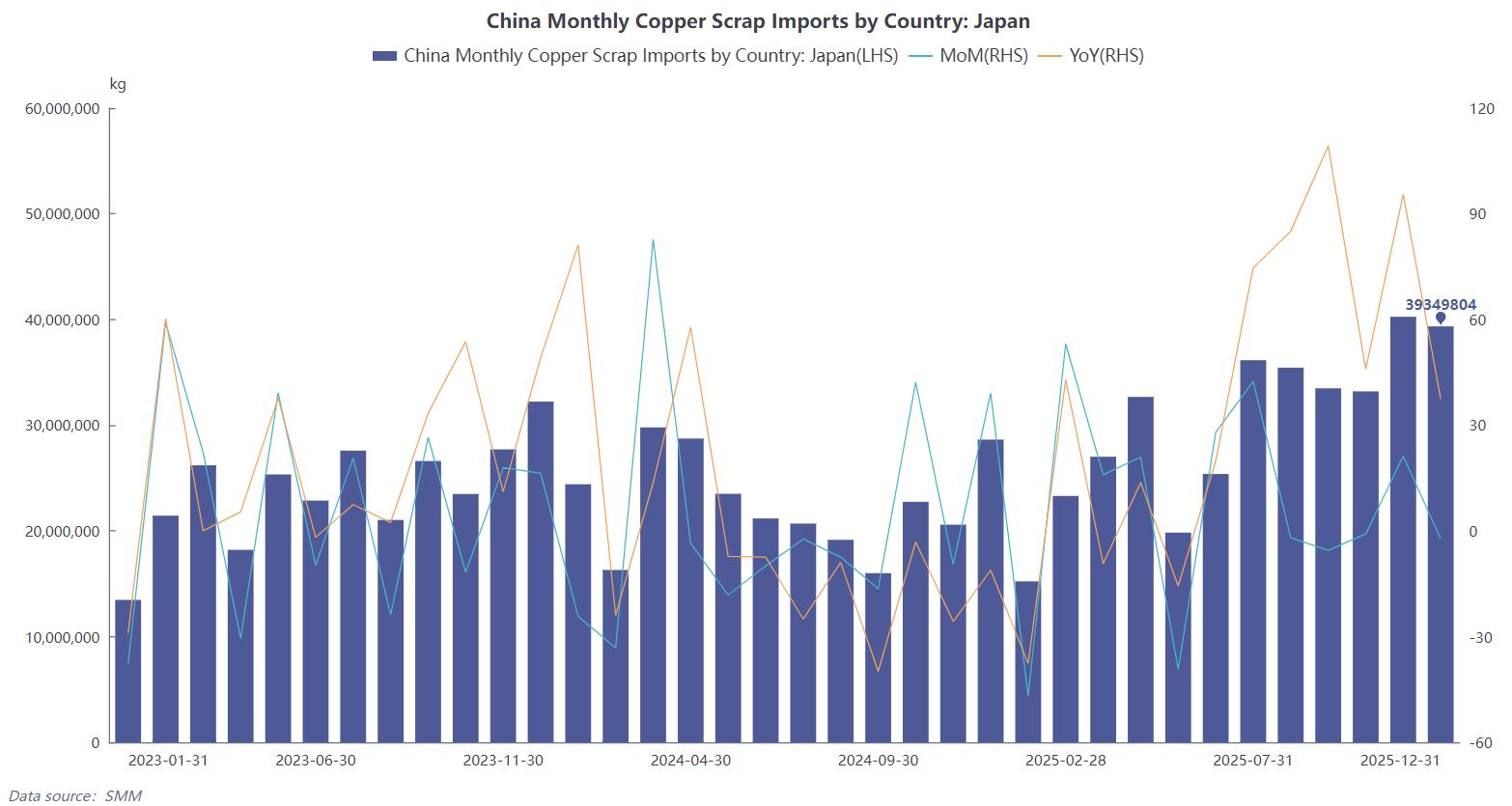

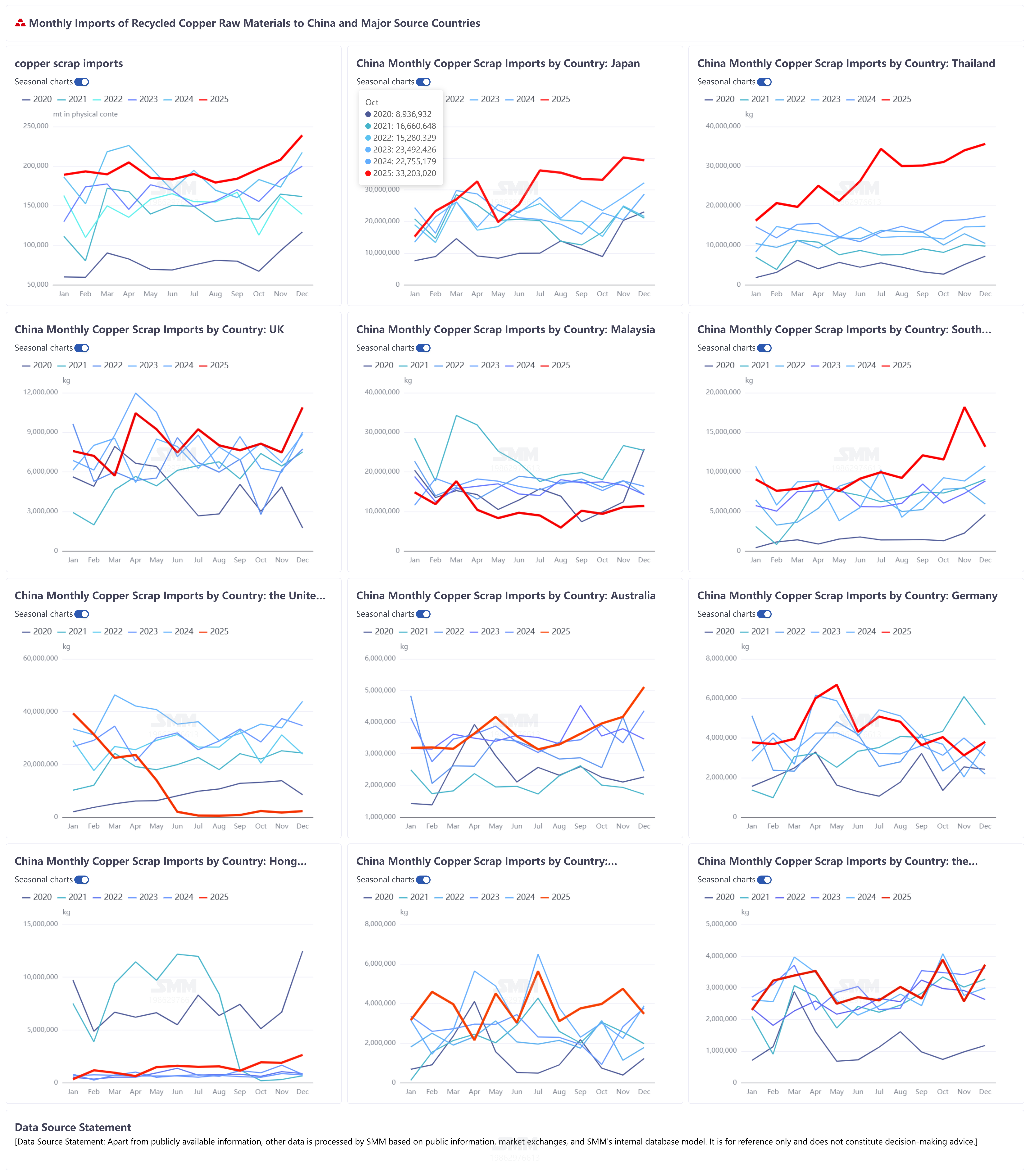

Analysis of the supply structure reveals a distinct characteristic of "one dominant player and multiple strong contributors with diversified sources": Japan, as the long-term stable largest supplier, exported 39,300 mt to China in December. Although this represented a slight decrease of 2.25% MoM, it showed a significant increase of 37.41% YoY, accounting for 16.47% of total imports, indicating a solid core position. Thailand, as the second-largest source country, performed particularly strongly, with December imports reaching 35,600 mt in physical content (14.91% share), up 4.74% MoM and surging 105.62% YoY, demonstrating strong growth potential and the increasing importance of regional supply chains. South Korea ranked third, with December imports of 13,200 mt in physical content (5.51% share). Although these fell 27.55% MoM, they still maintained a 22.52% increase YoY.

Furthermore, Malaysia, Taiwan, China, Spain, the UK, and others are also important suppliers, collectively forming a widely distributed and diversified supply system. Meanwhile, the US, once a major source, has seen its share of supply to the Chinese market shrink drastically. December imports were merely 2,270.02 mt, with the share dropping to 0.95%. Although this was an increase of 29.53% MoM, it represented a sharp decline of 94.83% YoY. The market share vacated by the US has been comprehensively and rapidly filled by the aforementioned Asian and European countries, leading to a regional reshaping of global secondary copper raw material trade flows.

