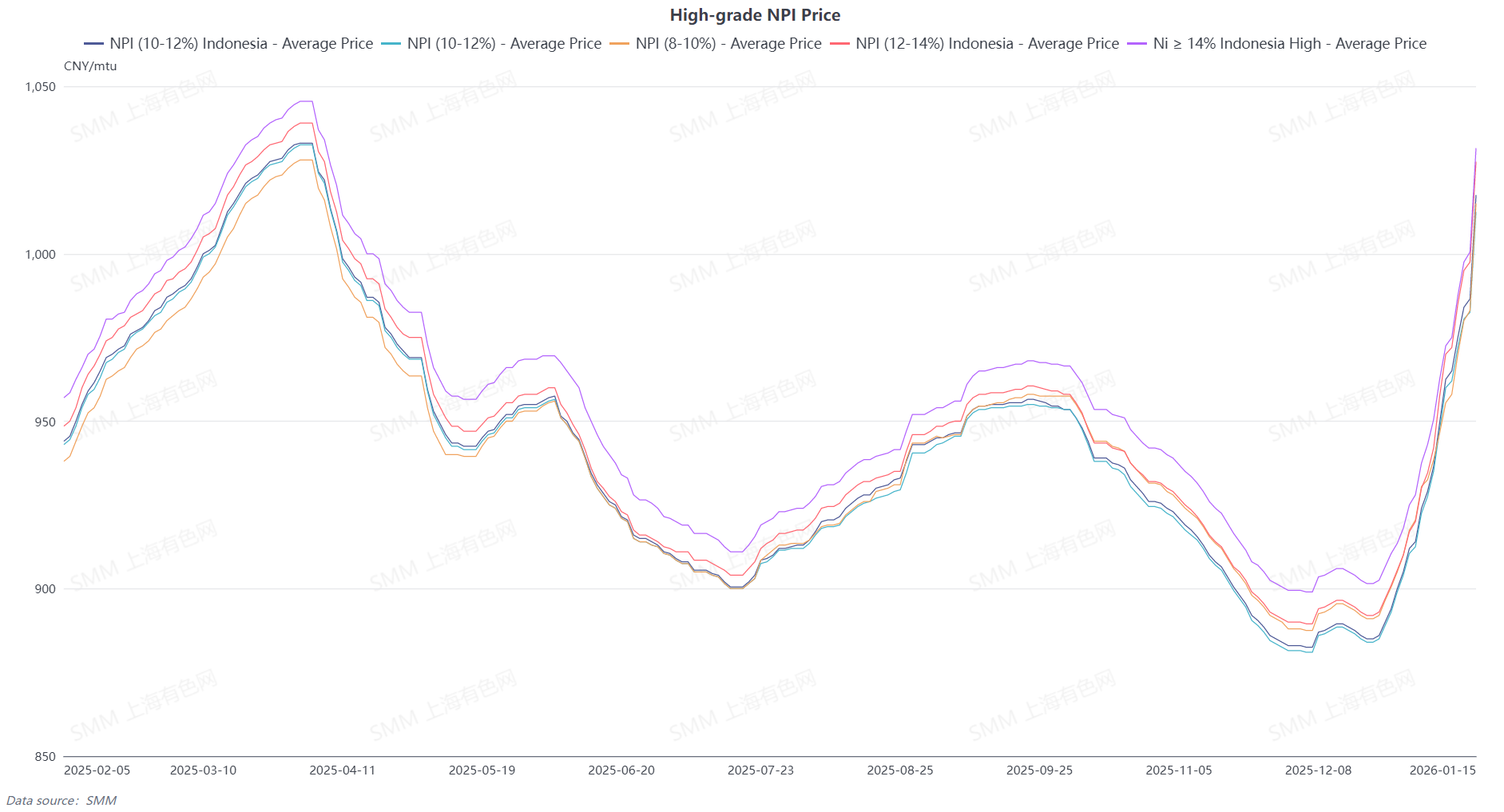

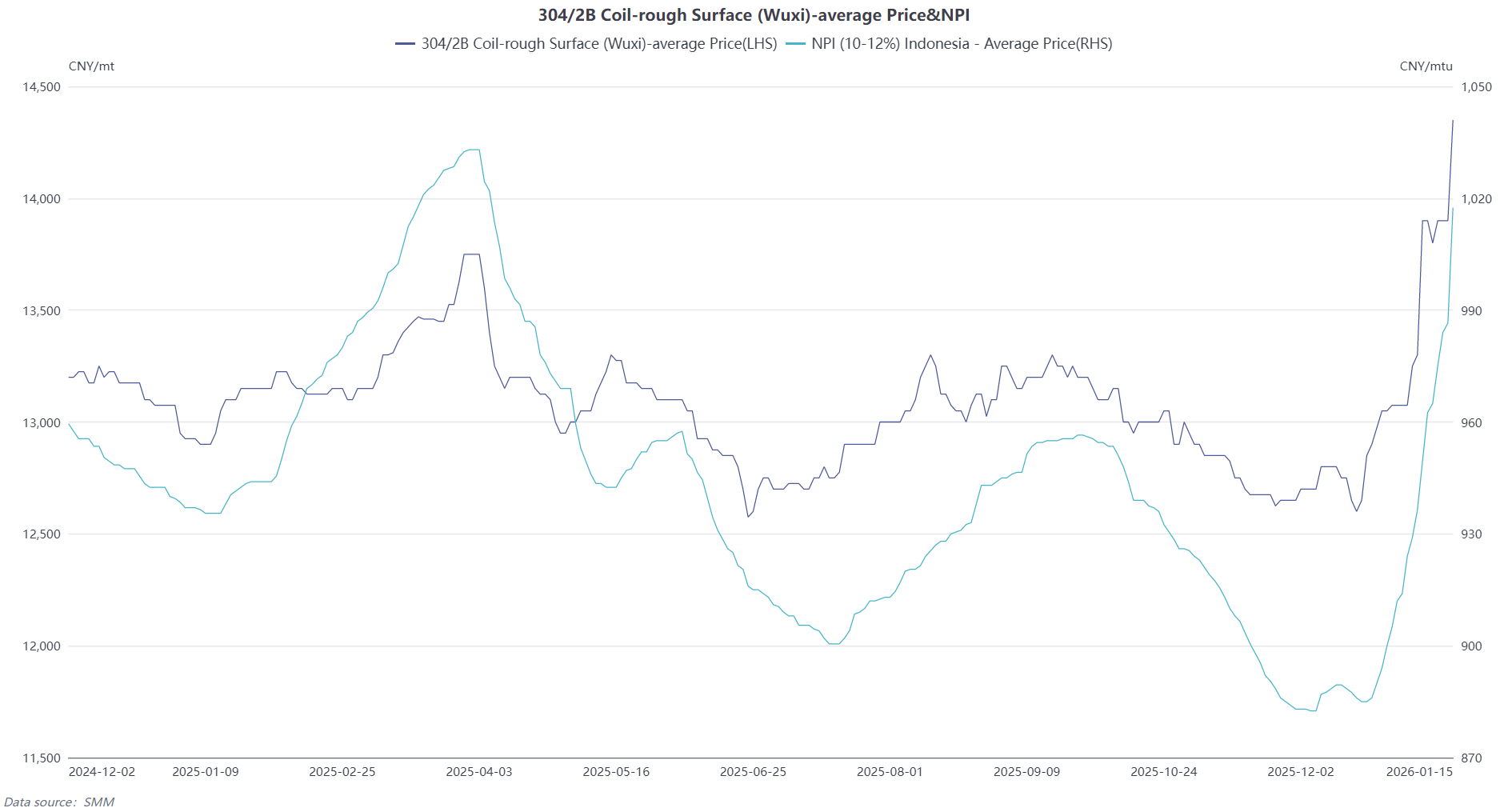

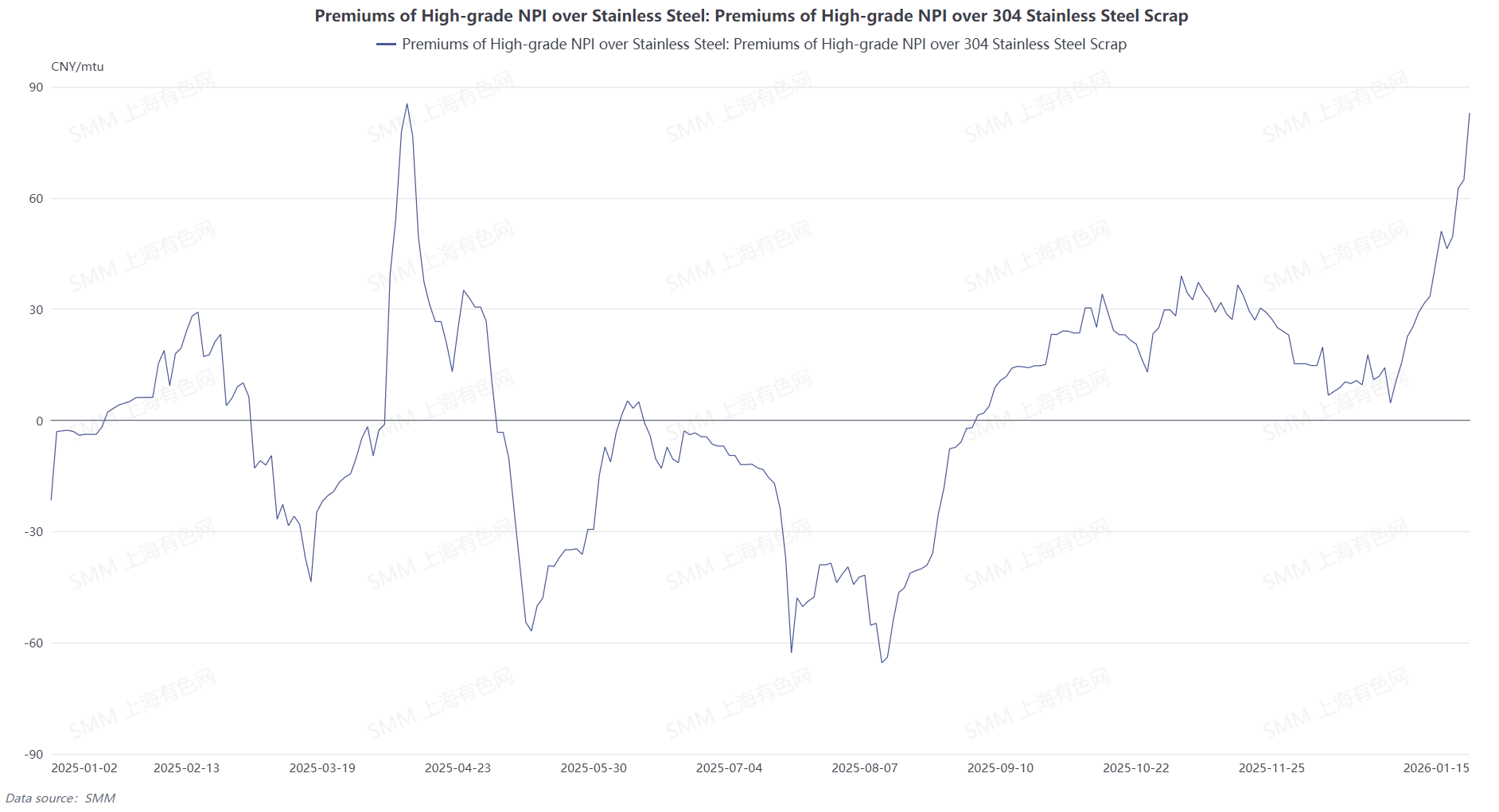

As futures continue to fluctuate at highs, some downstream steel mills have reported transaction or indicative prices of 1,020 yuan/mtu delivered, while upstream enterprises hold prices firm with strong sentiment, driving high-grade NPI prices to sustain significant increases.

Considering both upstream and downstream markets, although market offers have risen along with futures, actual transaction prices are currently hard to identify. Some upstream traders have raised offers to 1,100 yuan/mtu, while downstream mainstream indicative prices remain at 1,020 yuan/mtu. At the same time, weak fundamentals have fostered a strong wait-and-see sentiment among downstream enterprises.

Based on stainless steel finished product prices, the acceptable high-grade NPI procurement price is already above 1,050 yuan/mtu. However, due to weak end-use consumption and the significantly enhanced cost-effectiveness of stainless steel scrap, most stainless steel enterprises have prioritized purchasing scrap stainless steel. Additionally, as most enterprises have completed their stockpiling ahead of Chinese New Year, current high-grade NPI demand is mainly driven by trader arbitrage and conversion to high-grade nickel matte, while actual demand from stainless steel mills remains weak.

