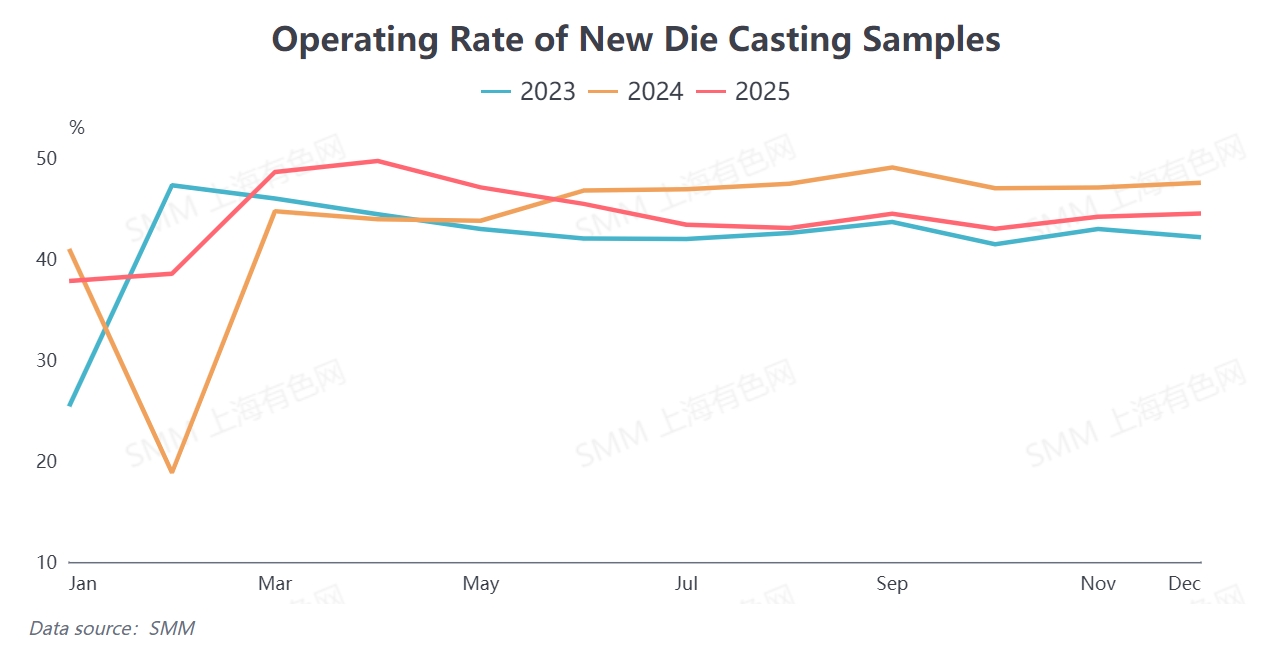

According to SMM data, the average annual operating rate of domestic die-casting zinc alloy in 2025 was 44.16%, up 0.48 percentage points YoY. The full-year operating rate showed a divergent trend of "rising sharply in H1 and pulling back in H2." The slight increase in the operating rate in 2025 was mainly driven by the export rush amid expectations of Sino-US tariffs in H1, coupled with the traditional peak season effect of "Golden March and Silver April," which led to a phased increase in industry operating rates. However, the decline in industry prosperity in H2 also introduced multiple variables for market development in 2026.

Reviewing end-use consumption of die-casting zinc alloy in China in 2025, the core downstream sectors exhibited a characteristic of "policy support but diverging demand." In the real estate sector, despite continuous implementation and strengthening of domestic policies to stabilize the property market, demand for building hardware fittings—a key application of die-casting zinc alloy—showed mediocre performance, with the industry still in a phase of digesting existing demand. In the automotive sector, favorable policies such as the "trade-in" policy effectively boosted a recovery in auto market consumption. However, amid the lightweight trend of NEVs, the usage of zinc alloy per vehicle was limited, providing insufficient support for the expansion of alloy demand. Meanwhile, in 2025, domestic smelters continued to release die-casting zinc alloy capacity. The price spreads between zinc and aluminum, and between zinc and copper, experienced wild swings along with commodity prices. Private die-casting zinc alloy enterprises faced dual pressures from low-priced alloy impacts and high raw material costs, leading to a prominent trend of "commercialized" operations. The operating rate continued to decline from H2, becoming a major drag on the industry's development throughout the year.

Looking ahead to 2026, the domestic die-casting zinc alloy core downstream end-use market is expected to remain generally stable, with policy support continuing to be the main driver on the demand side. In the real estate sector, the intensity and precision of policies aimed at stabilizing the property market will further improve in 2026. While the overarching direction remains "prioritizing stability," marginal improvements following policy implementation are expected to underpin demand for architectural hardware components. In the home appliance hardware segment, the dual policy incentives of "trade-in + subsidies for new purchases" will continue to be released, helping to rebound home appliance production and sales, thereby driving demand for die-casting zinc alloy components. In the automotive sector, the ongoing implementation of the trade-in policy provides clear guidance for vehicle consumption. The replacement demand for traditional internal combustion engine vehicles and the supporting demand for new energy vehicles complement each other, supporting zinc alloy consumption in the automotive field. Overall, the three major downstream consumption segments, which account for a significant proportion of die-casting zinc alloy demand, face no substantial downside risks on the demand side in 2026, and the industry's consumption foundation remains stable.

The main risks are as follows.

From the perspective of enterprise costs and market competition, the prices of basic raw materials such as zinc, aluminum, and copper in China rose significantly at the beginning of 2026. Die-casting zinc alloy enterprises continued to raise processing fees to pass on cost pressures, directly driving up the procurement costs of end-user hardware enterprises. This led to weaker purchasing enthusiasm downstream, making just-in-time procurement the mainstream in the market. At the same time, the gap in processing fees between private die-casting zinc alloy enterprises and smelters persists. Against the backdrop of high raw material prices, end-users have shown a significantly increased willingness to purchase low-priced zinc alloys to control costs. As a result, private die-casting zinc alloy enterprises face the risk of further market share erosion, and demand-side growth is expected to continue slowing down.

Furthermore, amid continuous capacity release, increased volatility in raw material prices, and sluggish growth in end-use demand, the contradiction between "low-price competition" and "high costs" in the die-casting zinc alloy industry is expected to become more pronounced. The operational pressure on small and medium-sized enterprises is at risk of intensification.

From the perspective of export trade, the US-China Busan meeting on October 30, 2025, agreed to suspend the implementation of relevant hefty tariffs on China until November 10, 2026. As die-casting zinc alloy and related products fall under the categories covered by the tariff suspension, exports to the US market in 2026 will enter a window of opportunity, providing incremental space for industry consumption. However, vigilance is also required against the uncertainty risks of tariff policies.

![Ningbo Zinc: Futures Zinc Price Rises Again, Traders Quote in a Buddha-Like Manner [SMM Midday Review]](https://imgqn.smm.cn/usercenter/tAyyp20251217171754.jpg)