SMM January 16 Update:

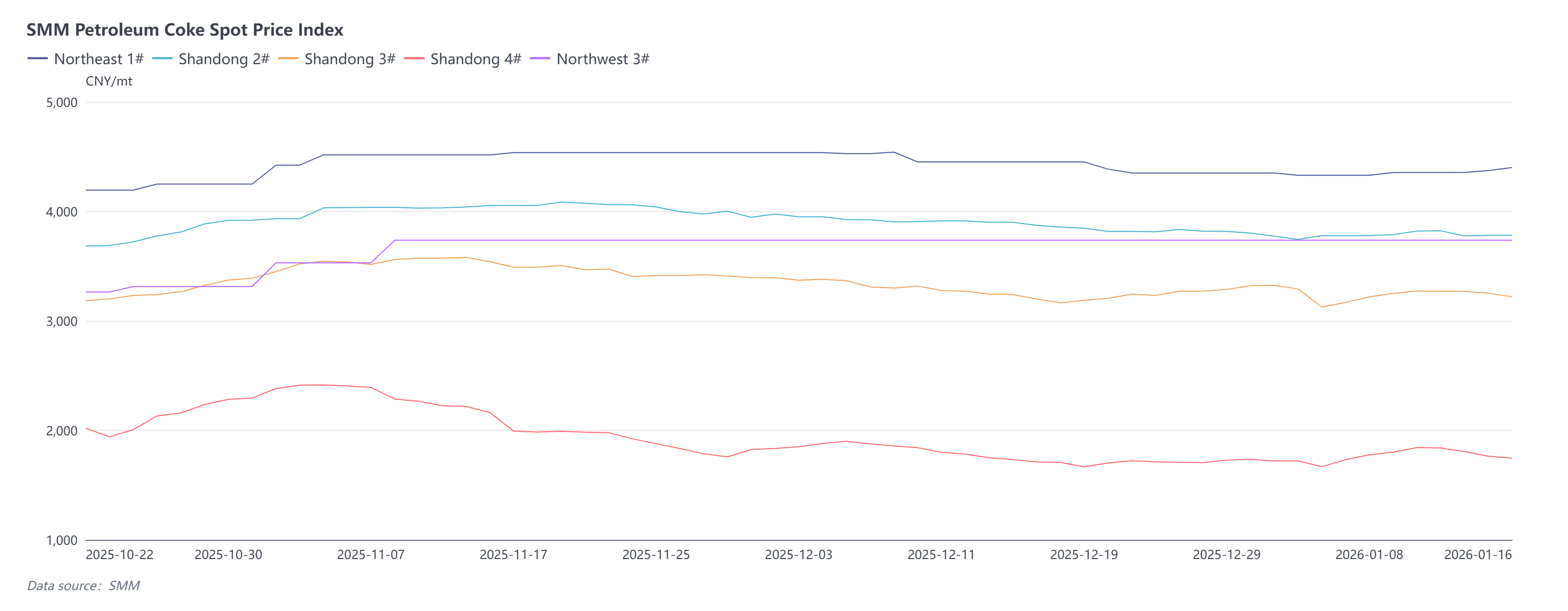

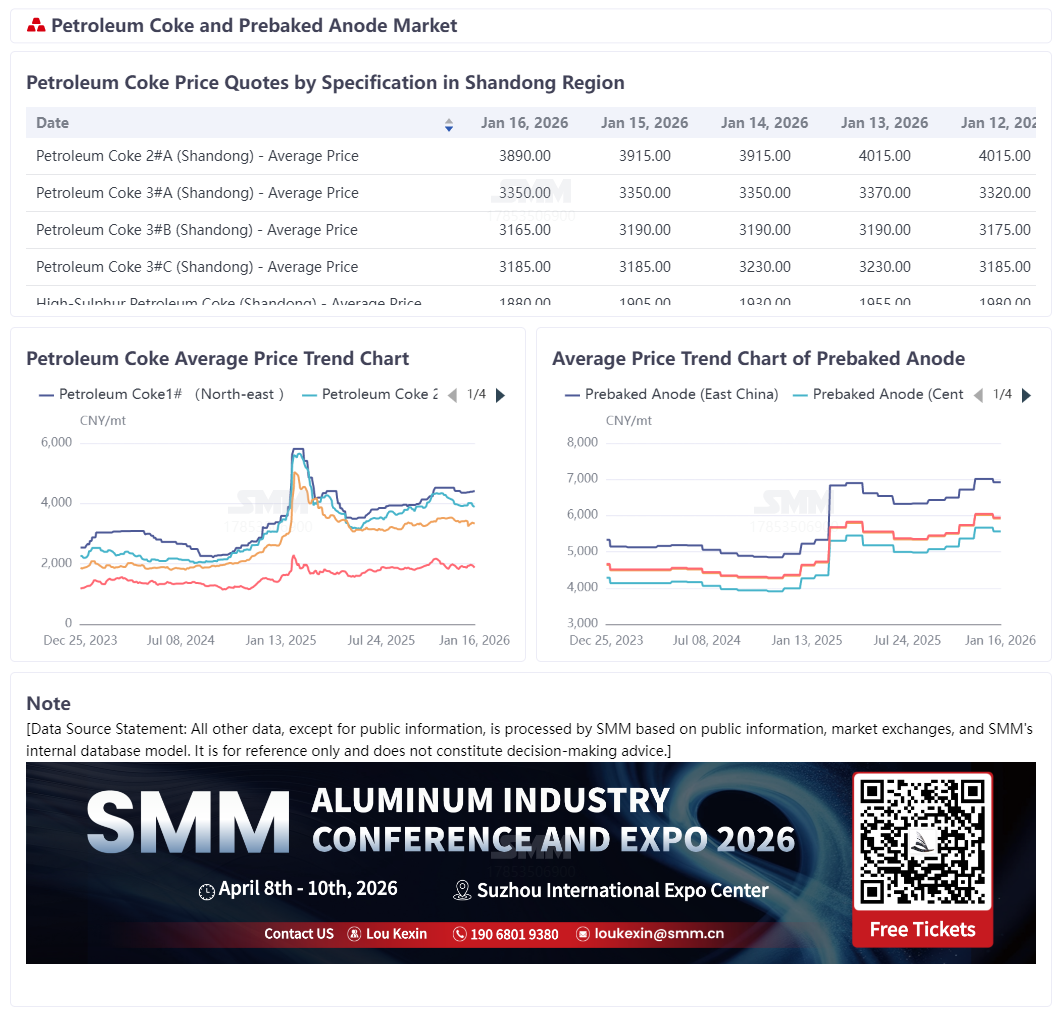

Recently, the trading atmosphere in the petroleum coke market has been moderate. Within the week, petroleum coke prices showed a trend of first rising then falling, with refinery shipments varying and price changes differing among various specifications. Specifically, this week, CNOOC-affiliated refineries' petroleum coke prices were largely stable. PetroChina's low-sulphur coke prices in north-east China increased slightly, currently ranging from 4046-4691 yuan/mt. SMM's spot price index for No.1 petroleum coke in north-east China was 4401.29 yuan/mt, up 1.04% WoW. In north-west China, medium-sulphur coke prices remained steady, with SMM's spot price index for No.3 petroleum coke at 3737.42 yuan/mt. Sinopec's refinery shipments were stable, with an overall moderate transaction atmosphere, mainly fulfilling orders, and petroleum coke prices were largely stable. Local refineries saw mixed shipment performance; within the week, refinery petroleum coke prices first rose then fell, with high-sulphur coke shipments under pressure in the latter half of the week, leading to a decline in high-sulphur petroleum coke prices. SMM's latest data shows that the spot price index for No.2 petroleum coke in Shandong was 3782.8 yuan/mt, down 0.16% WoW; the spot price index for No.3 petroleum coke in Shandong was 3220.3 yuan/mt, down 0.95% WoW; and the spot price index for No.4 petroleum coke in Shandong was 1746.16 yuan/mt, down 3.06% WoW.

This week, the imported petroleum coke market had a moderate trading atmosphere, with port spot prices showing a clear divergence. By category, the low-sulphur coke market performed relatively strongly, with prices generally stable and increasing slightly. The medium-to-high sulphur coke market, although maintaining a steady shipping pace, was affected by the continuous decline in domestic high-sulphur coke prices in the latter half of the week, resulting in port spot prices remaining in a consolidation phase, with some varieties seeing a slight weakening in transaction prices. Inventory-wise, petroleum coke inventory at Shandong ports increased slightly this week, mainly due to the arrival and unloading of a Saudi import cargo during the week. Supply side, petroleum coke supply pulled back this week compared to earlier periods, mainly due to ongoing maintenance at Yangzi Petrochemical and Anqing Petrochemical, simultaneous coke cleaning operations at Zhejiang Petrochemical, no new production resumptions during the period, coupled with some refineries making minor output adjustments as needed, dragging down overall petroleum coke production. Looking ahead, both Zhejiang Petrochemical and Yangzi Petrochemical are expected to resume production next week, and domestic petroleum coke supply is expected to gradually rebound.

