January 16, 2026

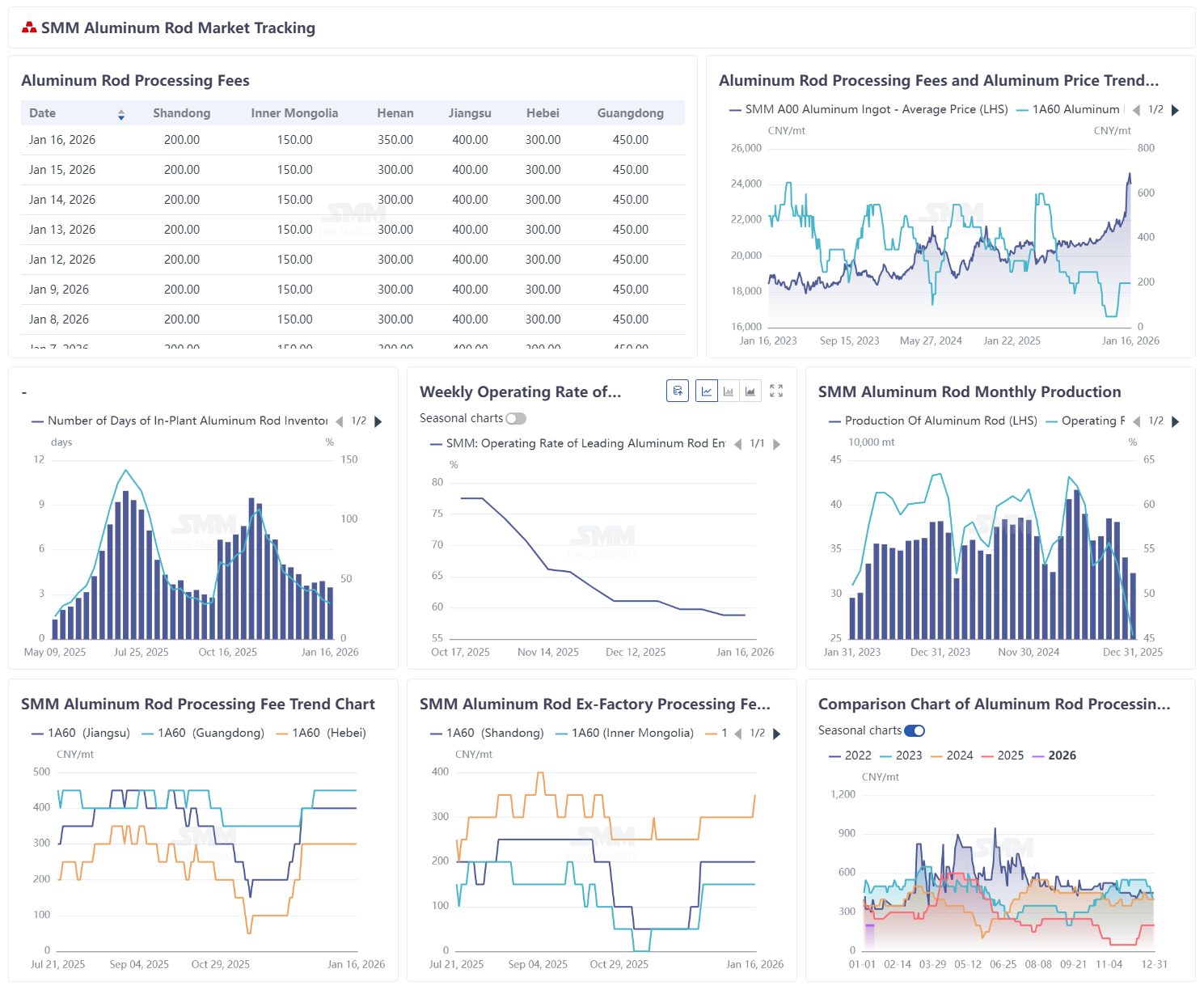

Reviewing the aluminum rod market in December, overall supply and demand improved, with processing fees bottoming out and returning to reasonable levels. According to SMM surveys, aluminum rod production totaled 323,800 mt in December, down 5.06% MoM. On the supply side, production in the aluminum rod industry continued to decline in December, mainly due to weak downstream demand, leading plants to control in-factory inventories while partially halting production lines for maintenance. Additionally, environmental protection-related controls in Henan disrupted continuous plant operations, insufficiently supporting operating rates. SMM believes that current aluminum rod processing fees have returned to reasonable levels, but downstream consumption lacks strong drivers, with purchases mainly for essential needs. Considering the approaching Chinese New Year, plants will manage inventory levels more rationally, production pace tends to slow down, and operating rates at aluminum rod plants are expected to continue declining in January.

According to SMM statistics, as of January 16, 2026, in-factory inventory days for domestic aluminum rod plants were 3.48 days, down 0.42 days MoM, with inventories continuing a weak downward trend. In terms of inventory ratio, the in-factory inventory ratio for domestic aluminum rod plants was 30.19%, down 2.96 percentage points WoW.

During the week, aluminum prices fluctuated at historical highs, and downstream fear of high prices persisted, but essential demand led to passive acceptance of high-priced aluminum rods. Regarding processing fees, as of January 16, 2026, offers for aluminum rod processing fees in Jiangsu were concentrated at 400-450 yuan/mt, in Hebei at 300-350 yuan/mt, and in South China at 300-500 yuan/mt. Processing fees returned to the following levels by region: Shandong at 150-250 yuan/mt, Inner Mongolia at 100-200 yuan/mt, and Henan at 300-400 yuan/mt.

This week, the operating rate for aluminum wire and cable remained stable without significant fluctuations. The main reason for the change was that enterprises focused on digesting backlog orders after the New Year holiday, and power grid order matching progressed orderly, alleviating short-term production pressure. Currently, the cancellation of tax rebates for PV modules has not affected cable demand, with limited short-term impact, but as overseas PV project installations materialize, overseas demand will gradually become apparent. Supported by subsequent orders, the operating rate is expected to see a slight recovery next week, but due to high aluminum prices and weak end-use demand, overall conditions will remain in the doldrums.