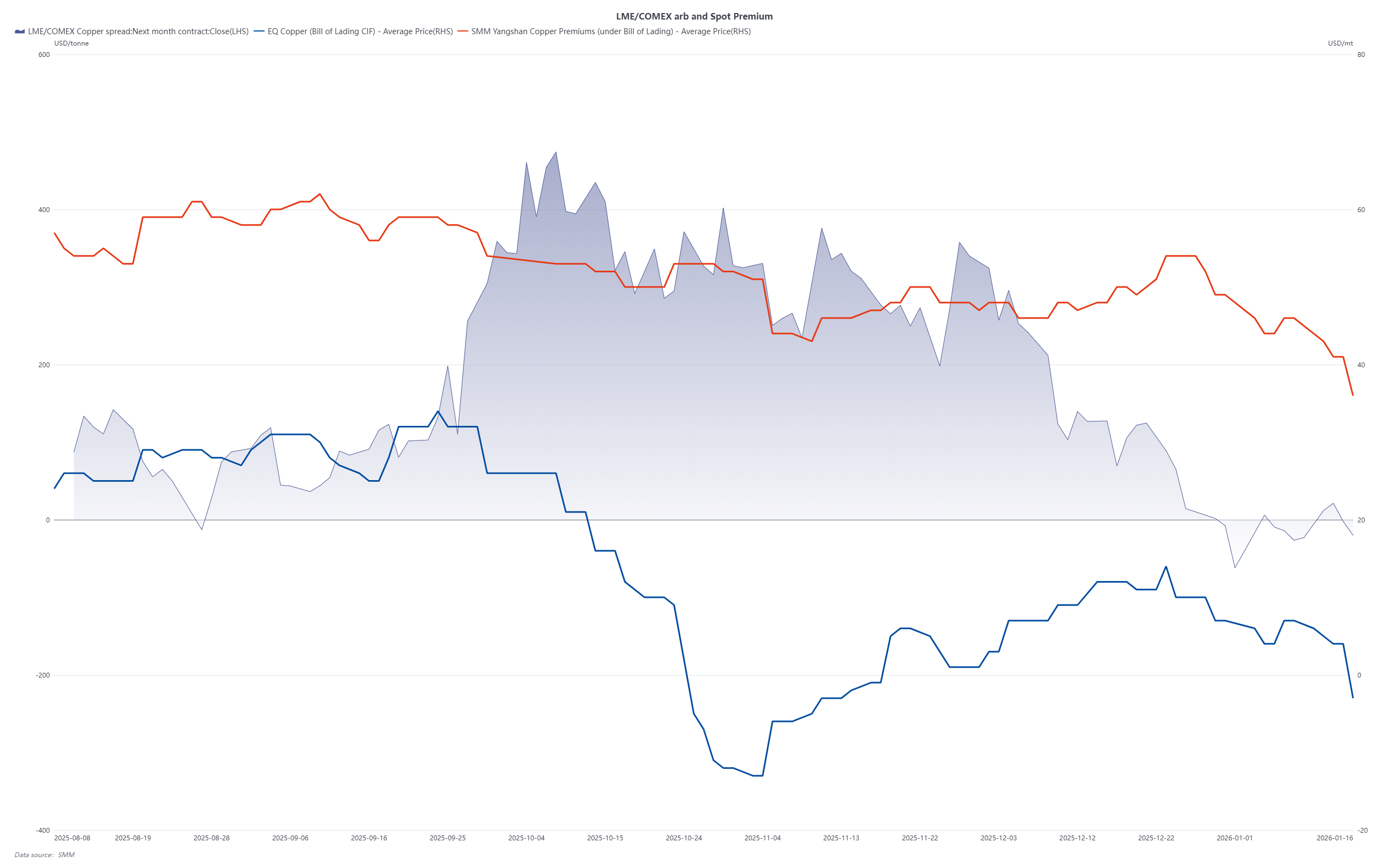

In early 2026, U.S. trade policy has once again become a key variable impacting the global copper market. On Wednesday, U.S. President Donald Trump publicly stated that he currently does not intend to impose tariffs on rare earths, lithium, and other critical minerals — including copper, which has been listed as a critical mineral since 2023. This statement quickly triggered a reassessment of U.S. copper import dynamics, leading to a narrowing of the LME-COMEX arbitrage spread.

The postponement of copper tariffs, combined with elevated domestic inventory levels in the U.S., is now placing pressure on copper prices. According to market estimates, the U.S. consumes around 1.6 million metric tons (Mt) of refined copper annually, while domestic production stands at roughly 900 kt. Exports remain around 150 kt per year, creating a structural deficit of approximately 850 kt. In 2025, total U.S. copper imports were close to 1.6 Mt — of which 850 kt covered the supply gap, while the remaining 750 kt served as replenishment or speculative inventory. Notably, an estimated 488.4kt is sitting in COMEX-registered warehouses (about 542,900 short tons), with an additional 280 kt believed to be held as unreported stock — a total inventory level approaching 800 kt.

More importantly, a number of long-term contracts signed in 2024–2025 for 2026 delivery — mostly COMEX-registered brands — were priced significantly higher than current spot valuations. With the arbitrage window narrowing, some of these cargoes are now being redirected to Asia. SMM has learned that in recent weeks, COMEX-branded warrants and shipping documents have been sold off at discounted prices in Chinese and Southeast Asian spot markets. Some traders have also expressed interest in re-negotiating semi-annual or quarterly long-term contracts for 2026, signaling a possible shift in trade flows.

As a result, net refined copper imports into China and Southeast Asia may not be as tight in Q1 2026 as previously expected. While competition for African and Indonesian-origin material remains strategically important, the potential return of U.S.-linked copper supply may partially offset the perceived supply risks. The regional copper market could therefore enter a more balanced — or even slightly oversupplied — phase in the early part of the year, marking a subtle shift from the tightness that dominated late 2025.