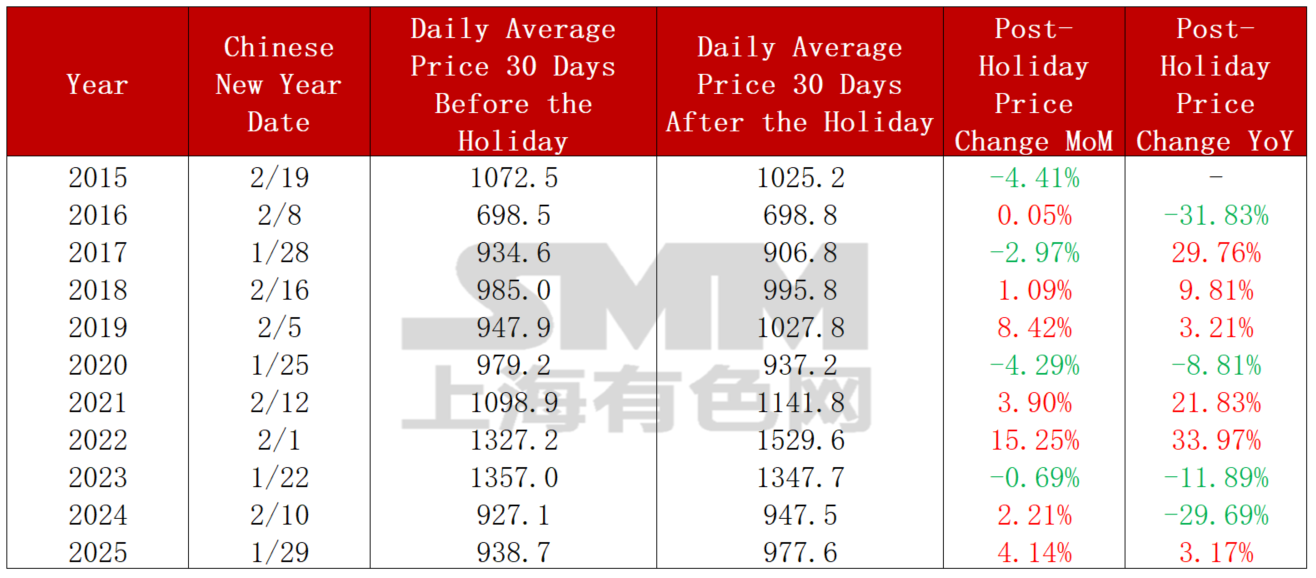

In summary, there is a serious divergence between upstream and downstream, with a wide gap in market offers. Under the influence of this divergence, coupled with weak end-use demand, substantial transactions may be difficult to achieve in the short term. Meanwhile, as macro and ore-side influences increase and most enterprises have procurement needs after the holiday, current market attention is generally focused on the high-grade NPI price trend after Chinese New Year. Below is a comparison of the average price of 8-12% high-grade NPI 30 days before and after Chinese New Year from 2015-2025:

As shown in the chart above, over the past decade, prices after the holiday have generally increased noticeably compared to pre-holiday levels, which is linked to post-holiday market recovery and the release of restocking demand. Under current conditions, with ongoing disruptions in Indonesian ore supply, recovering downstream stainless steel prices, strong price-firming sentiment among upstream enterprises, and limited spot cargo availability in the market, high-grade NPI prices are expected to find support.

![[SMM Nickel Sulphate Daily Review] April 3, Market Transactions Were Sluggish, and Nickel Salt Prices Declined Slightly](https://imgqn.smm.cn/usercenter/PFIti20251217171734.jpg)

![[SMM Analysis] This Week, the MHP and High-Grade Nickel Matte Markets Showed a Pattern of Weak Supply and Demand on Both Sides, with the Coefficient Remaining Stable](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)

![[SMM Nickel Midday Commentary] On April 3, nickel prices moved sideways, as Iran and Oman drafted an agreement on the regulation of the Strait of Hormuz](https://imgqn.smm.cn/usercenter/GmHLU20251217171733.jpg)