Demand side, significant structural divergence was observed. In the latter half of the week, overall downstream buying sentiment weakened, purchasing behavior returned to just-in-time procurement dominance, proactive restocking willingness cooled, and market trading atmosphere weakened, leading petroleum coke prices to consolidate overall. By sector, the core downstream carbon used in aluminum production showed regional divergence. Traditional major production regions such as Shandong, Henan, and Hebei continued to face pressure on enterprise operating rates due to persistent environmental protection-related controls. Meanwhile, new prebaked anode projects in energy-rich regions like Inner Mongolia and Yunnan successively commenced operation, with capacity gradually being released, effectively enhancing industry supply flexibility. This not only compensated for temporary production gaps caused by environmental protection-driven production restrictions and equipment maintenance in some regions but also supported the scale of just-in-time procurement for petroleum coke. However, overall market activity has currently declined, enterprise stockpiling support fell short of expectations, and mid and high-sulphur petroleum coke prices lacked sustained upward momentum. The anode materials industry maintained stable operations, with continuous release of just-in-time procurement demand for low-sulphur petroleum coke, becoming a key market support and driving firm low-sulphur coke price trends.

Overall, domestic petroleum coke market supply is expected to increase, while downstream demand performance is generally weak. Although pre-Chinese New Year stockpiling demand provides some market support, it is still difficult to alleviate the overall pressured pattern. In response, SMM expects the petroleum coke market to operate steadily overall next week, with prices for various categories continuing their divergent trends: low-sulphur coke prices are expected to remain firm, supported by pre-holiday stockpiling demand from the anode materials industry; mid and high-sulphur coke prices are expected to maintain stable operation, relying on just-in-time procurement from the carbon used in aluminum production industry.

![Aluminum Producers' Operating Rates Rebound to 61.9%; High Prices Challenge "Golden March" Peak Season [SMM Survey]](https://imgqn.smm.cn/usercenter/tXCfs20251217171653.jpg)

![ADC12 Prices Rose Again This Week[[Weekly Review of Aluminum Scrap and Secondary Aluminum]]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)