Overall, China's secondary copper raw material imports maintained growth resilience in terms of total volume in 2025, underpinned by the rigid demand for recycled metals driven by domestic green, low-carbon, circular economic development. The profound evolution of the supply structure, particularly the rapid rise in share from surrounding Asian countries (such as Thailand and Malaysia) and stable input from European sources, highlights the effectiveness of China's strategy to optimize import origins. This has reduced reliance risks from single markets and enhanced supply chain resilience and security. Driven by the "dual carbon" goals and resource recycling policies, domestic demand for secondary copper will persist in the long term. Imports are expected to remain at a certain scale, but growth rates may become more stable, with increased focus on synergistic development with the domestic recycling system. (The following appendix contains import data for secondary copper raw materials for December 2025)

Overall, China's secondary copper raw material imports maintained growth resilience in terms of total volume in 2025, underpinned by the rigid demand for recycled metals driven by domestic green, low-carbon, circular economic development. The profound evolution of the supply structure, particularly the rapid rise in share from surrounding Asian countries (such as Thailand and Malaysia) and stable input from European sources, highlights the effectiveness of China's strategy to optimize import origins. This has reduced reliance risks from single markets and enhanced supply chain resilience and security. Driven by the "dual carbon" goals and resource recycling policies, domestic demand for secondary copper will persist in the long term. Imports are expected to remain at a certain scale, but growth rates may become more stable, with increased focus on synergistic development with the domestic recycling system. (The following appendix contains import data for secondary copper raw materials for December 2025)